The Australian dollar could retest its post-2014 cycle lows below US70¢, according to NAB, amid continuing and potential enduring weakness across emerging markets.

…”The message is fairly clear; if we are not out of the woods regarding pressure on emerging markets – not just from the likely scaling up of US tariff actions on China but also rising US rates and potentially higher USD/EM Asia FX – the AUD is equally not out of the woods in terms of risk of returning to retest post-2014 cycle lows below US70¢,” NAB head of FX Ray Attrill wrote in a morning note.

More from NAB reprising September:

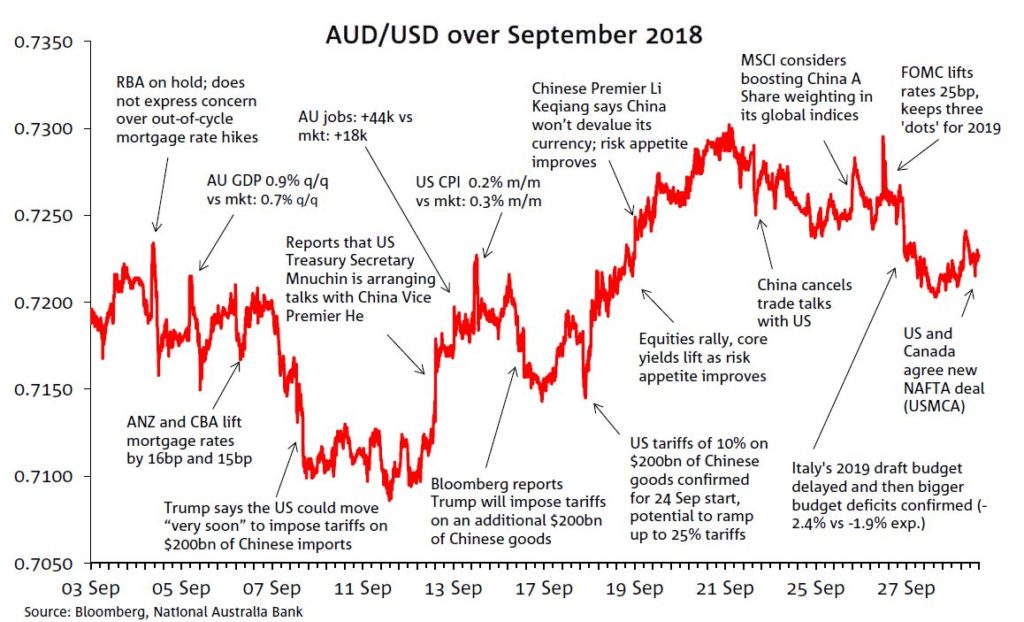

Heightened US-China trade tensions weighted on the pair early in the month driving the currency down to a low of 0.7085 on September 11th, a level not seen since mid-February 2016. However, in a classic “sell the rumour, buy the fact”, the announcement of a new round of US trade tariffs on Chinese imports with the threat of more to come was followed by an improvement in risk sentiment helping the AUD/USD reach a month to date high of 0.7302 on September 21st. Thereafter the cross was unable to make a sustained break above 73c, ending the month at 0.7227 with the downtrend established since reaching a high of 0.8136 late in January still unchallenged on monthly close basis.

Early in the month an RBA unconcerned over out-of-cycle mortgage rate hikes and a stronger-than-expected Q2 GDP print didn’t have lasting positive impressions on the AUD/USD. Instead US-led trade tensions were once again the bigger influence. The cross fell to 0.7102 on September 7th, as Trump suggested further US tariffs on an additional $200bn of Chinese imports were around the corner with tariffs on an additional $267bn of imports “ready to go”. The souring in sentiment saw Emerging Markets come under pressure and with that the AUD/USD down to a monthly low of 0.7085.

Eventually, US tariffs on a further $200bn of Chinese goods were announced on September 18th, but the fact these new tariffs were only 10% rather than 25% alongside reassuring comments from Chinese officials regarding their focus to stimulate their domestic economy with no intentions to seek a competitive devaluation of the yuan, boosted risk sentiment helping the AUD/USD briefly trade back above 73c.

Later in the month the Fed raised the Funds rate by 25bps to a range to 2-2.25%, as expected, and the removal of the word “accommodative” in the Statement was seen as a nod to the widely held view that the policy rate is getting pretty close to neutral. Although the Fed hiking decision was well priced, the AUD/USD still lost a bit of ground in the last few days of the month with the earlier improvement in risk dented by Italian budget concerns and the move higher in oil prices.

The NAB AUD Model

AUD/USD continues to trade near the lower edge of our short term fair value range (roughly +/- 3.5 cents) though has never managed to break below the range and so signal a clear ‘buy’ signal. Higher oil prices, to which LNG prices are formulaically tied, have been the main supportive influence, adding about half a cent to fair value in September. Coal has also been supportive, due to a 10% rise in spot coking coal prices. Aluminium was a negative influence though underperformed other base metals in September and as such was not representative of the broader base metals complex.

The lift in US front-end yields in September amid ongoing stability in AU-equivalent rates has pulled fair value down by almost a quarter of a cent, partly offset by a fall in the VIX, boosting the risk sentiment component of the model.

Commodities up, sure:

Advertisement

But negative spreads are exploding:

The net effect for the currency is still down.

With China beginning to stimulate building to offset the trade war headwinds, bulk commodity prices will be OK and support the terms of trade next year so I can’t see the Aussie dollar entering free fall. A grind lower into the mid and high 0.60s is still the base case next year, until the RBA is forced to cut by the housing correction.

Advertisement

David Llewellyn-Smith is chief strategist at the MB Fund which is long US equities that will benefit from a falling Australian dollar so he is definitely talking his book (or NAB is!). Below is the performance of the MB Fund since inception:

If the ideas above interest you then contact us below.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.