DXY was soft overnight. CNY weak. EUR strong:

AUD was mostly up:

Gold was warm:

Oil cold:

Base metals too:

Big miners lifted anyway:

EM stocks firmed:

And junk:

The Treasury curve flattened for the first time in a while:

Bunds were stable:

Stocks were up solidly but Nasdaq struggled with Apple:

Westpac has the wrap:

Market Wrap

Global market sentiment: Markets were sidelined ahead of the US midterm elections. US equities are slightly firmer, while the US dollar and US bond yields are slightly lower.

Interest rates: The US 10yr treasury yield slipped from 3.21% to 3.18%, while the 2yr yield ranged sideways between 2.89% and 2.91%. Fed fund futures yields repriced the chance of another rate hike in December at 75% (from 80%).

FX: The US dollar index is down 0.1% on the day. EUR bounced off 1.1354 to 1.1408. USD/JPY ranged between 113.05 and 113.35. AUD ranged between 0.7185 and 0.7215. Outperformer NZD rose from 0.6635 to 0.6675. AUD/NZD slipped from 1.0835 to 1.0805.

Economic Wrap

US services sector activity cooled in October, the ISM survey falling back from record levels to a still very solid 60.3 versus consensus at 59.0. The underlying detail on new orders, prices paid and employment all moderated a touch, but remain at lofty levels too, consistent with ongoing strong momentum in the services sector. Markit’s service sector PMI backed the strong message from the ISM survey, the final reading for their October survey was revised a touch higher to 54.8 from a preliminary 54.7 and last month’s 53.5.

Brexit – Comments from both UK and EU officials downplayed the potential for an imminent breakthrough this week and again highlighted the difficulty of gaining an Irish Border solution.

EU Fin-Min meeting will discuss Italian budget proposals. EU officials denied that they demanded a deadline for an Italian response by 13th November.

UK services PMI in October at 52.2 was lower than expected (53.3). As with the manufacturing sector, lower new business and greater Brexit uncertainty weighed on the participants.

Event Risk

Australia: The RBA policy meeting is expected to be on hold and contain few significant changes. The Statement on Monetary Policy is released on Friday and will provide an update to their forecasts and risk assessment.

Euro Area: ECB Chief Economist Praet speaks in Brussels at an event on managing financial crises.

US: Congress holds midterm elections. The Republicans currently hold both houses. Pundits and prediction markets reflect a strong likelihood that the Republicans retain the Senate and that the Democrats take the House. Results will come out on Wednesday (AEDT).

The Aussie dollar is still chopping through its huge market short, rallying on risk. It has plenty more work to do.

Yet there are still very big reasons why it is difficult to see any sustained bottom. Quite apart from the slowing local economy and housing bust, the US out-performance continues and yield spreads just keep widening to everywhere else. To Germany:

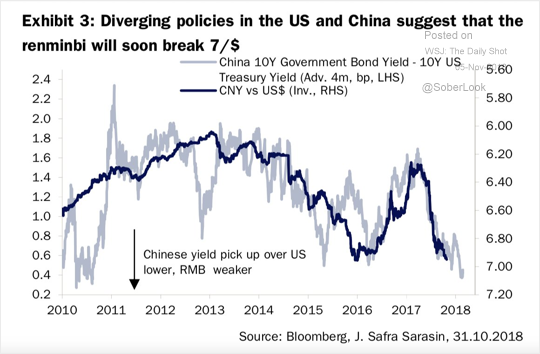

And China:

And there is more easing coming in the latter. Cold War 2.0 is a complicating factor but underneath that the momentum is still with DXY and away from AUD.

I doubt we have yet seen the bottom.