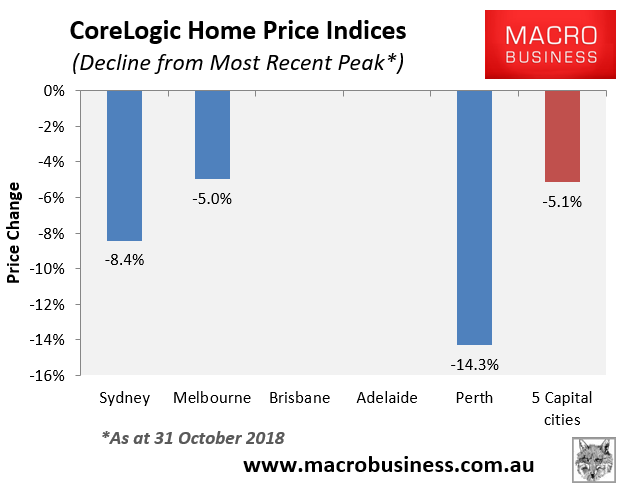

The ridiculous lack of affordable housing in Sydney and Melbourne has been brought to light in a new report from CoreLogic.

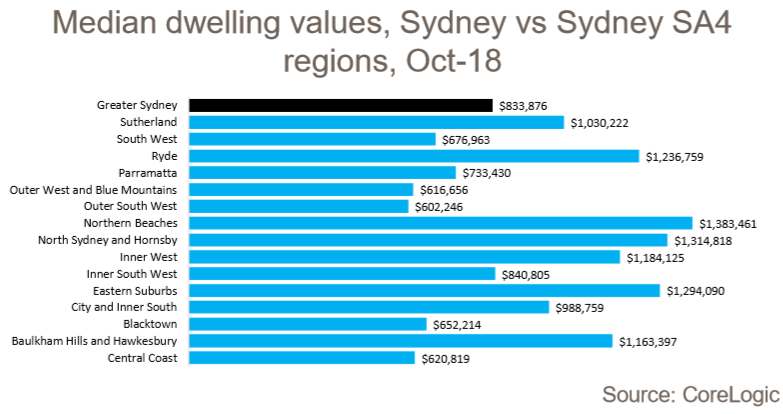

Despite dwelling values in Sydney declining a hefty 8.4% since peak:

There is no region within Greater Sydney where the median dwelling value is below $600,000:

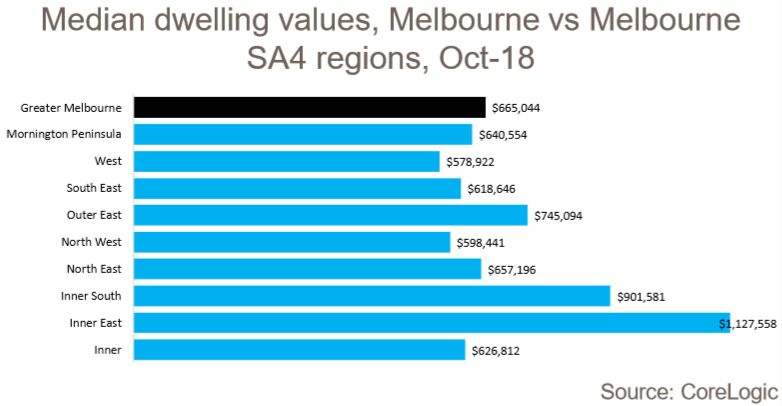

The situation isn’t much better in Melbourne, whose dwelling values have fallen 5.0% since peak:

Here, there are only two regions priced under $600,000, and only slightly.

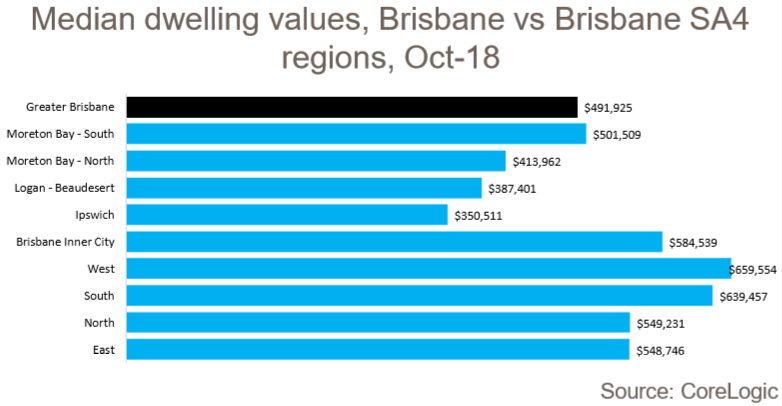

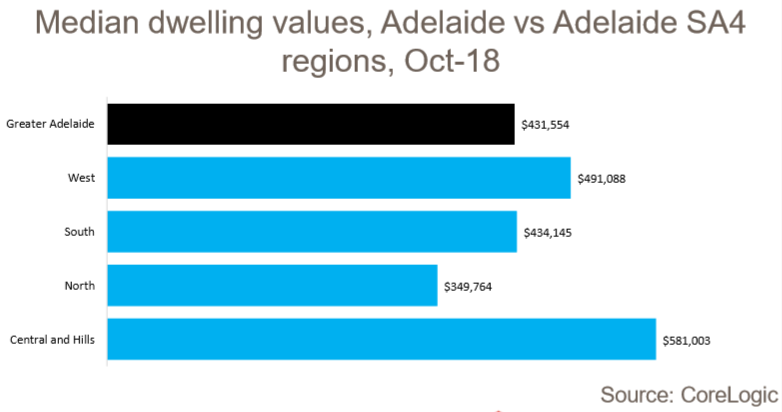

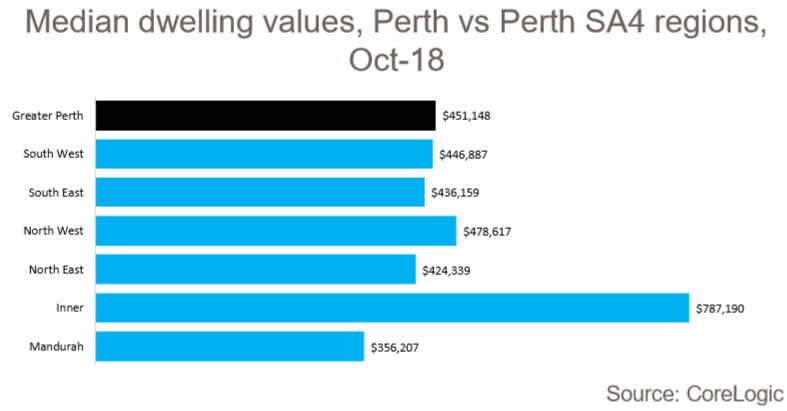

The situation is obviously much better in the other major jurisdictions, where dwellings are comparatively far more affordable, but still unaffordable overall:

These smaller jurisdictions also have a higher share of detached housing, meaning buyers get more ‘bang for their buck’.

Regardless, housing affordability in Australia stinks, especially in Sydney and Melbourne.