By Gareth Aird, senior economist at CBA:

Key Points:

- Australian residential property prices have fallen over the past twelve months.

- The near term indicators suggest that prices will continue to deflate.

- We believe that the best indicators to watch for assessing the very near term outlook for property prices are: housing finance; auction clearance rates, foreign residential demand; and the house price expectations index from the WBC/MI Consumer Sentiment survey.

Overview:

Dwelling prices are influenced by a range or factors. Prices go through both longrun super cycles as well as shorter-term cyclical ones. Over the medium to long run, prices are influenced by the economic cycle, the credit cycle (which is driven in part by monetary policy), tax policy, population growth, labour market participation, land release and dwelling construction. All of these factors are important for assessing the outlook for property prices over a multi-year horizon. But when considering the very near term outlook for prices it is more beneficial to focus on indicators that capture momentum.

We have identified four leading indicators of dwelling prices that we believe capture the momentum in the property market well. They are: (i) the flow of credit (i.e. housing finance); (ii) auction clearance rates; (iii) foreign residential demand; and (iv) the house price expectations index from the WBC/MI Consumer Sentiment survey. Some of these indicators are the symptom rather than the cause. And the lead times vary. But we consider each one of these indicators worth monitoring as they have a close relationship with near term changes in dwelling prices. From our perspective, we have found these indicators to be particularly useful for identifying turning points in short run housing price cycles. Presently all of these indicators are pointing to dwelling prices continuing to deflate over the near term (up to six months). This note discusses each factor.

(i) The flow of credit

The flow of housing credit is published monthly by the ABS in the housing finance publication. It measures the secured finance commitments for the purchase of owner occupied dwellings and finance commitments for the purchase of dwellings for rent or resale (investment housing). Put simply, it is the amount of money lent domestically each month to the buyers of Australian residential property. It differs from the stock of housing credit, published by the RBA, which is the total amount of credit outstanding to the household sector that was lent for the purposes of purchasing property.

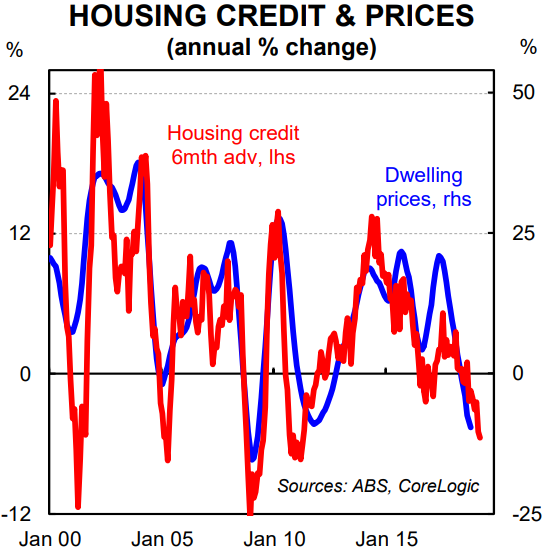

From a dwelling price perspective, the flow of credit matters more than changes in the stock. As chart 2 shows, the annual change in housing finance has a close leading relationship with the annual change in dwelling prices by around six months.

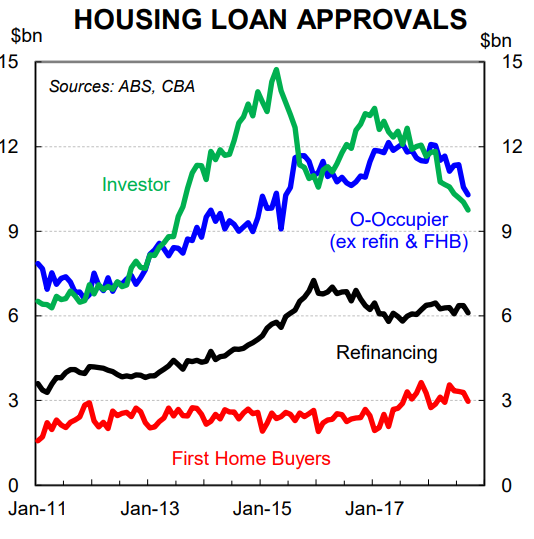

New lending is driven by the supply and demand for credit. The latest housing finance data indicates that the flow of housing credit continues to fall. And the pace of the decline has accelerated (chart 3). Credit to investors has been trending down for the past 1½ years. But it’s the shift downwards in lending to owner-occupiers that is behind the recent acceleration in the decline of credit.

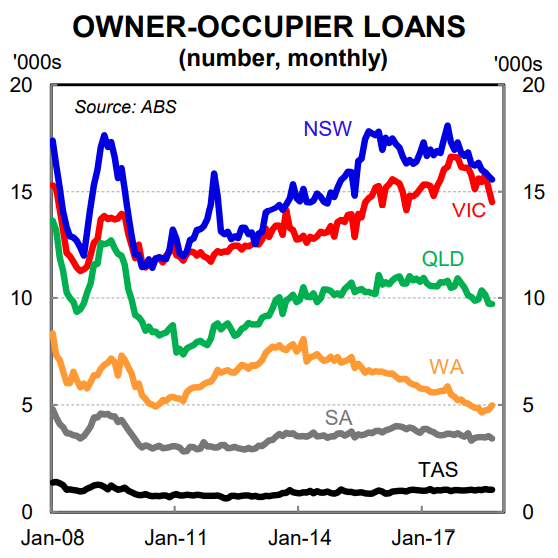

Why so? Lending standards have been tightened. But we believe that the demand for credit is having a bigger impact on new lending than the tightening in the supply of credit. We have that view for two reasons. First, it is not just the value of loans that is falling but also the number. As at September 2018, the total number of loans to owner-occupiers (ex. refinancing) was down by 11.1% over the year. Falls have been posted in most states (chart 4). A more rigorous assessment of living expenses should weigh on the value of lending. But it should not in and of itself have a material impact on the number of loans written. Second, credit to owner-occupiers has fallen sharply over the past few months. While there may have been some further tightening in lending standards by some financial institutions in the past two months, they would not have been sufficient enough to cause such a dramatic decline in lending over that period.

On their own, tighter lending standards should result in a “one-off” style levels adjustment to the flow of credit and a new paradigm should be set. That obviously takes a little bit of time given individual lenders have tightened at slightly different times. But as APRA Chairman Wayne Byres said in July, “the heavy lifting on lending standards has largely been done.” Therefore we conclude that tighter lending standards are not the primary driver of the acceleration in the downward trend of housing finance. Rather it is indicative of falling demand for credit because momentum and household expectations of property price appreciation have declined (see below).

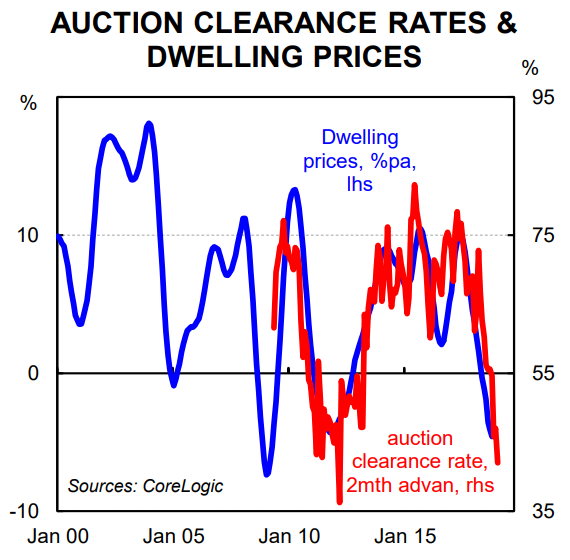

(ii) Auction clearance rates

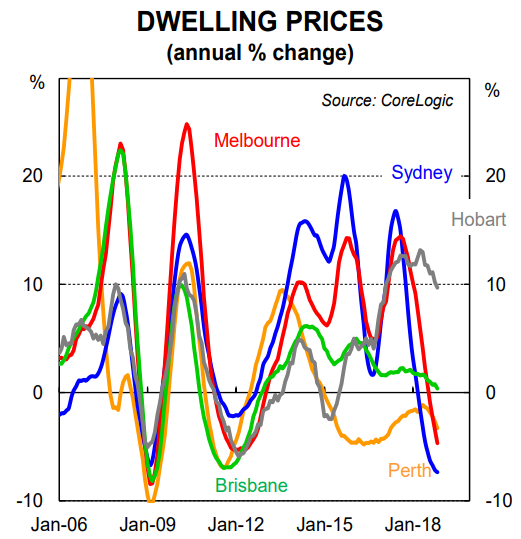

There’s a pretty sound relationship between auction clearance rates and annual changes in property prices. Generally auction clearance rates are a leading indicator of prices. As chart 5 shows, auction clearance rates tend to lead prices on average by two months. Auctions are more popular in Sydney and Melbourne as a means of selling a property. As such, the link between auction clearance rates and property prices is very much a Sydney and Melbourne story. As a rough rule of thumb, the annual change in dwelling prices tends to be negative when the auction clearance rate is below 55%.

Australia’s auction clearance rate has been on a downward trend since the beginning of the year. More recently the clearance rate has dipped to 40-45%. This is indicative of a housing market that has weakened and one where there is a mismatch between the expectations of buyers and sellers. As such, prices are adjusting downwards. The latest auction clearance rates imply that dwelling prices in Sydney and Melbourne will weaken further over the very near term.

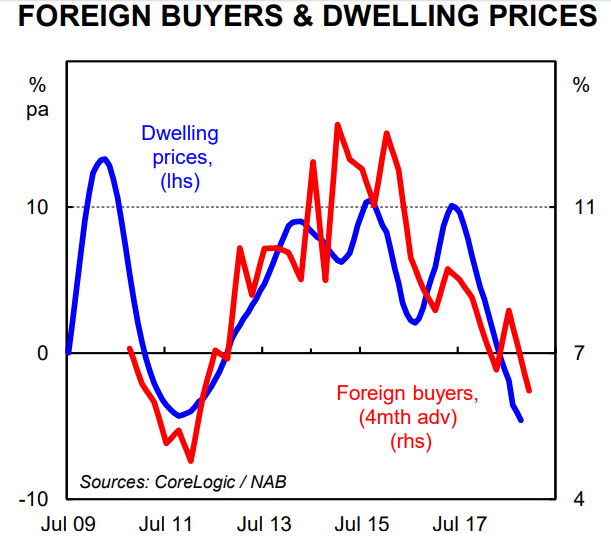

(iii) Foreign residential demand

Unsurprisingly, there is a relationship in Australia between the demand for property from foreign investors and dwelling prices. From early 2012, demand for Australian property, particularly in Sydney and Melbourne, was augmented by foreign buyers. But over the past two years, foreign investment in Australian property has waned. This is primarily due to a lift in state government stamp duties levied to foreign investors as well as tighter capital controls out of China.

The NAB Quarterly Australian Residential Property Survey captures housing sales to foreign investors as a share of total sales. As chart 6 shows, there is a decent relationship between the annual change in property prices against the share of sales going to foreign investors. Generally foreign purchases have led prices on average by around four months, although that lead time has shrunk more recently.

The decline in foreign investor demand is consistent with a further easing in dwelling prices over the near term. At present, there is no evidence to suggest a rebound in foreign investor demand unless there is a policy change – such as a reduction in stamp duties levied to foreign investors.

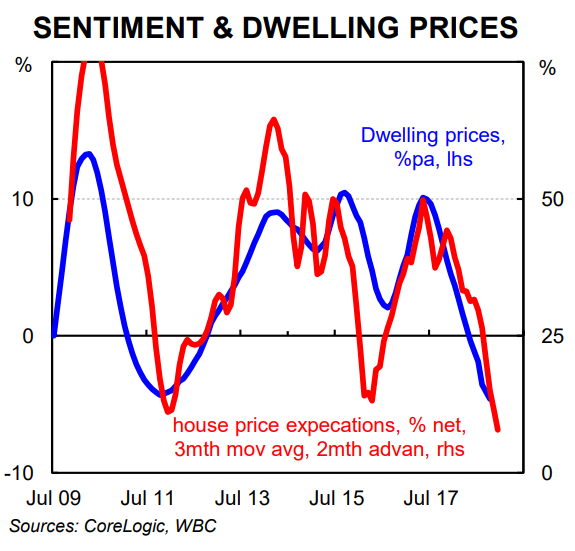

(iv) House price expectations

The monthly WBC/MI Consumer Sentiment survey contains an index that captures the consumer response when asked about their expectation of house prices in their state over the next 12 months. The question has been included in the survey since late 2009. It is effectively a gauge of the sentiment towards housing from an asset price perspective.

As chart 7 shows, it has proved a very useful near term indicator of the annual change in dwelling prices. There is of course a self-fulfilling aspect at work. If households expect prices to weaken then demand for credit will fall and prices will correct lower. The reverse is also true when households expect price growth to accelerate. That is why we believe that momentum indicators of the market are the most important to assess when looking at what is likely to happen to prices in the very near term. The WBC/MI house price expectations index is pointing to dwelling prices continuing to deflate over the near term.

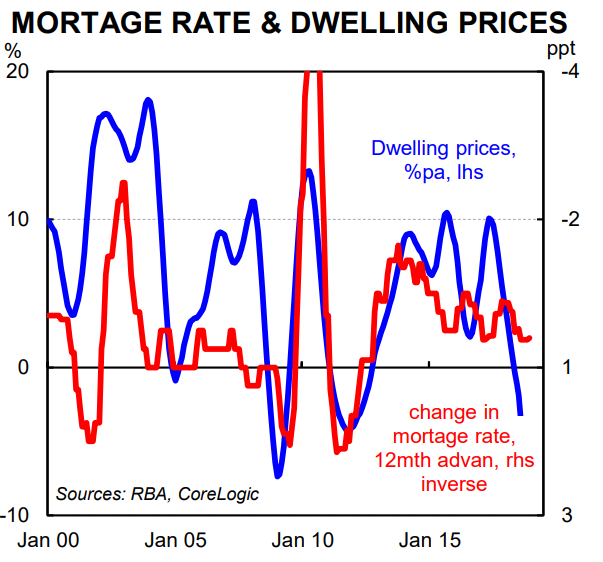

What about changes in interest rates?

Clearly changes in mortgage rates have an impact on dwelling prices (chart 8). And in that sense we could have included mortgage rates on the list of leading indicators of property prices. But we didn’t because the impact of changes in interest rates on property prices shows up in the housing finance figures. That is, changes in mortgage rates impact the demand for credit which is captured in the flow of new lending. And given the leading relationship between the flow of credit and dwelling prices we can pick up the impact of changing mortgage rates on dwelling prices by monitoring the flow of credit.

Having said that, borrowing and lending rates are used by investors for valuation purposes and are the benchmark for assessing what a “good” or “reasonable” return is. That is an important determinant of dwelling prices in the medium term. But in general, when assessing the near term outlook for property prices we can account for the impact of changes in mortgage rates by looking at the change in the demand for credit.

Conclusion

The evidence suggests that dwelling prices will continue to deflate in the very near term. As always, there will be significant variations between capital cities and indeed suburbs within the same cities. But the broader trend should be one of continuing mild price declines.

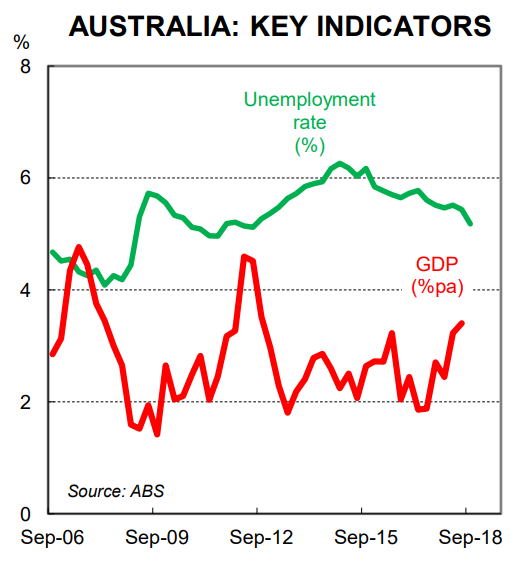

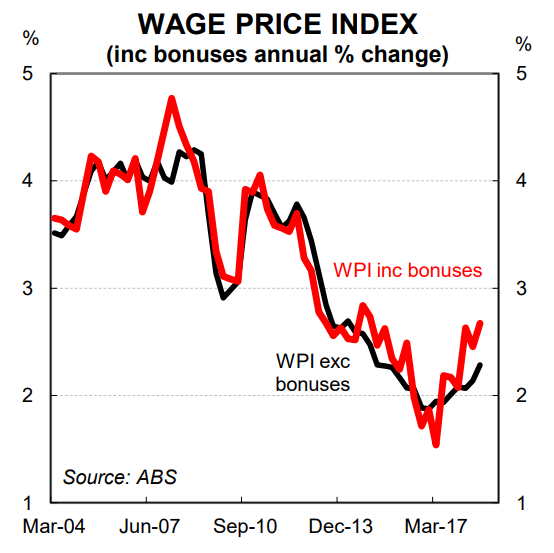

To date, the RBA has remained relaxed about the fall in dwelling prices because the broader economy has performed relatively well – economic growth has lifted and the unemployment rate has declined. And wages growth is also slowly accelerating (charts 9 and 10).

As long as the downturn in the housing market remains divorced from the broader economy the RBA will continue to signal that rates are more likely to go up than down. But the risk of a negative wealth effect impacting consumer spending is rising the longer the downturn in dwelling prices persists. The monthly reads on retail sales and the quarterly national accounts data on household expenditure will warrant close monitoring for any sign that a negative wealth effect is materialising.