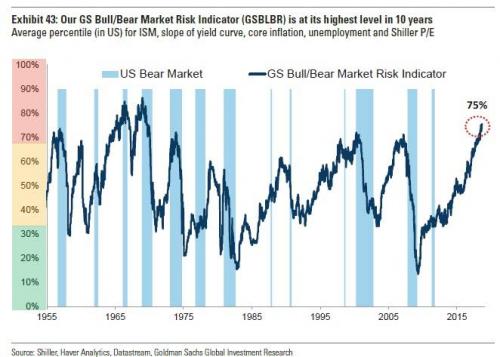

All of these variables are related. Tight labour markets are typically associated with higher inflation expectations. These, in turn, tend to tighten policy and weaken expectations of future growth. High valuations, at the same time, leave equities vulnerable to de-rating if growth expectations deteriorate or the discount rate rises, or, worse still, both of these occur together.

To aggregate these variables in a signal indicator, we took each variable and calculated its percentile relative to its history since 1948. For the yield curve and unemployment we took the lowest percentiles relative to history, while for the other indicators we took the highest. We then took the average of these.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.