How Does Fed Policy React To Stock Market Declines?

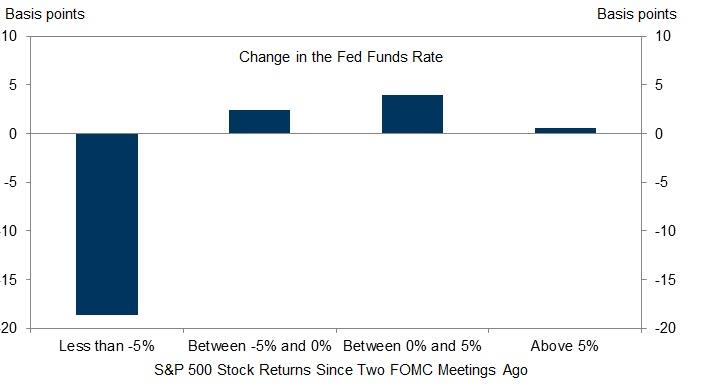

The equity market sell-off since the beginning of October has led to questions around whether the Fed will maintain its current path of rate hikes. Historically, the Fed appears to have responded with more accommodative policy after stock market sell-offs, on average (Exhibit 1). This has led some to conclude that there is a Fed “put,” in which the Fed responds to large stock market declines with accommodative policy, but does not change course when faced with small declines or increases in stock prices.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.