Yesterday we saw China’s “whatever it takes” moment, via Bloomie:

President Xi Jinping vowed “unwavering” support for non-state firms over the weekend, the country’s stock exchanges committed to help manage share-pledge risks, and the government released a plan to cut personal income taxes. That follows a rare coordinated effort from top financial officials on Friday to support the battered equity market.

“This rebound is very comforting, a warm current in winter’s frigid waters,” said Weining Chen, a fund manager at Miyuan in Beijing. “The remarks and polices since Friday are seen as an ample dose for now. But there are still expectations that the authorities will not stop here because the economic figures are still not looking optimistic.”

Regional stocks and debt rallied. Iron ore saw the writing on the wall for more stimulus:

These factors would in the past have delivered a big “buy Australia” signal in stocks, debt and forex. That happened in Asian markets. Yet in Australia the stock market fell, bonds were bid and the AUD dumped.

Obviously the Wentworth debacle played a role. But this is new too. Australian political risk has been shrugged off for years by markets.

Markets are beginning to wake up to the end of the houses and holes miracle. Bank funding costs still refuse to come down. Indeed they are still rising with the longer term moving averages on BBSW:

If this lasts much longer there will be more out of cycle rate hikes.

Banks are caught in a wrenching three year bear market that has decoupled Australian stocks form the world:

And key property bellwethers are now following :

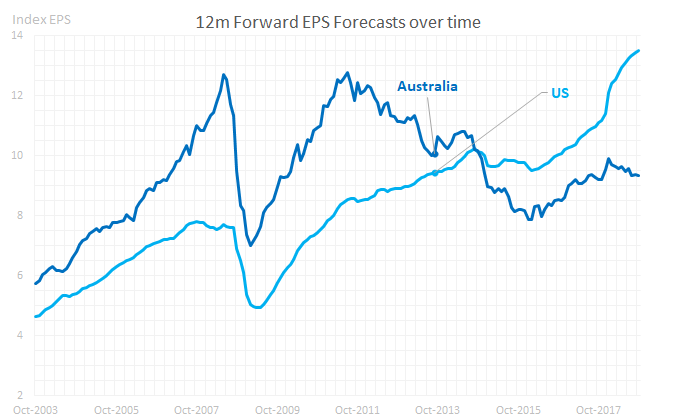

Indeed, the forward profit consensus for the entire bourse keeps falling:

In the past rising commodity prices would be interpreted by markets as rising income, higher wages, growing consumption and higher profits and taxes. Not any more. The nexus is broken as the rorted tax system fails to collect the income, the miner’s don’t rally so far on China risk, there’s no investment and flow through to jobs and wages and any tax cuts are distant on a stretched fiscal position. Then there is peak household debt and reform of corrupt banks to prevent the shift from rising national income to leveraging in global markets to bid up house prices and boost domestic demand.

The houses and holes economic model is broken. All there is in its place is an endless flood of cheap foreign labour to try to back fill the gap, destroying national politics in the process.

When China comes out and says it will do whatever it takes to support growth, bulk commodities pin their ears back yet Australian assets are seen as even less desirable you know that we are on the nose big time. And with three toxic elections ahead plus Cold War 2.0 intensifying by the day there does not appear to be any immediate circuit breaker ahead for Aussie assets.