This month’s figures revealed that the Australian economy grew 0.9 percent in the June quarter, above the 0.7 percent market consensus forecast. Growth was supported by strong domestic as well as overseas demand; fixed investment, however, remained flat. CPI inflation remains at 2.1%, inside the Reserve Bank of Australia’s official target band of 2-3%, and the unemployment rate at 5.3%. The RBA Shadow Board rules out any likelihood that a reduction in interest rates could be called for. It attaches a 45% probability that holding interest rates steady at 1.5% is the appropriate setting, while the confidence in a required rate hike equals 55%.

The seasonally adjusted unemployment rate in Australia, according to the latest ABS figures, remained steady at 5.3%. Net employment increased by 44,000, three quarters of it full time employment. The participation rate edged up from 65.5% to 65.6%. Real wage growth, which is reported quarterly, remains flat. Considerable focus will be placed on the November announcement to see whether the relatively low unemployment rate is generating any inflationary pressure.

The Aussie dollar, relative to the US dollar, is oscillating within the 71-73 US¢ range. Yields on Australian 10-year government bonds have rebounded to above 2.7%, after marking a recent low of 2.52%. The Australian stock market remains buoyant, with the S&P/ASX 200 stock index currently priced above 6,200.

The fiscal profligacy in the US is continuing to fuel its economic boom. The unemployment rate remains at a historical low of 3.9%, while CPI inflation has increased to 2.7% and the US trade deficit widened by 9.5% to US$ 50.1 billion in the July quarter. Another increase in the federal funds rate is expected before the end of the year, possibly two. The US administration has widened the range of tariffs imposed on Chinese and other imports, bringing the WTO to publicly appeal for restraint on the trade war and to downgrade its forecast for the global economy. The US boom contrasts with economic news from many other countries, in particular emerging markets, which are experiencing significant slowdowns. Emerging market equity prices and currencies have fallen more than 20% from their highs earlier this year. High-yield credit spreads between the US and the rest of the world are likewise rising, pointing to an uncomfortable divergence between the US and global economies. This divergence could mean that the US economy’s strength is fleeting and it is only a matter of time before the US economy will fall in line with the rest of the world. A more benign interpretation is that the US and global economies are not as interconnected as most analysts suppose.

Both consumer confidence, as measured by the Westpac Melbourne Institute Consumer Sentiment Index, and business confidence, according to the NAB business confidence index, have softened. Manufacturing production expanded slightly, whereas the services PMI continued its recent decline. Capacity utilization barely moved, remaining slightly above 82% in August. The only new indicator relating to the housing market, the construction PMI, fell marginally, from 52 to 51.8. Along with wage growth, the evolution of the housing market will continue to attract interest as it affects the outlook for monetary policy.

The distribution of the Shadow Board’s policy preferences has shifted mildly in favour of a rate increase. The Shadow Board is 45% confident that keeping interest rates on hold is the appropriate policy, three percentage points down from the previous month. It attaches zero probability that a rate cut is appropriate (unchanged) and a 55% probability (53% in August) that a rate rise, to 1.75% or higher, is appropriate.

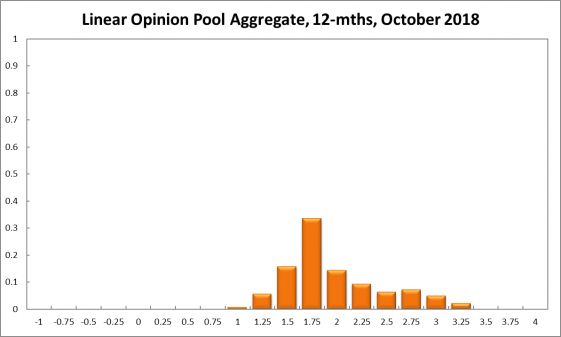

The probabilities at longer horizons are as follows: 6 months out, the estimated probability that the cash rate should remain at 1.50% equals 23%, one percentage point down from the previous month. The estimated need for an interest rate decrease fell back to 4%, where it was two months ago, while the probability attached to a required increase rose from 71% to 73%. The numbers for the recommendations a year out paint a similar picture. The Shadow Board members’ confidence that the cash rate should be held steady equals 16% (17% in September), while the confidence in a required cash rate decrease equals 6% (7% in September), and in a required cash rate increase 78% (76% in September).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.