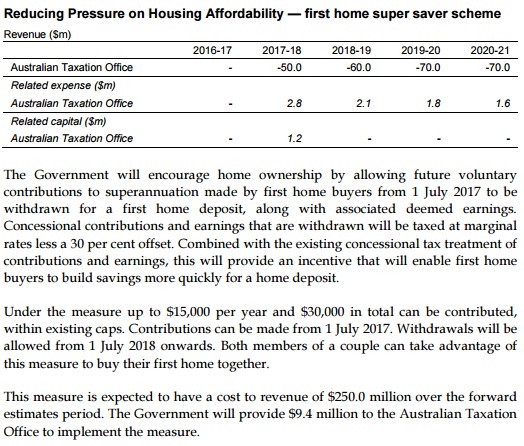

Desperate to keep the East Coast property bubble going, the Turnbull Government last year passed legislation to allow first-home buyers (FHBs) to use up to $30,000 of voluntary super contributions for a housing deposit. The scheme was announced as part of a ‘housing affordability’ package announced in the 2017 Federal Budget.

However, the re-gigged First Home Savers Account is rather weak. It was only projected to cost the Budget $250 million over the forward estimates (see below) – probably an overstatement given Labor’s scheme had such a poor take-up rate and just 2% to 3% of young people currently salary sacrifice additional funds into superannuation.

Advertisement