King dollar returned last night, breaking out and setting its sights on the 2017 highs. CNY hit new lows. EUR is in trouble:

Despite this, AUD rallied like a mad thing, proof that the epic market short is solid support at current prices:

Gold was hammered:

Oil too:

And base metals:

Big miners eked out gains:

EM stocks rebounded:

US junk too, EM not so good:

Treasuries sold:

And bunds:

Italy reheated on weak GDP:

US stocks finally enjoyed some relief:

Westpac has the wrap:

Market Wrap

Global market sentiment: US equities rose, while key commodities oil and copper fell amid US-China trade concerns. The US dollar benefitted from disappointing Eurozone data and a Brexit warning from S&P. Given all that, AUD and NZD performed well.

Interest rates: The US 10yr treasury yield firmed slightly from 3.10% to 3.12%, the 2yr yield up from 2.83% to 22.84%. Fed fund futures yields priced the chance of another rate hike in December at 75%.

FX: The US dollar index is up 0.4% on the day. EUR fell from 1.1385 to 1.1341, hurt by disappointing GDP data. GBP was the day’s underperformer, falling from 1.2810 to 1.2896 – the lowest since mid-August – amid Brexit concerns. Rating agency Standard & Poor’s said that the chance of a no-deal Brexit has increased, and that scenario would cause a recession and trigger a rating downgrade. USD/JPY rose from 112.60 to 112.98. Outperformer AUD extended earlier gains, from 0.7090 to 0.7122. NZD also performed well, given the firm USD, rising from 0.6540 to 0.6573. AUD/NZD ranged sideways between 1.0820 and 1.0840.

Economic Wrap

Eurozone economy slowed sharply in Q3. GDP grew just 0.2% (vs 0.4% expected), the weakest quarter in five years, taking the annual rate down to a subdued 1.7% from 2.2%. Admittedly temporary factors such as a sharp fall in German auto production as new emission standards were implemented depressed activity, but business surveys suggest underlying momentum is slowing into Q4. The European Commission’s economic, business, industrial and services confidence gauges all deteriorated more than expected in October, edging down to their weakest readings since mid-2017, underscoring a more cautious mood in the Eurozone. German preliminary CPI matched expectations, +0.1% in Oct, lifting the annual pace to 2.4% from 2.2%.

US Conference Board’s consumer confidence index rose to an 18-year high of 137.9 in October from a downwardly revised 135.3, a solid labour market and tax cuts more than countering the stock market rout and elevated trade tensions. Both present conditions and expectations rose while confidence about the labour market hit its highest levels since 2001.

Event Risk

NZ: Monthly business confidence (ANZ) fell to a 10-year low in August, but did bounce slightly in September.

Australia: Q3 CPI is expected to rise 0.5% with the core measures up 0.4%. Westpac’s forecast for core inflation is lower than consensus, anticipating a 0.3% rise. The big unknown for this quarter is the impact of changes to childcare rebates.

Japan: The BOJ policy meeting will be watched for any tweaks to the bond buying program and associated Yield Curve Control policy. The quarterly outlook report will also be released.

China: Official NBS PMI’s are anticipated to remain around current levels with manufacturing last at 50.8 while non-manufacturing has been more positive, last at 54.9.

Euro Area: Sep unemployment rate is seen to hold at 8.1% as slack in the labour market gradually declines. Oct CPI advance is expected to show annual headline inflation up to 2.2% from 2.1% and a lift in core inflation to 1.1% from 0.9%.

US: Oct ADP employment is out ahead of nonfarm payrolls on Friday. Q3 employment cost index is anticipated to rise 0.7%, holding the annual pace at 2.8%. The US Treasury make their quarterly refunding announcement.

These variables – a weak EUR and CNY plus powering DXY – are the near perfect conditions for big AUD falls. But the ‘risk on’ rally protected it instead, as well as the huge market short. However, if such conditions persists, and they are our base case, then the AUD will buckle.

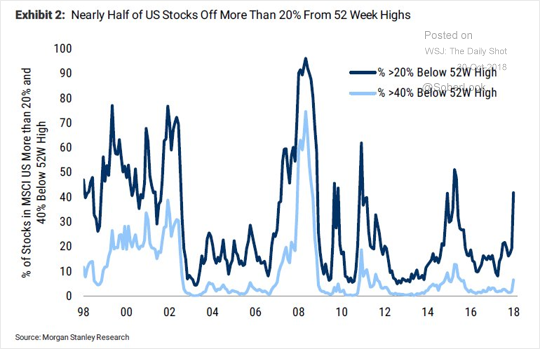

Meanwhile, the debate about stocks persists. Internal market damage is nasty:

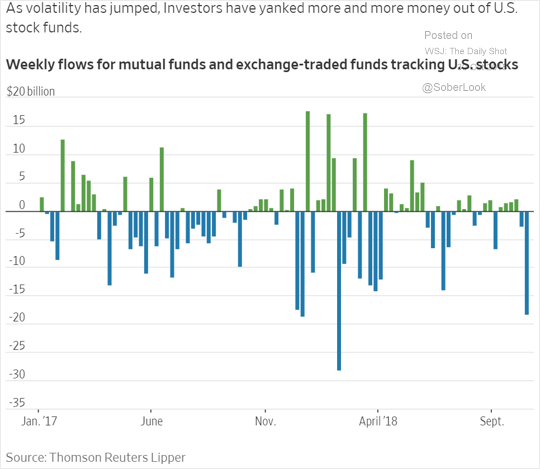

Equity flows are interrupted:

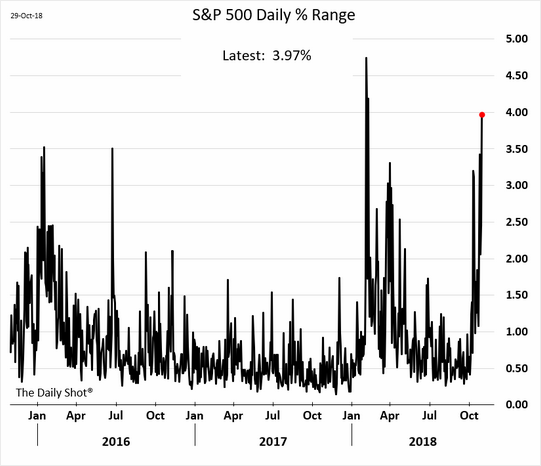

Volatility is on the march:

It’s bad globally:

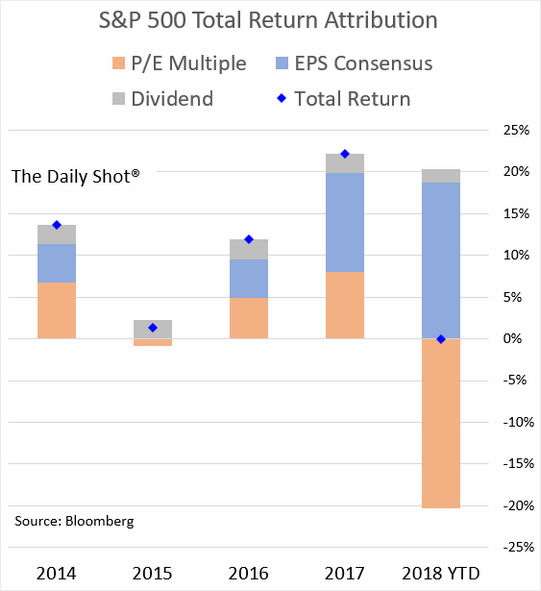

It’s all about multiple compression suggesting rising exogenous risk:

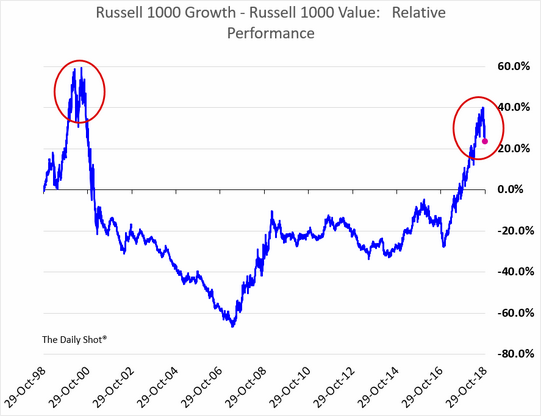

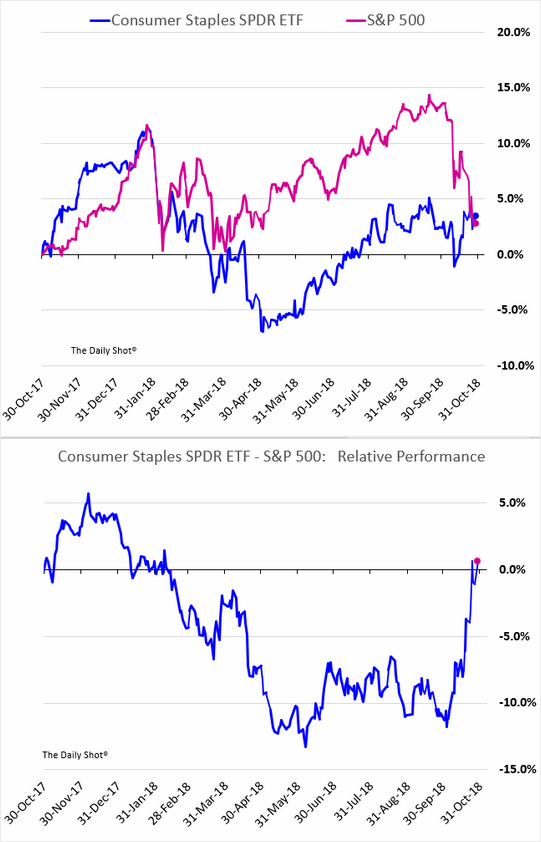

Growth worries are paramount:

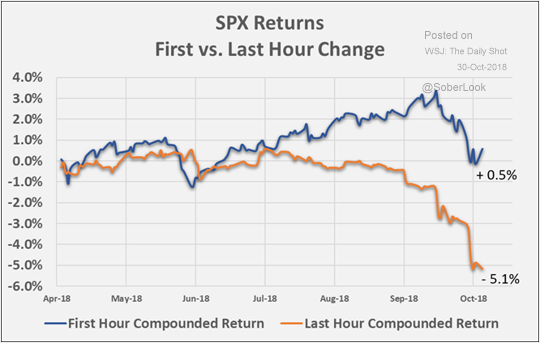

And it’s all being made worse by the proliferation of quant strategies that rebalance late in the day:

Which is where JPM quants comes in:

Did the macro and fundamental outlook deteriorate enough to justify this extreme swing in investor positioning?

In October, US GDP surprised expectations to the upside, core PCE remained steady, and ~80% of US companies reporting Q3 earnings beat analyst expectations that were formed before the sell-off, while forward guidance remains largely unchanged. Given the weakening economy in China and poor market performance in the US, there may be an increased (rather than decreased) probability of November progress on trade.

With investors positioned defensively, and leverage rapidly coming out of system, there is an elevated risk of market reversion into year-end. Investors should keep this risk in mind – namely that an October ‘rolling bear market’ turns into a ‘rolling squeeze higher’ into year-end. This would cause further underperformance of active managers relative to broad indices.

First, we note that October month-end will lead fixed weight asset managers to increase their equity exposure. Given the size of the move in October (largest since Feb 2009), that could contribute to ~1-2% of upside market pressure (based on the historical beta of month-end reversion).

Buyback activity is expected to increase significantly going forward (~$200bn realization run rate to year-end).

We also expect volatility to decline into year-end, which should prompt systematic investors to re-build equity positions (~$100Bn).

Finally, any progress on trade could result in discretionary inflows, reduction of current elevated short positioning, and year-end performance chase.

It appears the worst may be over for now. But such a sell down looks more than just a hiccup. The EPS growth outlook is still excellent and unperturbed by the volatility and more stimulus is coming but so is more tightening. Treasuries have not pulled back that much during the sell-off.

We know it is late cycle and the stakes are rising.