By Chris Becker

Another US jobs report – the non farm payrolls or NFP – has come and gone but its impact was already felt on risk markets due to rising US Treasury yields, with even the 2 year closing in on the mythical 3% level. US stocks ended the week down as a nervous September rolls into a possibly ominous October for stock markets. Currency markets are still relatively mixed, with the USD still firm against the majors and undollar assets. Euro remains depressed, but not any lower while Pound Sterling jumped higher on positive Brexit implications, the Antipodean currencies remain in the toilet…

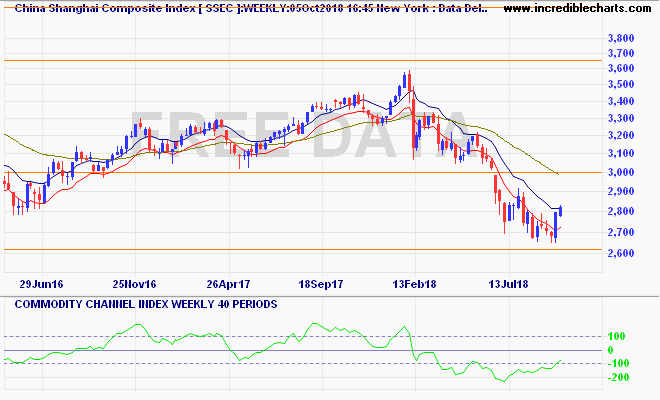

Looking at Chinese stocks first, last week saw the Shanghai Composite on holidays for “National Day” – a long bloody day! Anyway, the pattern still holds with the previous bounce off terminal resistance at the 2600 point level after cruising down into a decelerating price pattern. This would normally bode well for a swing move higher, but given the negative risk sentiment out there, I’m not too sure on the open this week: