A slightly better day here in Asia, but Chinese stocks remain in a funk as they stare down the short barrel of Trump’s hands on the tariff trigger. Moving into a week of central bank meetings and following Friday’s NFP print, risk markets – particularly currencies – are nervous, with all eyes on US stocks to keep making new highs after a temporary dip recently.

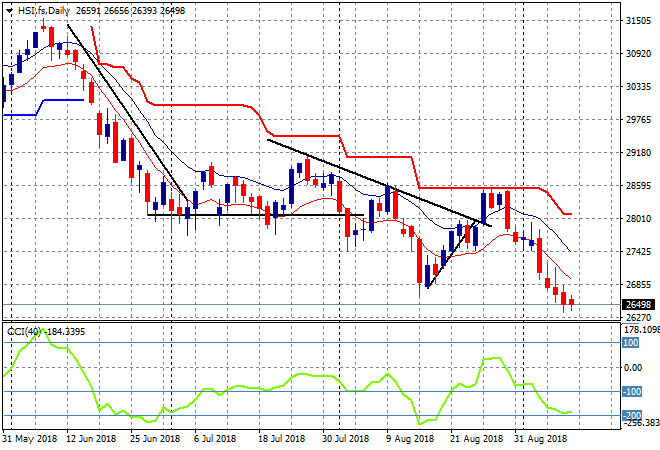

The Shanghai Composite was looking to finish the session only down a few points but has sold off sharply into the close, down 0.5% to 2657 points as continues its freefall. The Hang Seng Index is off as well but slowing down, closing 0.2% lower to 26542 points, making another new daily low as its correction continues:

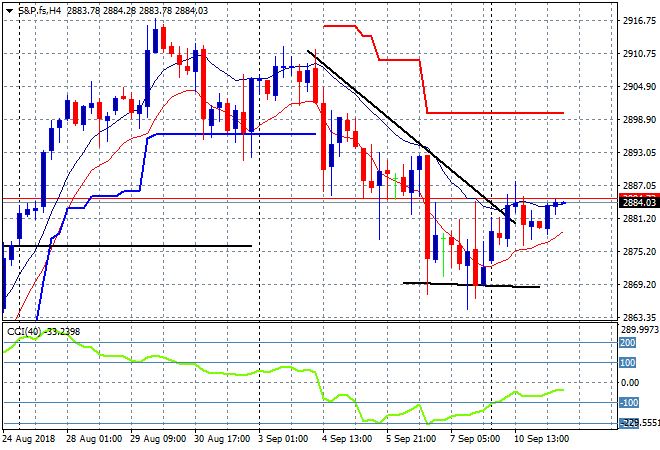

S&P futures are slowly building here while the Eurostoxx are up 0.2% indicating a followthrough on last night’s small blip higher on both sides of the Atlantic. The four hourly chart of the S&P500 is coming up against short term resistance at the 2887 level and could burst through tonight staging a comeback to the 2900 former high:

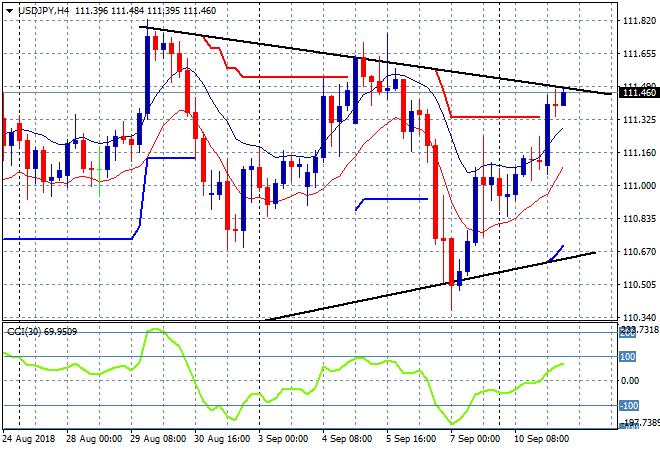

Japanese stocks have again outpaced the rest of the region as Yen was substantially weaker against USD, with the Nikkei 225 closing 1.3% higher at 22664 points, solidly bouncing off support. The USDJPY pair has gotten back above the 111 handle, recovering more than Friday night’s selloff. It’s now coming up to the midweek high at 111.60 that needs to be breached soon:

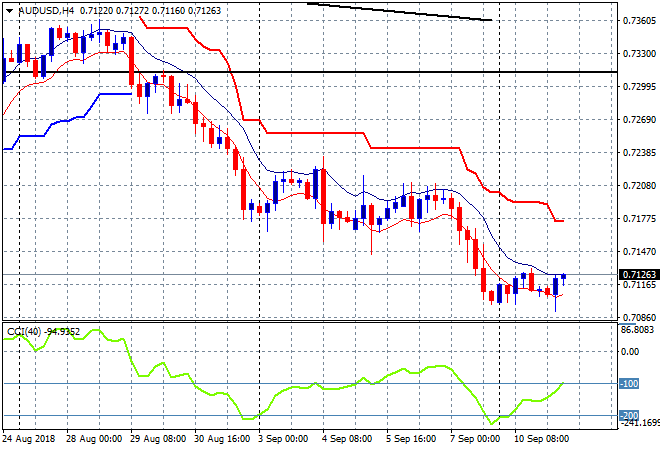

The ASX200 had a better than expected session, given the political turmoil fallout on business confidence, closing 0.6% higher to 6179 points. The Aussie dollar remains depressed but has not broken down entirely as it bounces along a temporary bottom here, still holding on vainly just above the 71 handle:

The economic calendar has one major release to watch tonight, the monthly German ZEW confidence survey that is usually Euro-sensitive.