Stocks have retraced further here in Asia in the wake of last night’s third rate rise for the year by the Federal Reserve with the USD moving swiftly higher against the major currencies in the last couple hours. This maybe in relation to the Italian budget jitters or the reaction to the first rate hike in over a decade by the HSBC in Hong Kong, or the growing distress over what can only be described as a shambling press conference by President Trump.

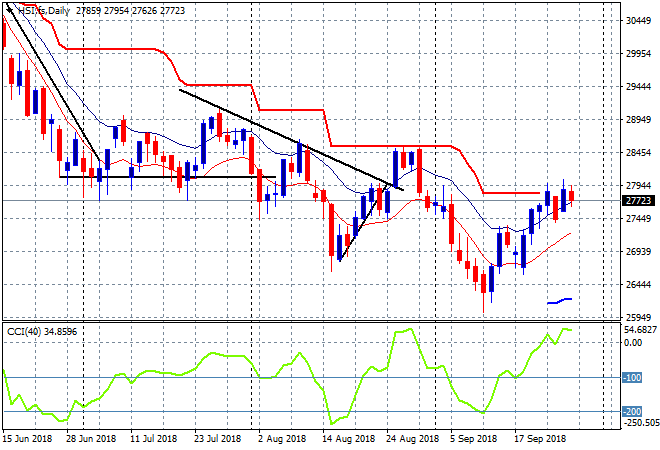

The Shanghai Composite has again retreated below 2800 points, unable to build confidence here by falling some 0.4% or 10 points to 2794. The Hang Seng Index is off only 0.2%, down to 27759 points, still dicing with overhead ATR resistance. There is potential here if it can cross above key resistance at the former daily highs at 28500 points, but momentum is lacking:

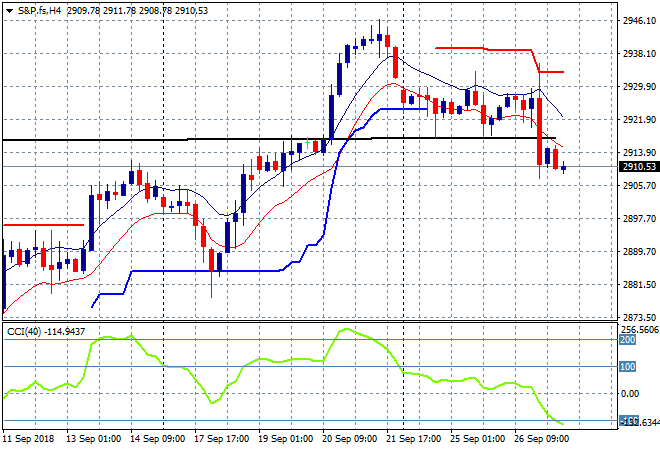

S&P futures have fallen sharply in the last couple of hours with the Eurostoxx issues also off 0.5% indicating a rough session ahead tonight:

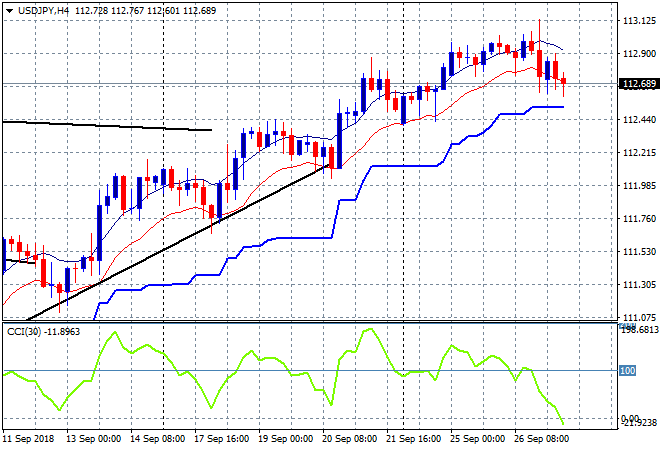

Japanese stocks retreated by nearly 1% on both bourses as Yen was stronger throughout the session on the safe haven bid, with the Nikkei 225 closing at 23796 points. The USDJPY pair has rejected overhead resistance above at the 113 handle, falling further further after recent strength evaporated on the Fed rate decision last night. I’m watching the 112.50 level at ATR support closely:

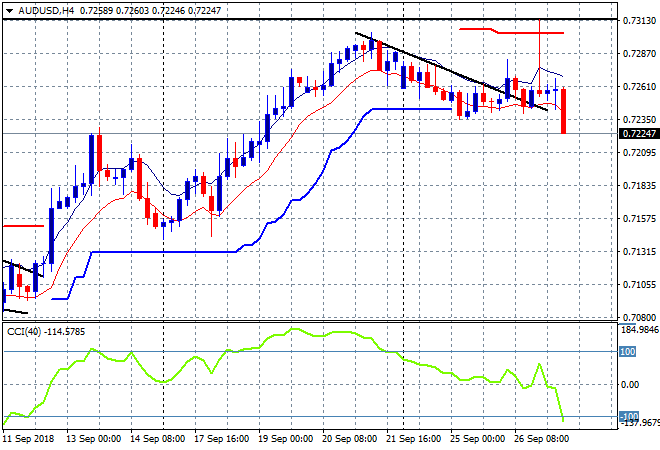

The ASX200 has slipped again, falling some 12 or so points to 6181 points, still unable to climb above former support now resistance at the 6200 point level. The Aussie dollar has shrarply fallen in the last couple of hours, almost hitting the 72 handle and making a new low for the week. This is ominous indeed with my target below at 71.30:

The economic calendar includes some important releases tonight, with the European CPI print for September first and foremost, then US 2Q GDP and durable goods orders.

Having a long weekend – can’t beat this weather combined with raising a glass to Queen Lizzie – so I’ll see you all on Tuesday.