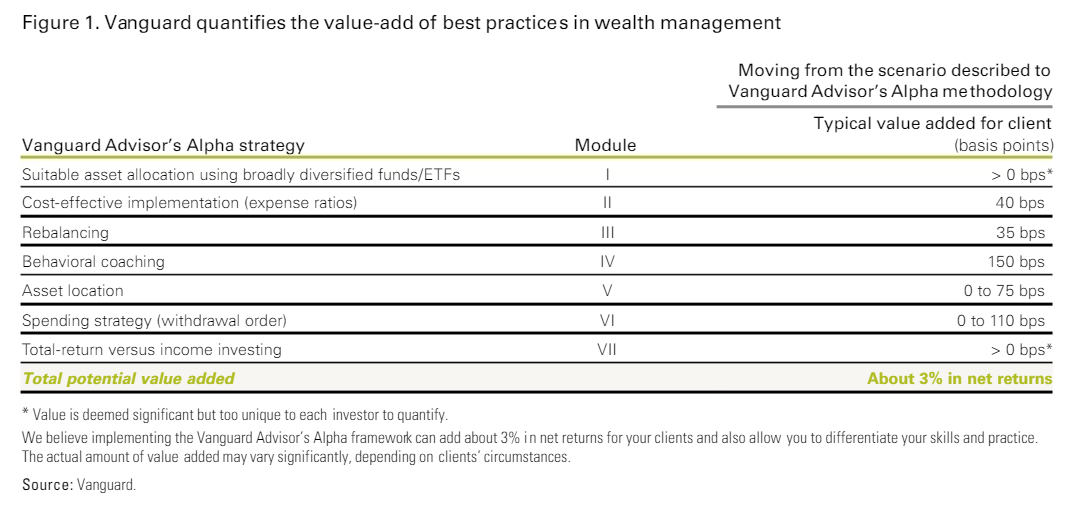

Trying to work out how much value an investment adviser adds to the investment process is difficult, but Vanguard has had a go at quantifying it anyway. Vanguard’s conclusion is that there are seven key areas adding to around 3% per annum (intermittently rather than every year) that could be added by an adviser (see here for full report).

Vanguard shied away from most of the investment side – understandably as it is difficult to make generalisations.

Most of the gains Vanguard saw were from either tax structuring (V and VI in the list below) or from fixing common investor behavioural biases (III, IV and VII). And this ties with what I see as the core strengths of most good financial planners: (a) to structure assets in a tax effective manner and (b) to act as a guide/mentor/psychologist for investors – explaining complexities, steering investors clear of the worst investments and talking investors out of succumbing to greed or fear.

Source: Vanguard

Asset Allocation:

Vanguard understandably cop out of having a number on Asset Allocation and just say that an adviser’s impact is greater than zero.

Most of the research agrees asset allocation is the most important decision an investor has to make for investment returns. The issue that Vanguard missed, in my opinion, is that there are two different types of asset allocation: strategic or tactical.

Strategic asset allocation is structuring an investor’s assets to match their risk profile, whereas Tactical asset allocation is the practice of switching out of overvalued asset classes into undervalued asset classes.

Strategic asset allocation can be done by most financial planners (including online robo-advisers), and most financial planning companies have extensive systems to make sure that clients don’t end up in the wrong asset classes.

Tactical is more difficult. While there are some financial planners who can do tactical asset allocation, my view is that you are more likely to get a good result using an investment manager who has a full-time job doing asset allocation rather than a planner doing it part time while managing a full book of clients.

Tax structuring

The estimates are based on US tax issues, but the same applies in Australia. If you take into account pension eligibility and superannuation, you will probably find the impact to be greater in Australia.

Many accountants can perform this role as well. You probably shouldn’t be doing this part yourself.

Investor Biases

There are three parts to this: rebalancing assets back to target weights (reducing the risk of the portfolio), investor behaviour (preventing investors from succumbing to greed at the top of the market or fear at the bottom) and total return investing (not getting hung up on yield).

These are all things that investors can potentially do themselves. But most investors will do it badly. I blogged recently about the Nervous Investor:

The main factor is investor behaviour. When markets wobble, investors tend to sell or sit on their cash. When markets have been performing well, investors tend to invest their cash.

From a risk perspective, this might seem reasonable to the Nervous Investor – buy when risks seem low and sell when risks seem high.

But, from a return perspective, it is exactly the wrong strategy: buy high, and then sell low.

Your brain is actively working against you

What is clear from the studies is that the average investor in the heat of the moment makes poor investment decisions.

The media doesn’t help – they generally only report two things: (1) the markets are up a lot and you should have bought last week, get in quick before you miss out (2) the markets are down a lot and you should have sold last week, sell now before you lose the lot

Getting perspective is difficult, especially if you rely on newspapers, financial TV or stock brokers. The first two are in the entertainment business and so creating an exciting story trumps any obligation to give you a realistic perspective. Stockbrokers are in the business of making money from turnover, so convincing you to buy one day and sell a few weeks later trumps any obligation to give you long-term advice.

Some investors will be able to overcome these inherent biases and do it themselves. Most investors can’t.

Investors used to have three options to overcome the inherent biases:

- Do it yourself. This may seem like the cheapest option but can easily wind up being the most expensive option.

- Use a planner. The most expensive option, useful for people who want high service and someone to call and talk to about issues

- Use a robo-advisor. Much cheaper than a planner, but you only get strategic asset allocation.

Warning: Shameless self-promotion. We started the MB Fund to add a fourth option – costs that are much closer to robo-advice than planning, including tactical asset allocation as well as strategic, offering full transparency and frequently blogging to fill the information gap.

————————————————————–

Damien Klassen is Head of Investments at the Macrobusiness Fund, which is powered by Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.