From Shayne Elliot yesterday:

Mortgage credit growth would probably halve, to 2 to 3 per cent, in the coming years, Mr Elliott said, and credit growth from investor borrowers has already “ground to a halt”.

“I wouldn’t be surprised if it [the house price correction] had further to run … I wouldn’t be surprised if it continued a bit longer.”

…Not using HEM means “the process will become a little but slower” because borrowers will need more documents to support loan applications, Mr Elliott said.

…The average household average on income of $110,000 three years ago could have borrowed $550,000 for a mortgage but “that same family today with exactly the same income – $110,000 – today could probably only borrow about $440,000,” Mr Elliott said.

…”Will they continue to fall? I don’t know. [But] I don’t think borrowing capacity is going to go up any time soon.”

So, there it is from the horse’s mouth. Assuming a 10% deposit on that $500k home (which is clearly in neither Sydney nor Melbourne!) a 20% fall in available credit should equate to roughly a 17% fall in the house price (assuming that they low ball the same place). And why wouldn’t they given the same calculus extends across the market.

Eliminate interest-only, add out of cycle rate hikes and abundant new supply, the removal of negative gearing income, falling immigration plus an inevitable turn in sentiment and that pushes losses well below 20%. All markets panic at some point, too, probably around an offshore shock when the RBA runs out of ammo, and there’s your capitulation. Then there will be the negative feedback loops in finance itself.

It is very easy to see Sydney and Melbourne down 30% over five years in nominal terms. That’s -40% real.

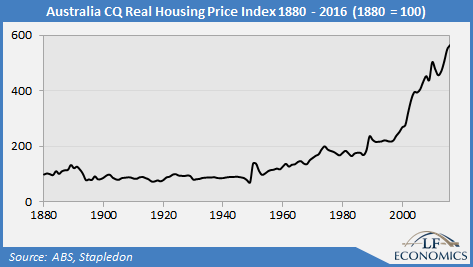

Beyond that, generational scarring, conservative banks and lower immigration will ensure that it is an L-shaped recovery as well, so the real losses could keep mounting for decades, just as they did after the 1890s:

It was always a bubble and the royal commission is the pin.