By Chris Becker

A tumultous week on equity markets, spurred by the “Bondcano” as 10 year US Treasury yields continue to spike higher above the much vaunted 3% level. This has caused a cascade of effects, exarcebated by the ongoing trade tensions between the US and China. This has been setting up for sometime as stocks got way ahead of themselves throughout the year, following the intra-annual business cycle, and then of course culminating in a selloff in the late September, early October period. We’ve been here before, but is it the start of GFC 2.0 or just another – albeit rare – correction in the new era?

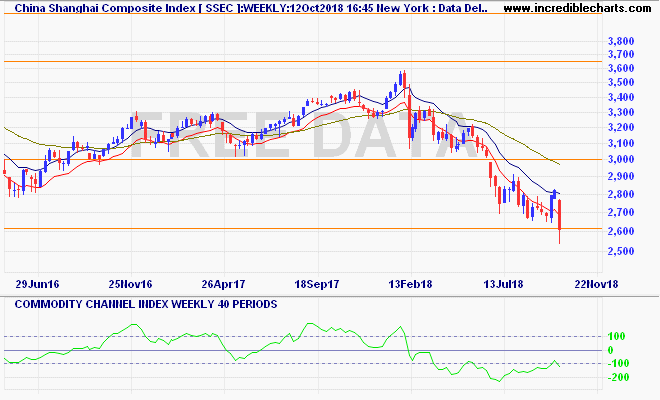

Looking at Chinese stocks first, last week saw the Shanghai Composite return from holidays and immediately gap down severely, wiping out the previous two weeks advance. Eventually the market recovered, bouncing off the 2600 point support level, but only just. The tail of buying support below that was filled is some good news, but the overall pattern does not give much hope here – perhaps a small bounce back up to 2700 but the bear market is staying: