The Bank of Japan kept guidance and its policy intact today at the latest meeting, with no negative impact on Yen or stocks, as the rest of Asia continue the risk on mood from overnight markets. While the Yuan appreciated slightly offshore today against USD, the new round of tariffs has not filtered through to either currencies or shares as traders put aside any risk concerns of the growing trade war.

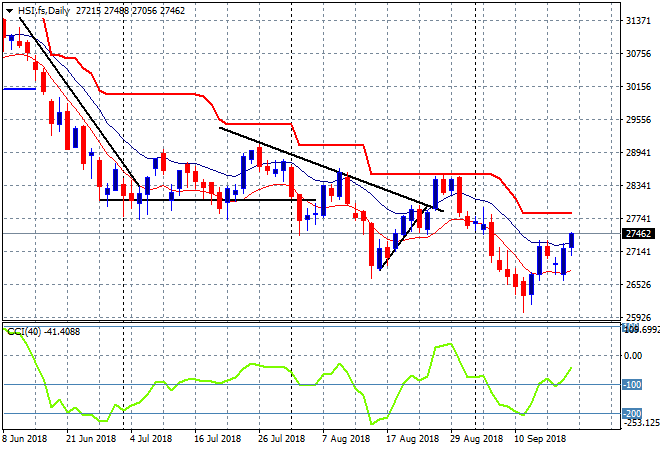

The Shanghai Composite has followed through on yesterday’s bounceback, currently up 1.2% going into the close at 2734 points, getting through short term resistance at the 2700 point level. The Hang Seng Index is up even further, closing 1.4% higher to 27459 points, finally able to get out of its current funk and above the high moving average on the daily chart. This sets aside short term resistance for a run up to at least 28000 points:

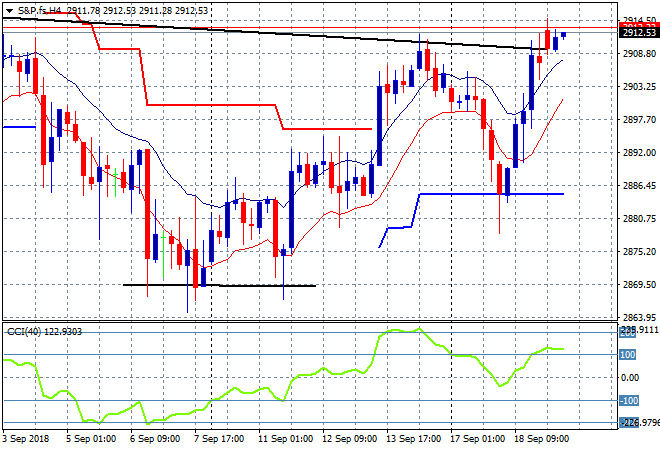

S&P futures have moved up alongside the Eurostoxx issues, the later up 0.2% as we go into the European open. The four hourly chart of the S&P500 shows a break above the previous high last week which means we should see a new rally forthwith:

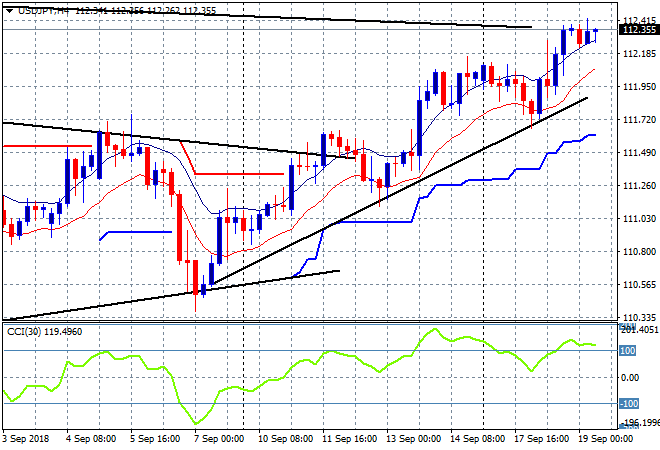

Japanese traders are quite ebullient here with the Nikkei 225 closing 1% higher to 23672 points. The USDJPY pair is still maintinaing last night’s session high at the 112.30 level in the wake of the BOJ meeting and is all set to make new highs when the City opens, even though price is a little overbought:

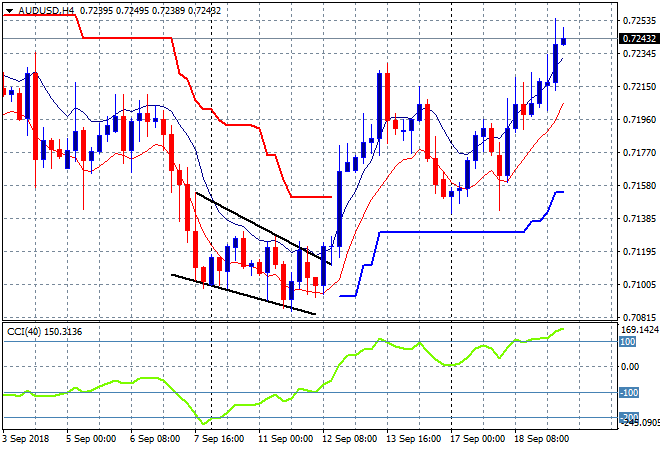

The ASX200 remains the laggard, up only 0.4% and the worse performer in Asia as the Aussie dollar soars higher, closing at 6190 points. The Aussie dollar is on a tear in an unsustainable burst higher, now up to the 72.40 mark versus the USD, way above last week’s intrasession high. Note that price action here is signalling a reversion to mean so watch for a reversal later tonight:

The economic calendar continues with three releases of note tonight, with the UK CPI print for August, another speech for ECB President Mario Draghi in Berlin and finally the DOE crude oil inventory report.