The bounce is here in full with a sea of green across Asian stock markets today, navigating through a steady BOJ interest rate meeting and a somewhat disappointing Chinese manufacturing PMI print. Australian inflation figures – out of date given it’s quarterly – didn’t move the Aussie dollar that much either.

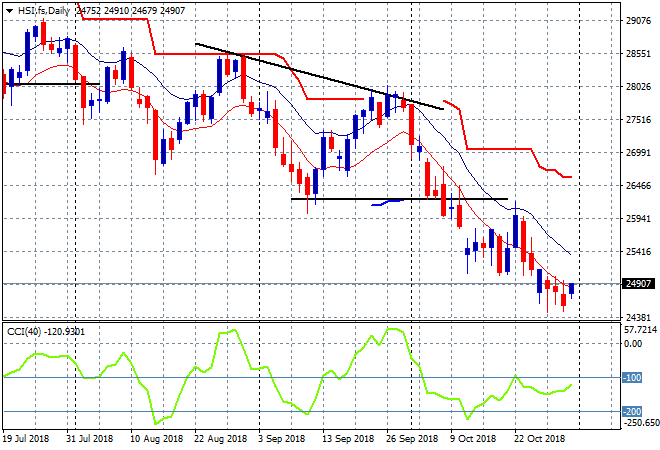

The Shanghai Composite is moving higher, currently up 1.5% going into the close at 2605 points, ready to maintain itself above key support at the 2600 level. The Hang Seng Index is playing catchup, up around 1.1% or so to 24858 points, but still below the previous support level at 26000 points with intrasession lows indicating a possible bottom here on a deceleration curve:

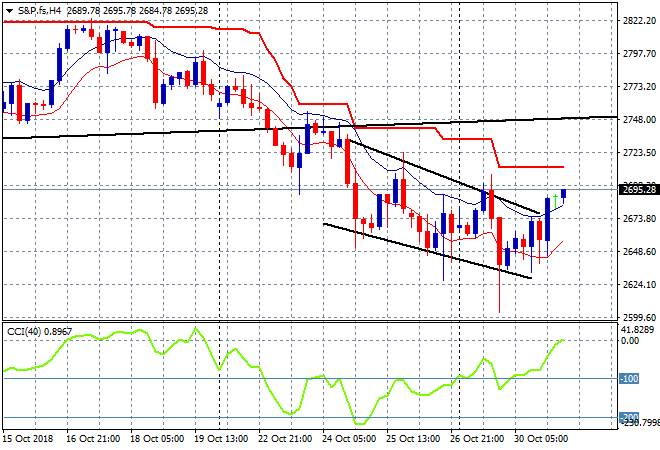

US and Eurostoxx futures are up firmly, with the four hourly S&P 500 chart showing a potential breakout here after a bottoming action overnight. The upper leg of this trend channel is getting crowded as a bounceback firms:

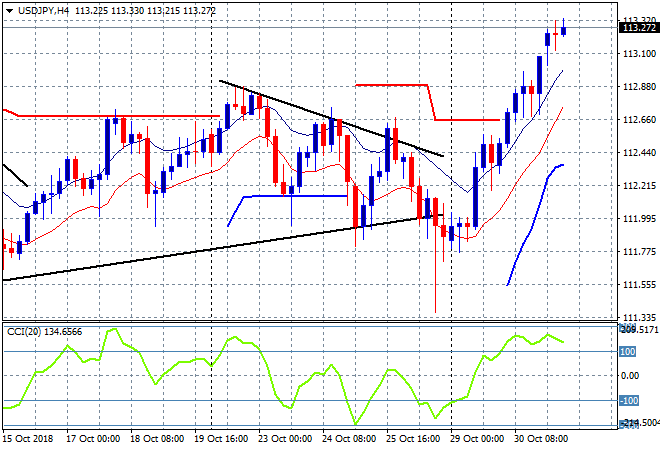

Japanese stocks were the best performers again due to the selloff in Yen with the Nikkei 225 closing 2% higher at 21878 points, doubling down on yesterday’s solid gains. The USDJPY pair finally pushed through the 113 handle, making not just another new daily high but a new weekly high as it too doubles down on its overbought status:

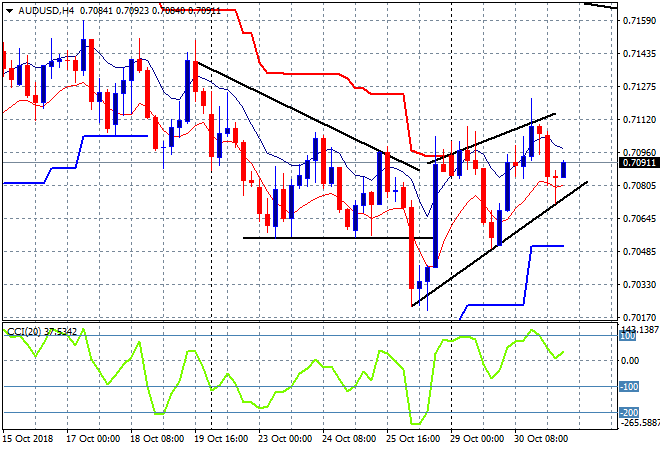

The ASX200 continued its upward trajectory but had a pause at lunchtime before closing 0.4% higher to 5830 points after a similar move yesterday, which could be the start of something more substantial. The Aussie dollar has retraced slightly despite the positive risk sentiment, mainly due to overnight commodity price selloffs but also a lacklustre CPI reading. It’s currently just below the71 handle and rolling ATR resistance on the four hourly chart:

The economic calendar has three important releases to take note of tonight, starting with the EZ wide CPI print, then Canadian GDP finishing with the monthly DOE oil inventory report.