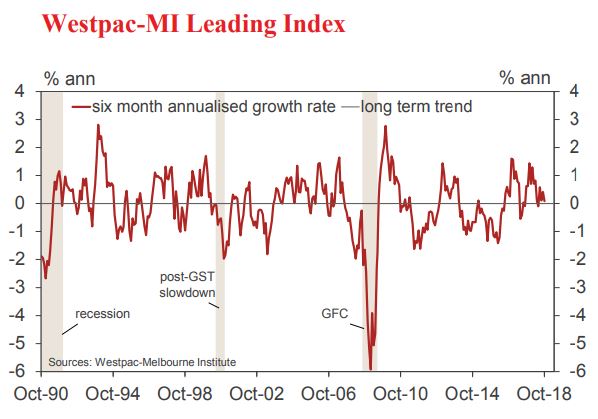

• The six month annualised growth rate in the Westpac–Melbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, , fell from 0.41% in September to +0.08% in October.

With this latest slowdown, the Index growth rate continues to point to slowing momentum into the new year. Over the seven months from October last year to April this year the growth rate averaged 0.89%.

In the six months since April the growth rate has averaged only 0.19% – a clear step down.

Those readings to April were consistent with the strong, above trend momentum in the official growth figures that showed the Australian economy growing at a 4% annualised pace in the first half of 2018. However the weaker reads we have seen in recent months point to a slower growth pace over the second half of 2018 and into 2019.

Westpac expects momentum to slow to around 2.5% in the second half of 2018, which will be slightly below trend, with this slower pace to be sustained through 2019 at around trend of 2.7%.

Factors that we anticipate will be important headwinds for growth going forward are: an uncertain outlook for the consumer with ongoing weak wages growth; falling property prices in Sydney and Melbourne and a very low savings rate pointing to limited capacity for households to maintain current spending momentum. We also expect a slowdown in jobs growth as both political uncertainty and global volatility weigh on firms’ employment decisions through the first half of 2019.

Despite a generally upbeat set of minutes from the Reserve Bank’s November Board meeting, these noted that “the outlook for consumption continued to be a source of uncertainty in an environment of slow growth in household incomes, high debt levels and easing conditions in housing markets in some parts of the country. 21 November 2018

Over the six months from May to October the growth rate in the Index held at 0.08%. There were few significant moves over that period with S&P/ASX 200 detracting 0.10 percentage points and dwelling approvals subtracting 0.14 percentage points. A number of small positives offset these effects.

Possibly of more interest in this report is the fall in the growth rate between September and October. The growth rate fell by 0.33 percentage points with S&P/ASX 200 subtracting 0.30 percentage points, US industrial production subtracting 0.18 percentage points and aggregate hours worked detracting 0.15 percentage points. Partly offsetting this was a positive contribution of 0.21 percentage points from RBA commodity price Index with little change coming from the domestic components of the Index.

The Reserve Bank Board next meets on December 4. The minutes of the Board’s November meeting confirm that there is still no urgency to move on rates although the Board maintains its view that, eventually, the overnight cash rate is more likely to rise than fall. Westpac reaffirms its view that the cash rate will remain unchanged for the remainder of 2018 and through 2019 and 2020.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.