DXY was flat last night. EUR and CNY similar:

AUD caught a dose of RBA stupid as it rose towards Futureboom!

Gold fell:

Oil fell:

Base metals fell:

Big miners fell:

Junk was firm:

Treasuries sold

Bunds less:

Stocks ground out more recovery:

Westpac has the wrap:

Market Wrap

Global market sentiment: Risk sentiment was moderately firm ahead of the US midterm elections. The S&P500 is up 0.5%, while US bond yields are slightly higher.

Interest rates: The US 10yr treasury yield rose from 3.19% to 3.22%, while the 2yr yield rose from 2.90% to 2.93. Fed fund futures yields repriced the chance of another rate hike in December at 80% (from 75%).

FX: The US dollar index is up 0.1% on the day. EUR ranged between 1.1390 and 1.1440. USD/JPY rose from 113.10 to 113.50 – a one-month high. AUD round-tripped from 0.7215 to 0.7241 and back. NZD similarly round-tripped from 0.6665 to 0.6684 and back. AUD/NZD slipped from 1.0845 to 1.0815.

Economic Wrap

The US Job Openings and Labour market Turnover Survey (JOLTS) showed some moderation in key labour market metrics, but broadly continues to point to tight labour market conditions. The number of job openings eased back from record highs in September to 7.01mn (vs expectations at 7.09mn), while the quits rate – a gauge of employee confidence in job prospects – held steady at seventeen year highs of 2.4%.

Eurozone final service (53.7) and composite (53.1) PMI’s lifted from their Flash readings (53.3 and 52.7) on the back of improved outcomes in Germany and Spain. However, Italy’s slip to contraction and the decline in overall confidence across the region highlight the risk seen in the orders components, as was reflected in Markit’s commentary on the data.

The GDT dairy auction resulted in a 2.0% fall in prices overall, with whole milk powder down 2.9% (slightly weaker than yesterday’s futures market prediction of 0% change).

Event Risk

NZ: Q3 labour data is expected to show a decline in the unemployment rate from 4.5% to 4.4%, a steady jobs growth rate of 0.5% qoq, and a steady 0.6% qoq wage growth rate. We also have the RBNZ’s 2-year ahead inflation expectations survey.

China: Oct foreign reserves data is released.

US: Results of the midterm elections held on Tuesday will be released. The Republicans currently hold both houses. Pundits and prediction markets reflect a strong likelihood that the Republicans retain the Senate and that the Democrats take the House.

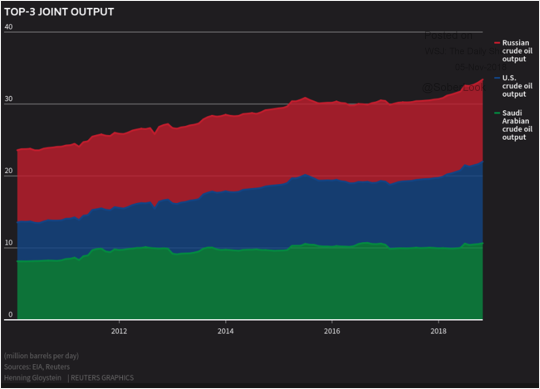

Oil is suddenly and seasonally weak. In truth it’s been building for weeks as Saudi, the US and Russians have all piled into the Iran gap:

US especially is booming:

Driving up inventories:

And triggering market selling:

Prices are still too high at $72. Everyone can expand above $50. As the global economy slows we may well see lower prices yet, meaning diminished pressure on bonds everywhere and support for equities, so long as it doesn’t crash.