In one way, conventional thinkers will castigate the question. Here we are today with a deflating housing bubble and good growth, a very difficult task to pull off.

But Damien Boey at Credit Suisee has a few charts that suggest all is not rosy in today’s RBA IQ count:

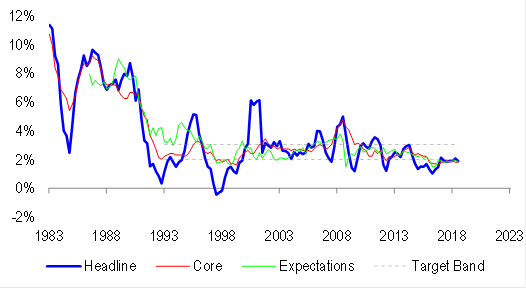

1. Core inflation is disappointing, and moving further below the RBA’s target band. Depending on the measure, it lies somewhere between 1.7-1.8% in year-ended terms, below the previously reported 1.9%.

2. Compositionally, headline CPI was weighed down by childcare rebates and falling telecommunications costs. But the rebates should have been stripped out from the core measure. And within the core, it appears that trend discretionary CPI inflation remains soft, despite the inflationary effects of AUD/USD depreciation on tradable prices. Also, housing-related inflation has been softening. The data suggests that pricing power is weak in a soft demand environment, which in turn is being driven by a sharp downturn in the housing cycle.

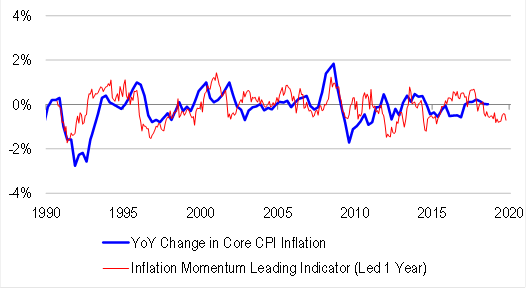

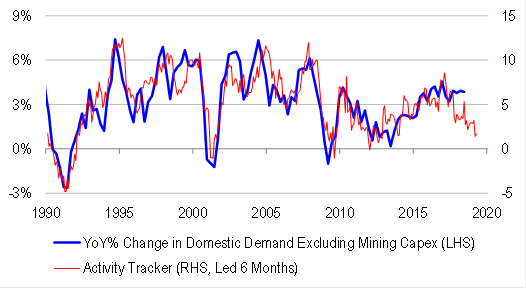

3. In terms of outlook, we expect to see more slowing in core CPI inflation. Our proprietary leading indicator, based on the deviation of activity growth from trend, the relative strength of emerging markets (EMs), and potential for AUD/USD depreciation, is pointing to further negative inflation momentum in the period ahead. Importantly, it is the softness of domestic demand growth, underpinned by recent weakness in housing, capex and consumer sentiment indicators, which is trumping the potentially reflationary influences of easing financial conditions in the EM complex, and scope for AUD/USD depreciation.

4. The RBA is unlikely to react much to the marginal downside surprise in CPI data. But nevertheless, bond and currency market investors are likely to respond. Cumulative CPI misses (relative to the Bank’s forecasts) are only getting bigger, and history suggests that this is likely to result in material inversion of Australian-US yield differentials, undermining the carry trade appeal of the currency. Curve flattening is also likely.

So is this the dumbest ever RBA? For one reason no it isn’t. The failure to forecast Australian disinflation started with the Stevens RBA and continues under the Lowe version. So there are two iterations involved:

But for the bank to persist with the stupidity and believe in its preposterous Futureboom! despite all evidence to the contrary for eight consecutive years kind of suggests that the bank is getting more stupid:

Does it really believe in this fantasy? Or is it some whack strategy to keep confidence up and the ponzi going a little longer? After all, it doesn’t want to get blamed for the bubble bursting.

Whether it is stupid or corrupt, neither conclusion is comforting.