It’s been a mixed session here in Asia with Chinese stocks falling while Japanese markets lifted as Yen waned on a strengthening USD. The other majors are relatively unchanged though leading up to the US mid-term elections which are sure to ramp up volatility across risk markets. The RBA held at its meeting this afternoon with a small rise in the Aussie while the Kiwi has drifted lower in anticipation of the RBNZ meeting later in the week.

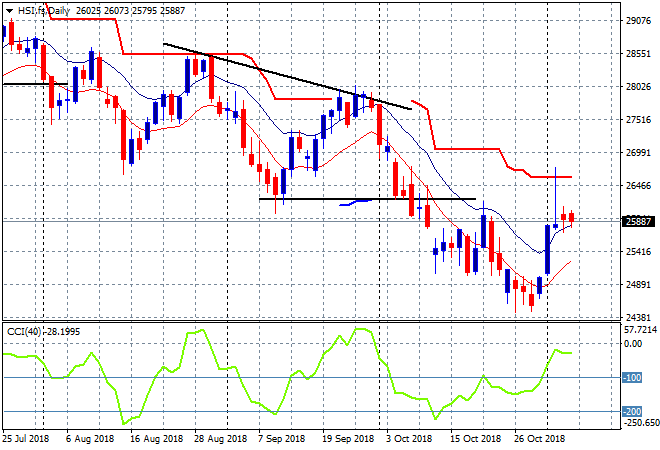

The Shanghai Composite is down 1% going into the close, currently at 2637 points, still maintaining above key support at the 2600 level but unable to translate the recent swing into a proper recovery. The Hang Seng Index is off only slightly, recovering from Monday’s losses to be down a handful of points to 25894 points, still below the previous support level at 26000 points. The daily chart still has some upside potential with no new daily low and price still above the high moving average:

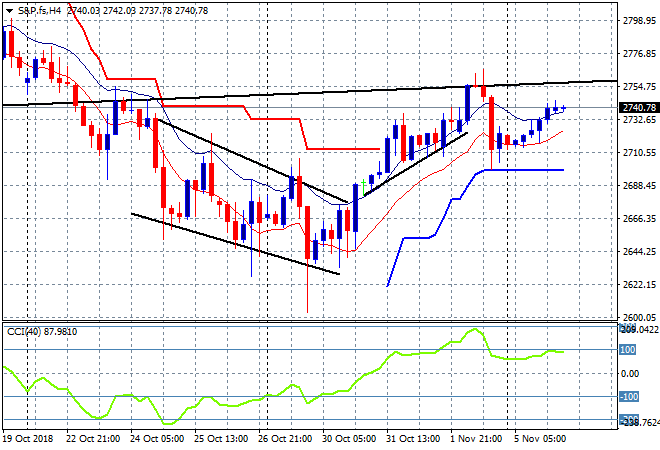

US and Eurostoxx futures are rising slightly, with the four hourly S&P 500 chart lifting and trying to get back to Friday night’s session high, still respecting tentative ATR trailing support at the 2700 point level. I still contend we can’t call this correction over before getting back above the previous monthly trendline (in black ) at the 2745 to 2750 area:

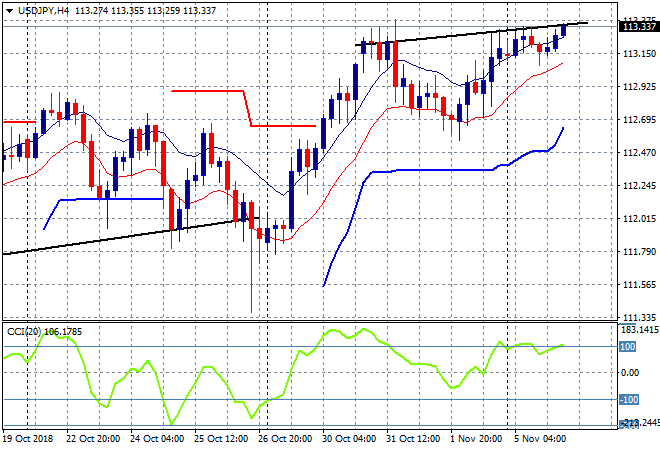

Japanese stocks have caught up to the postiive correlation with the rising USDJPY pair, as the Nikkei 225 pushed 1% higher to 22144 points. The USDJPY pair has now exceeded last week’s highs above the 113 handle, building for another rally but this could be wiped out quickly on tonight’s election result on any USD weakness:

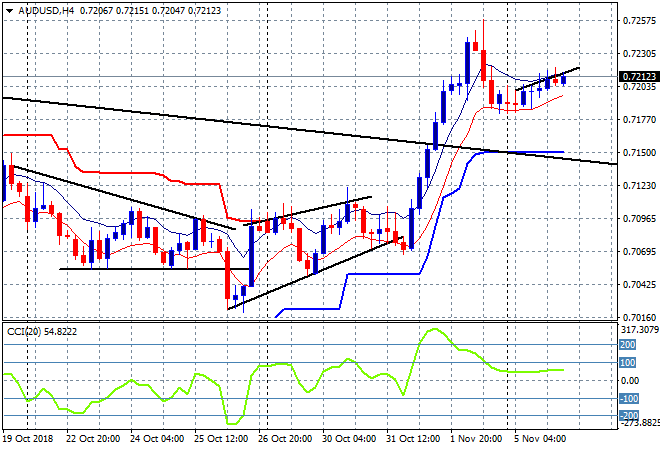

The ASX200 has finally seen some upside action as Melbourne Cup fever spreads over to the other great betting market, finishing a solid 1% higher to 5875 points. The Aussie dollar did nothing at all on the RBA meeting with only a slight uptick thereafter above the 72 handle with tight support just below at 71.70 as a good uncle point:

The economic calendar is relatively quiet tonight which is a good thing, given its the US mid-term election that everyone will be focusing on instead.