By Chris Becker

The equity correction continued overnight with steep falls on Wall Street that were barely covered by the end of the session, with oil prices cratering in the wake of the Saudi’s murderous own-goal. This finally caused a rush to safety in Treasuries, with the 10 year yield falling to 3.11% and the chances of the December Fed rate hike also falling back from a near certainty. Confidence is seemingly shattered here, with prices at new weekly lows, but momentum is also extremely oversold, the usual precursor to a short covering bounce.

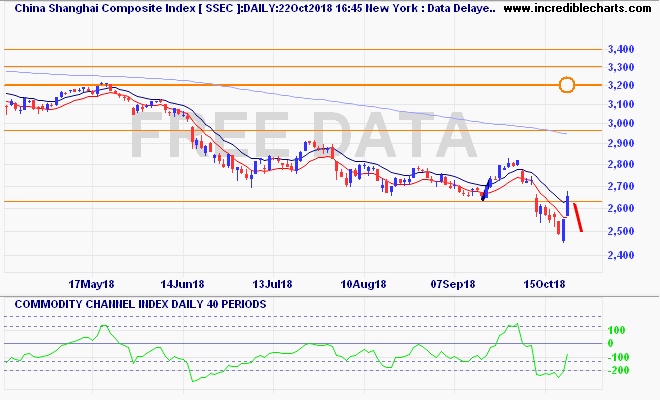

Recapping Asia’s session yesterday where the Shanghai Composite fell slightly before the long lunch break but has returned thereafter to sell off swiftly, closing 2.4% lower to 2589 points, getting back below key support at the 2600 level. The short term advance was swiftly brought back to earth with the daily chart still showing classic signs of a bear market, with my target still at the 2300 terminal support area. An inability in the short term to get back above 2600 will be telling: