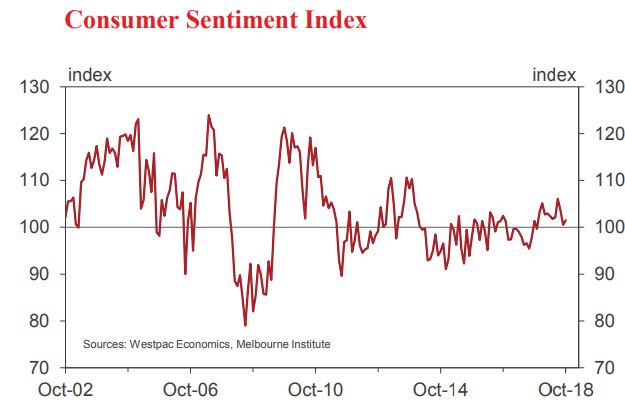

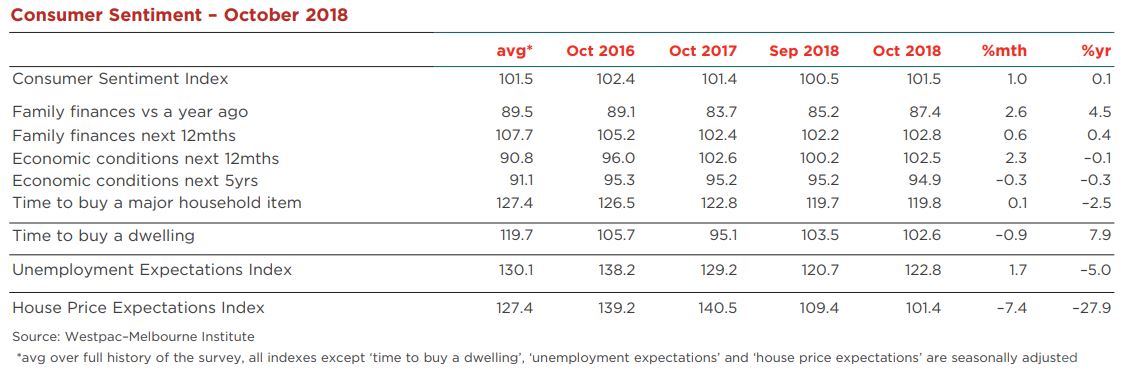

• The Westpac Melbourne Institute Index of Consumer Sentiment rose 1% to 101.5 in October from 100.5 in September.

This month’s small gain follows a 5.2% fall through August and September. During that period the boost from the tax cuts announced in the May budget had faded while the leadership change; mortgage rate increases; declining house prices and rising petrol prices were weighing on confidence.

It is encouraging that these negatives seem to have, at least for the time being, run their course. Several positives have likely helped stabilise the Index, including strong economic growth, a solid labour market and ongoing recoveries in the previously weak mining states.

The net effect has seen the headline index holding slightly above the 100 line indicating that optimists are just outnumbering pessimists. The slight ascendency of optimists has been the case for 11 consecutive months since December 2017. That contrasts with the previous 12 months between December 2016 and November 2017 when the Index registered below 100 for 11 of those 12 months.

Concerns around interest rates and house prices are still apparent. The sub-group detail showed sentiment amongst households with a mortgage continued to weaken in October, dipping a further 0.8% to be down 6.4% over the last two months. Interestingly, the breakdown by voter group suggests some of the negative sentiment impact from the change in Prime Minister in late August may have reversed with confidence amongst those identifying as Coalition voters recovering about two thirds of the 6.4% drop recorded in September.

Most index components recorded small gains in October. Assessments of family finances showed the most promising revival. The ‘finances vs a year ago’ sub-index rose 2.6% to be comfortably above levels this time last year, albeit still a couple of percentage points below the highs seen earlier this year. The forward view is less convincing. The ‘finances, next 12 months’ sub-index only edged up 0.6% and is 4.1% below its high following the announcement of the tax cuts in the Budget in May.

Consumer expectations for the economy also showed mixed moves. The ‘economic outlook, next 12 months’ subindex posted a solid 2.3% rally but longer term expectations continued to soften. The ‘economic outlook, next 5years’ sub-index is now down 9.1% from the five year high recorded back in July.

Spending-related sentiment showed little change on the relatively downbeat tone in recent months. The ‘time to buy a major household item’ sub-index inched 0.1% higher but is still around the lowest levels seen since November last year.

Labour market expectations, which were a notable bright spot in the weak September survey, softened a touch in October. Despite this, the index still shows a clear improvement from the softer reads through June-July, August with a solid 5% improvement on a year ago. Most of this is coming from a more balanced performance across the major states, with a particularly dramatic turnaround in labour market expectations in Western Australia.

Consumer views around housing continue to deteriorate. The ‘time to buy a dwelling’ index slipped a further 0.9% following September’s 4.8% fall, unwinding all of the 5.5% gain in August. Despite the weakening, buyer sentiment is still well above the lows seen through mid-2017.

Consumer expectations for house prices posted another sharp fall in October. The Westpac Melbourne Institute Index of House Price Expectations dropped 7.4% to 101.4, taking the index below its 2015 low point to the weakest level since the first month the survey question was run, in May 2009. The state detail showed a particularly sharp 20.3% drop in Victoria, suggesting the price correction in Melbourne, which has been slower to come through than in Sydney, is starting to bite.

House price expectations are now particularly weak in NSW (87.1) and Victoria (88.0) although in both cases state indexes are still above the prints seen in WA when the Perth market was moving into its prolonged price correction in 2015-16 (the WA Index averaged below 80 through this period). In contrast, price expectations remain bullish in Tasmania (142.8) and are holding at positive levels in Queensland (130.1).

The Reserve Bank Board next meets on November 6.

While the Reserve Bank remains confident about the outlook for growth, predicting 3.25% growth in 2019, the Governor continues to emphasise that the Bank remains uncertain about the outlook for consumer spending. Forces linked to higher interest rates; weak wages growth; household budget pressures and falling house prices conspire to complicate that outlook. All of those factors are apparent in the various sub-indexes in today’s report.

However with reads just above the 100 level for the overall Index households remain settled. A strong labour market is undoubtedly a key factor.

With inflation benign and these conflicting forces playing out it is logical that the Reserve Bank will keep rates on hold. With global developments adding a further dimension of uncertainty Westpac confirms its view that the Bank will keep rates on hold through 2018; 2019 and 2020.

Undoubtedly the job market is the key and as it fades with house prices will be the trigger for big falls ahead in confidence.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.