Here comes President Trump to save the day – so goes the refrain, even though the blame for this correction lays squarely in his ample lap. The idea of a better “deal” with China is giving stocks a boost across the region, with the Yuan now into a ten year low against the USD as the PBOC raise the fix ever closer to the 7 major handle.

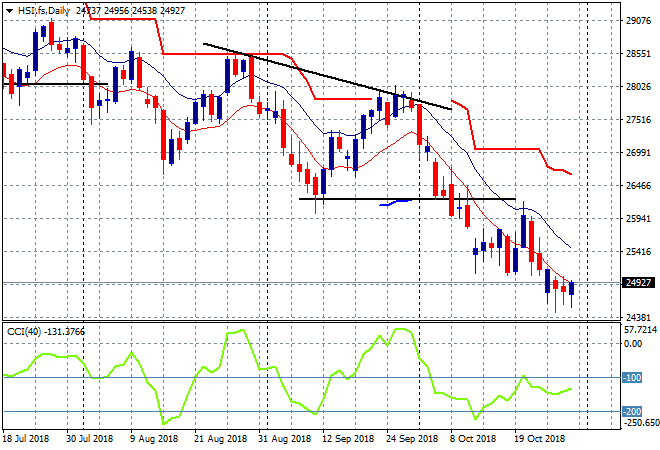

The Shanghai Composite is on a run, currently up 1.3% going into the close at 2574 points, still below key support at the 2600 level but could finish above there if this confidence (read: artifical sweetener) persists. The Hang Seng Index however did a minor retracment, down 0.2% or so to 24757 points, still well below the previous support level at 26000 points with intrasession lows indicating a possible bottom here on a deceleration curve:

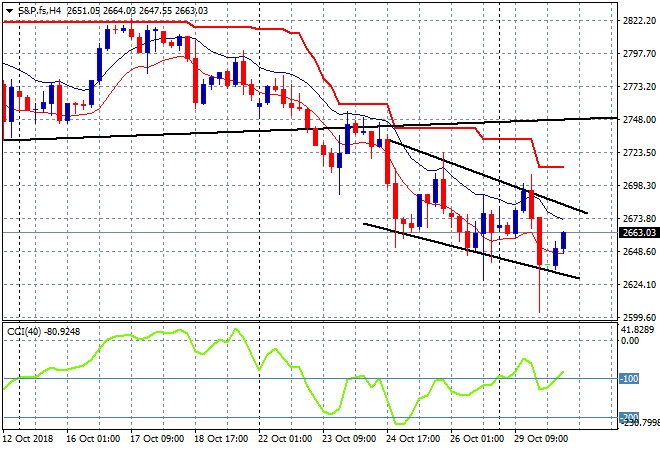

US and Eurostoxx futures are up slightly, with the four hourly S&P 500 chart showing a potential bottoming action near the 2640 level, if last night’s late session crash fill is to be believed. Watch the upper leg of this trend channel for a bounceback:

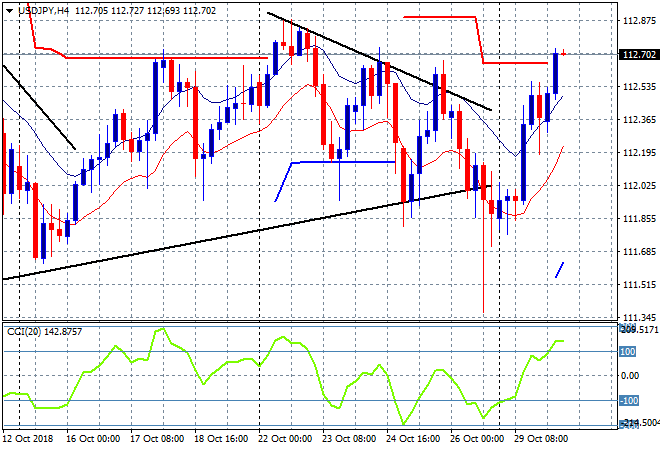

Japanese stocks were the best performers with the Nikkei 225 closing 1.5% higher at 21457 points, in a very convincing single day action. But is this due to the Yen selloff or just short covering? The USDJPY pair finally pushed higher, making another new daily high and almost matching last week’s intrasession high. I’m looking at the 112.80 level to come under pressure later tonight:

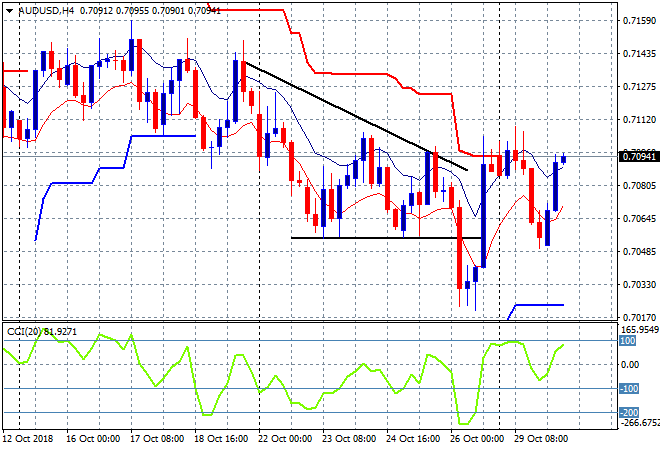

The ASX200 continues to do much better, closing 1.3% higher to 5805 points after a similar move yesterday, which could be the start of something more substantial. The Aussie dollar has also bounced back on the positive risk sentiment, almost reaching the 71 handle and rolling ATR resistance on the four hourly chart:

The economic calendar is full of major releases tonight, mostly Euro centric with German unemployment, Italian GDP and EZ wide CPI prints. It then switches over to the US for the latest consumer confidence figures.