But AUD was smashed against everything anyway hitting new lows against GBP, EUR and USD:

Market positioning was unchanged at a very short -72k:

Advertisement

It also fell against EMs:

It is interesting to note that the AUD keeps falling despite a falling US dollar index (DXY) which suggests the local currency weakness is as much about an Australian de-rating as it is a US boom:

Advertisement

Gold was up a bit:

Oil down:

And base metals:

Advertisement

Miners were hit hard:

EM stocks puked to new lows:

US and EM junk sent out a warning:

Advertisement

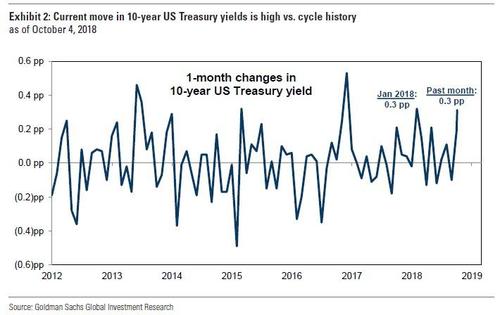

As Treasuries were flogged again:

And bunds:

Italy won’t go away:

Advertisement

Stocks were hit again:

The driver was US jobs which came in cold but good revisions and hurricane distortions were enough to keep the market hawkish:

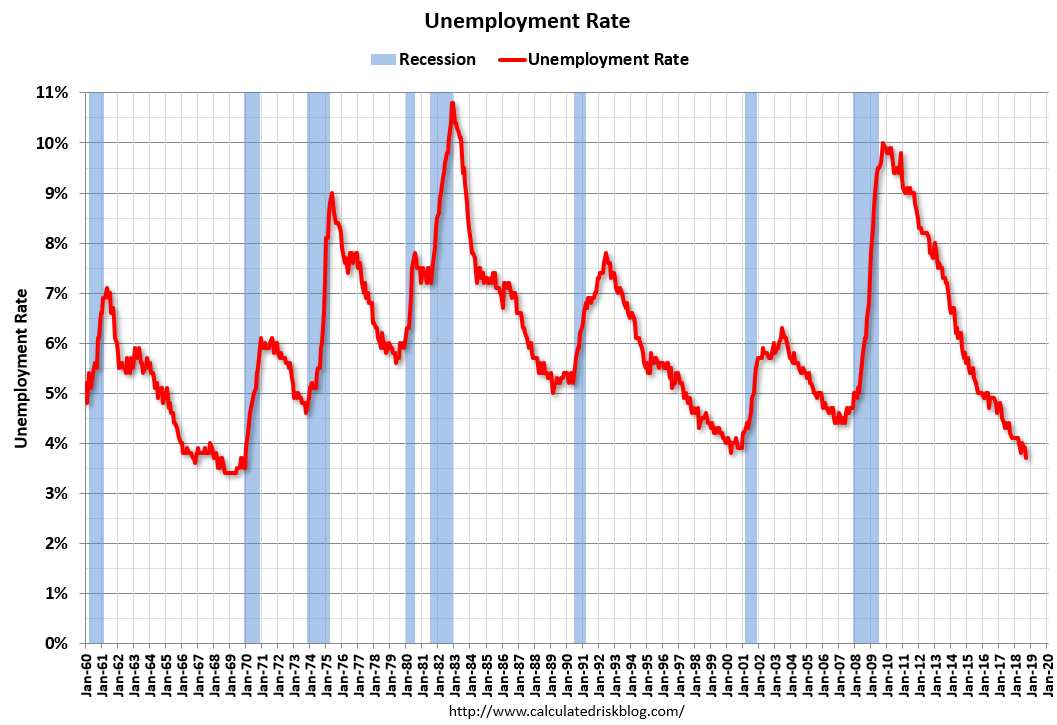

The unemployment rate declined to 3.7 percent in September, and total nonfarm payroll employment increased by 134,000, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in professional and business services, in health care, and in transportation and warehousing.

Hurricane Florence affected parts of the East Coast during the September reference periods for the establishment and household surveys. Response rates for the two surveys were within normal ranges.

… The change in total nonfarm payroll employment for July was revised up from +147,000 to +165,000, and the change for August was revised up from +201,000 to +270,000. With these revisions, employment gains in July and August combined were 87,000 more than previously reported.

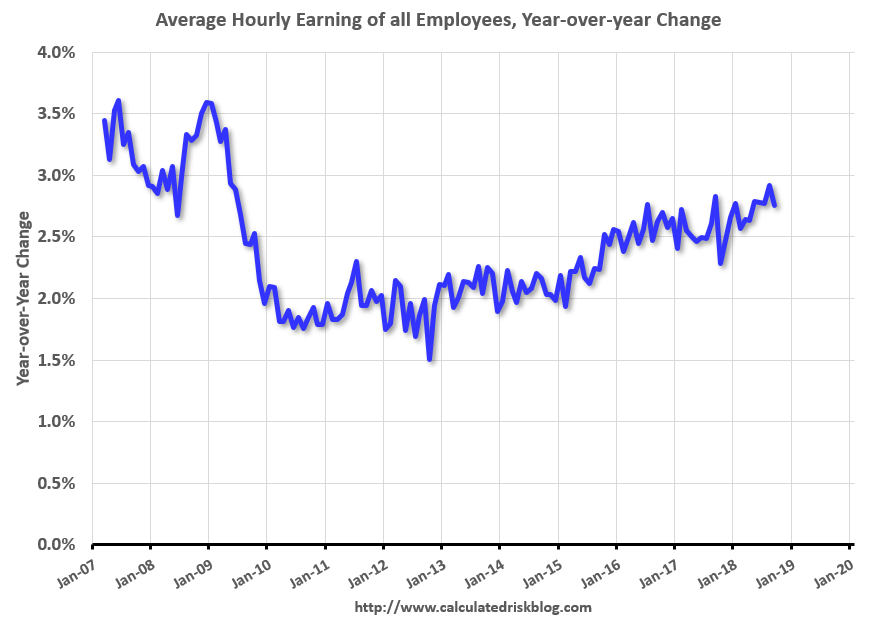

…In September, average hourly earnings for all employees on private nonfarm payrolls rose by 8 cents to $27.24. Over the year, average hourly earnings have increased by 73 cents, or 2.8 percent.

Advertisement

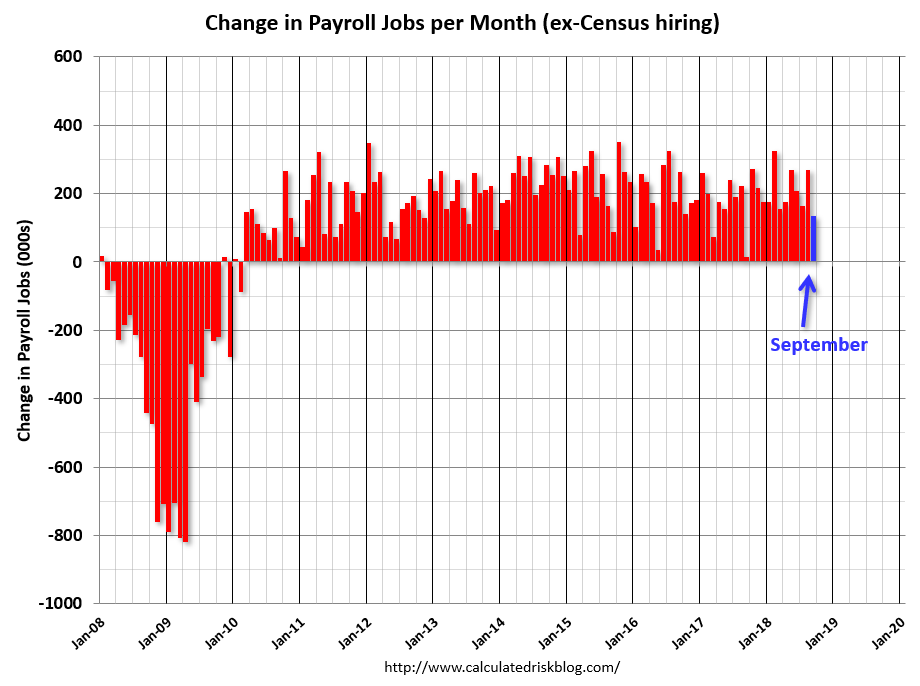

Charts from CR. Headline was soft:

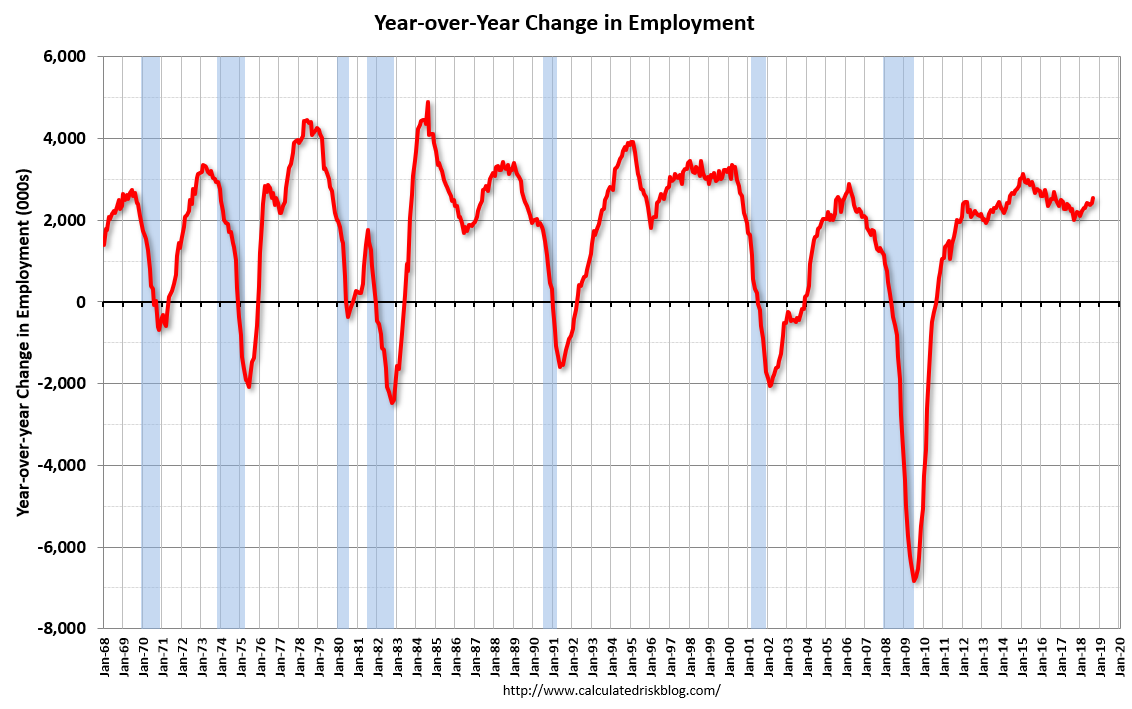

Jobs growth accelerated:

The unemployment rate hit a 50 year low:

Advertisement

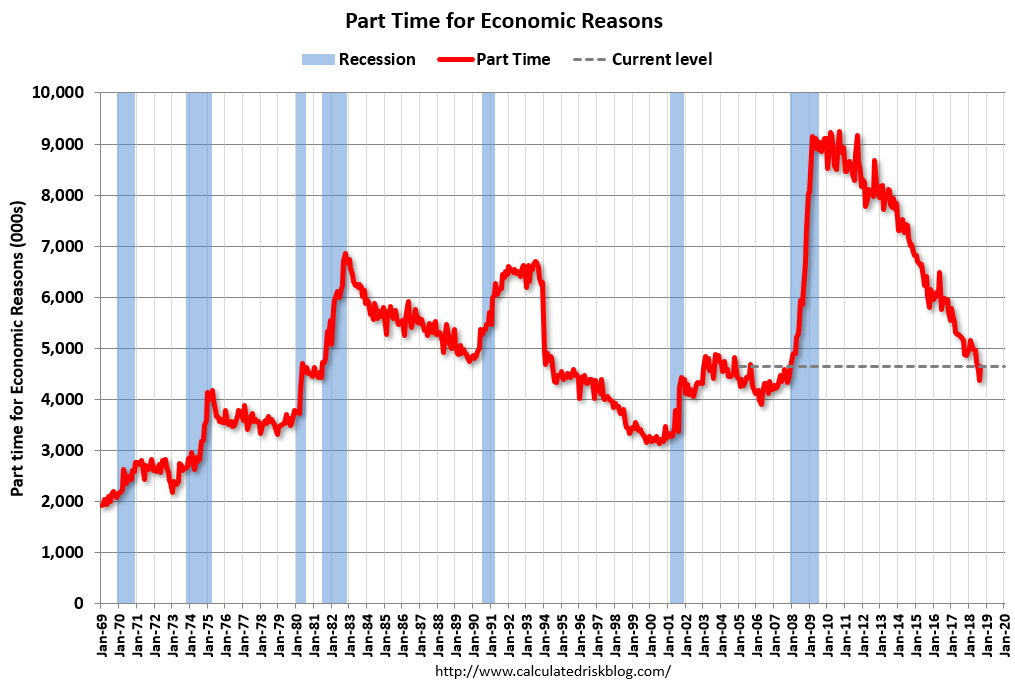

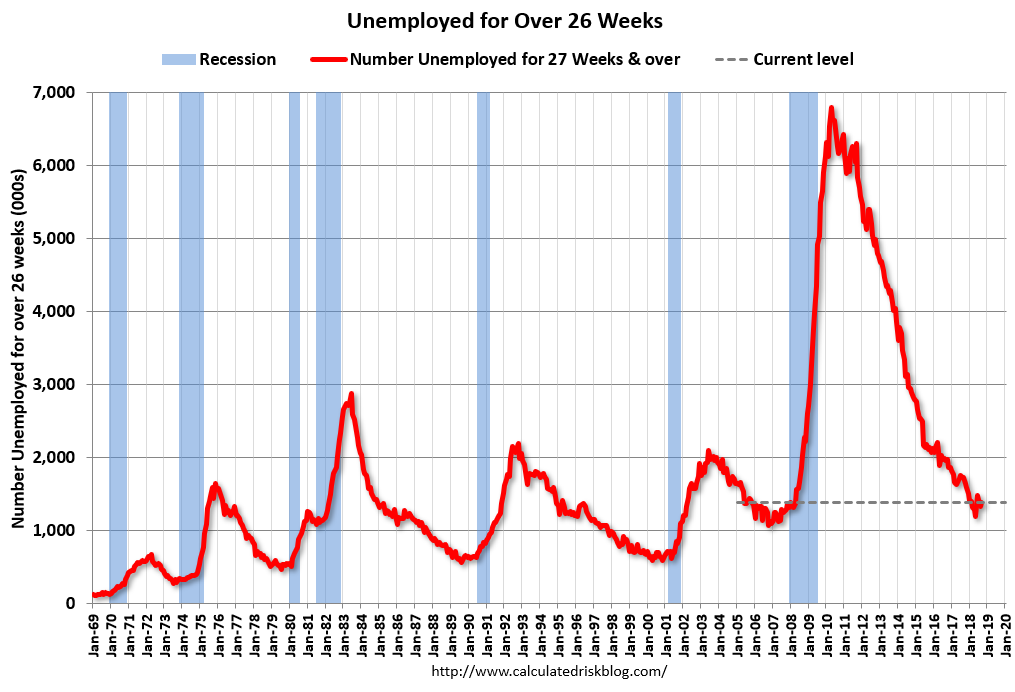

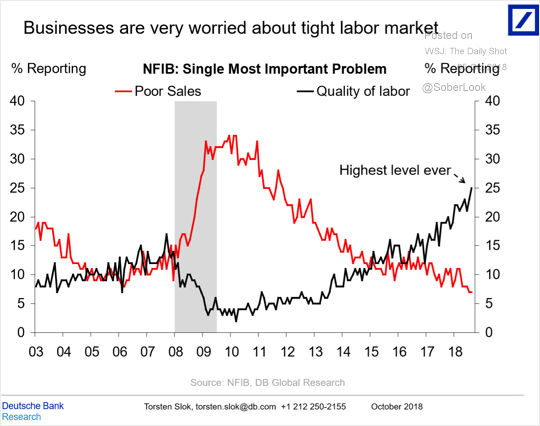

But there is still shadow slack:

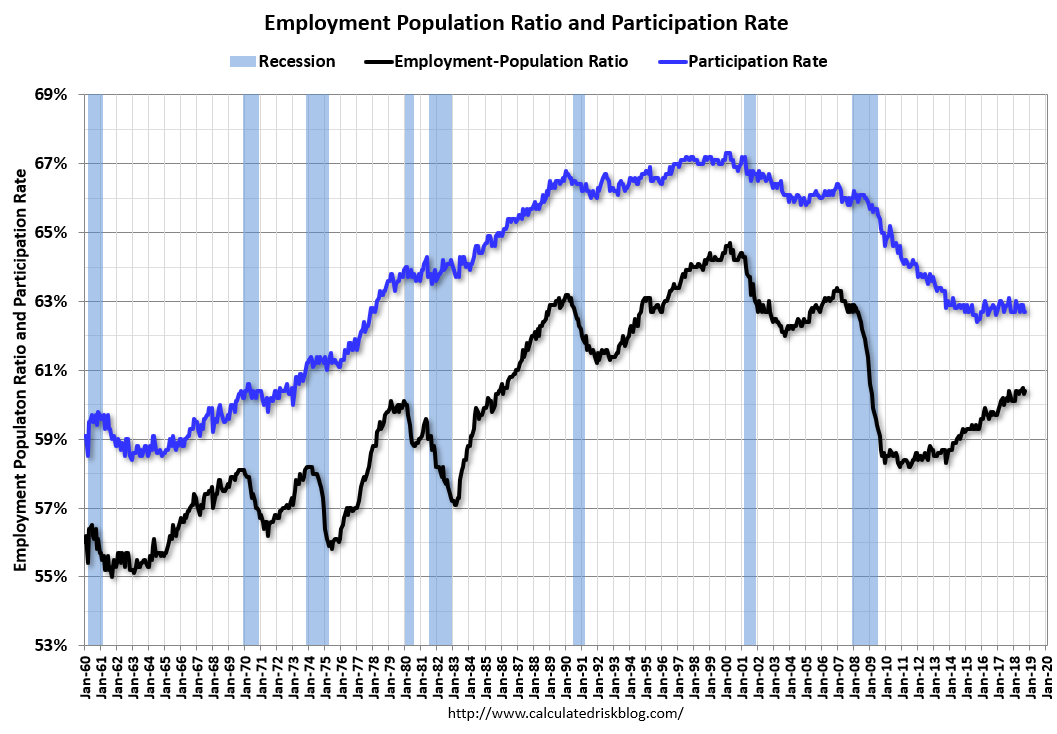

Analytical measures are still improving:

And wages fell back but remain in an up trend:

Advertisement

Which is likely to continue:

Still looks like Goldilocks to me. Good jobs growth and solid wage gains to boost demand yet nothing too extreme to upset either the Fed or crimp corporate margins. Via Goldman:

Advertisement

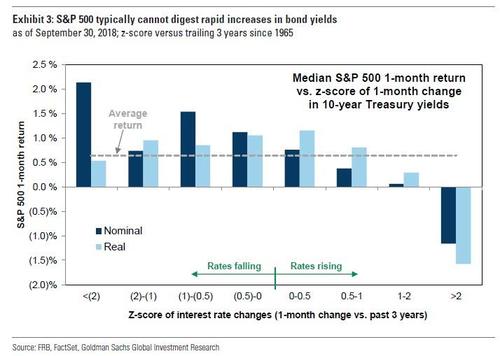

When bond yields have surged by 1-2 standard deviations in a month (~20-40 bp today), S&P 500 returns have typically been flat. When bond yields have risen by more than 2 standard deviations in a month (~40+ bp), S&P 500 returns have typically been negative (see Exhibit 3).

S&P 500 valuation multiples stand at near-record highs. Consistent with prior Fed tightening cycles, we expect higher interest rates will constrain further valuation expansion.

Correct. It is the pace of Treasury selling that is the key. I don’t see a reason for yields to run away but that has been the pattern when markets throw an inflation tantrum so we might have see some volatility before lowflation calm returns.

Advertisement

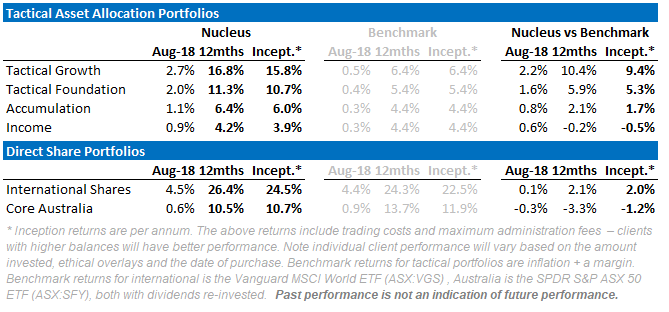

David Llewellyn-Smith is chief strategist at the MB Fund which is long US equities that will benefit from a falling Australian dollar so he is definitely talking his book. Below is the performance of the MB Fund since inception:

If the ideas above interest you then contact us below.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

S&P 500 valuation multiples stand at near-record highs. Consistent with prior Fed tightening cycles, we expect higher interest rates will constrain further valuation expansion.