DXY is up and almost away. EUR is weak. CNY less so:

AUD held on anyway:

It was mixed against EM:

Gold dropped:

Oil held on but if OPEC can’t cut then US shale must and that means $40-45:

Base metals are under the pump:

And big miners:

EM stocks also held on:

But EM junk let go:

The Treasury curve flattened:

Bund curve too:

Stocks were mixed:

Westpac has the wrap:

Market Wrap

Global: USequities were not too ruffled by President Trump’s latest threat to impose more tariffs on China, the S&P500 unchanged. Oil is down 1.5%, and the US dollar is higher.

Interest rates: The US 10yr treasury yield rose from 3.05% to 3.07%, while 2yr yields rose from 2.82% to 2.84%.

FX: The US dollar index is up 0.4% on the day. EUR fell from 1.1345 to 1.1280. USD/JPY rose from 113.45 to 113.85. AUD fell from 0.7250 to 0.7200. NZD ranged between 0.6770 and 0.6810. AUD/NZD fell from 1.0680 to 1.0630, perhaps reflecting expectations of an LVR loosening by the RBNZ today.

Event Wrap

US consumer confidence dipped in November to 135.7, matching consensus expectations, but that follows five consecutive monthly gains that lifted sentiment to 18 year highs. Most of the pullback was due to an easing in the expectations sub index (to 111 from 115.1), while present conditions firmed and households’ assessment of the labour market rose to a another 18-year high.

Fed Vice Chair Clarida stuck to existing Fed policy themes, stressing caution via data dependence and a gradual trajectory for Fed Funds. He noted that the Fed is “much closer” to neutral and was hopeful that inflation would continue to run close to 2% despite strong growth and a robust labour market given positive prospects for labour force participation and higher business investment

Event Outlook

NZ: The RBNZ Financial Stability Review at 9am this morning is a possible forum for a loosening of property lending restrictions.

Australia: Q3 construction work is expected to rise 0.9%. Westpac’s forecast is for a 0.6% increase with continued strength in public works partly offset by consolidation in new home building.

Euro Area: Oct money supply and credit data is due.

US: Q3 GDP 2nd estimate is expected to be unrevised at a 3.5% annualised pace. Oct new home sales have been edging down but are expected to be up 4.0%, reversing the majority of Sep’s 5.5% decline. Fed Chair Powell speaks on “The Federal Reserve’s Framework for Monitoring Financial Stability”.

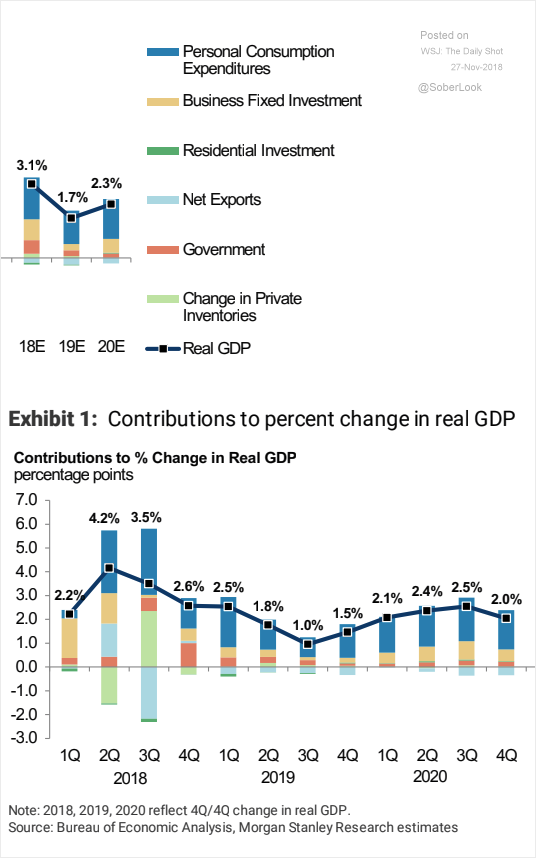

Markets are in a transition from fearing Fed hikes to fearing growth. Here are some charts that illustrate the point. Fundamentally, the US will slow with the fiscal cliff:

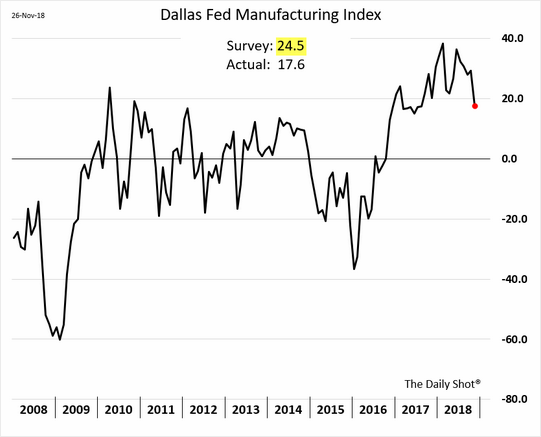

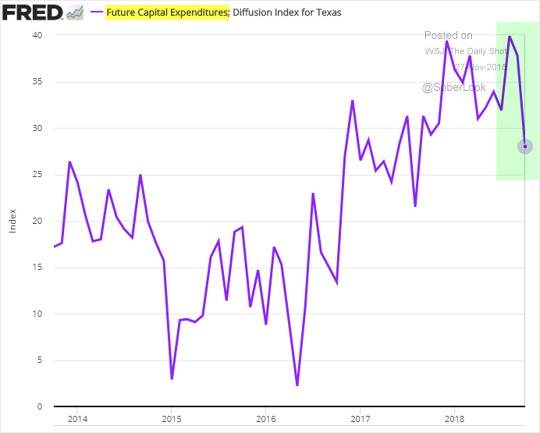

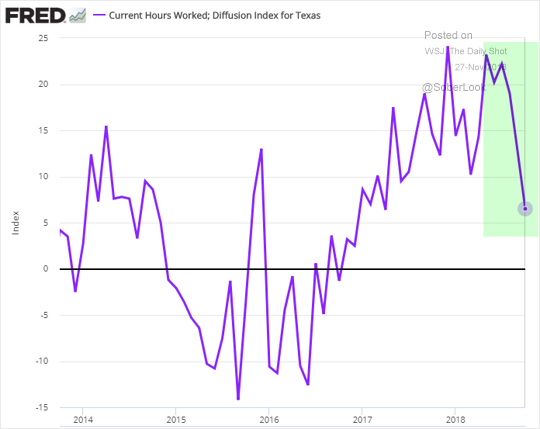

Adding to that now is the oil patch smash:

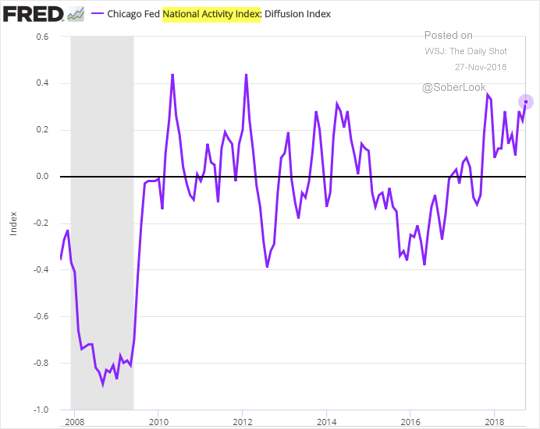

Wider activity is still strong:

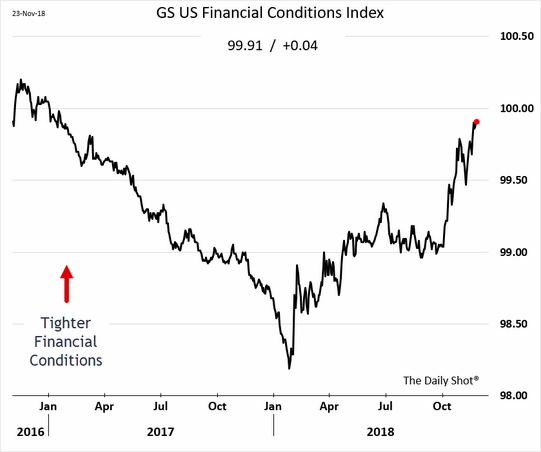

But so is financial tightening:

The Fed is going to have to pause, maybe even after the December hike. This is giving the AUD and some EMs a bid even though DXY remains strong. The two swing factors are Trump infrastructure and the oil price. The former is likely but it seems equally the case that Dems may delay its takeoff until it benefits them in late 2020. The latter hangs on an OPEC cut.

We remain AUD bears in trend terms as China will keep slowing and the terms of trade keep correcting plus the housing bust intensifies. But we also acknowledge that a short term bottom may be in if US growth can find no new driver.