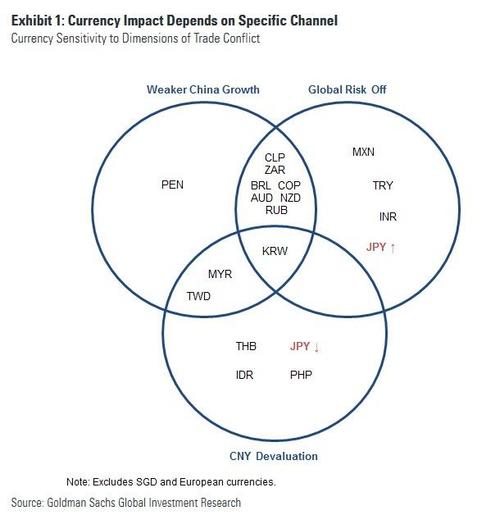

Via Goldman comes implications of the next phase of Trump trade war as tariffs mount to $200bn:

(i) by lowering expectations for Chinese growth,

(ii) by causing a general decline in risk tolerance and therefore weakness in riskier currencies, and

(iii) by weakening the Chinese Yuan relative to the US Dollar. Each of these channels has different implications for currency markets.

A broader pullback in risk assets affects a number of these currencies as well, but also other risk-sensitive EM exchange rates with smaller economic links to China. In contrast, CNY depreciation affects a different set of currencies — most notably Asian exporters that compete with China in third markets. Two currencies are particularly notable in this graphic: (i) the Korean Won, which ticks all of the boxes, and (ii) the Yen, which trends to depreciate alongside CNY weakness, but appreciate in times of falling global risk tolerance.

First, the Trump Administration has expressed its displeasure with USD strength, particularly against the CNY, and the PBOC has taken steps to stabilize the Yuan. In our view this implies that the “CNY devaluation” channel will be less significant this time around — with the Yuan remaining stable or depreciating only very gradually.

Second, market sentiment around EM assets has become much more fragile. This might imply that spillovers to EM currencies outside of Asia could be more meaningful.

Third, partly reflecting the prior point, valuations are much cheaper for many EM currencies as well as certain commodity prices (especially copper).

(i) sell USD/JPY, as the Yen’s strong response to a worsening risk environment would likely outweigh the effects of declining Chinese demand expectations and any modest weakening in the Yuan,

(ii) buy USD/KRW, which remains at the center of the storm, and

(iii) remain tactically cautious about high-beta EM FX, even for currencies outside the region. Long JPY/KRW would likely be the cleanest tail risk hedge.

AUD still going down.

David Llewellyn-Smith is chief strategist at the MB Fund which is long US equities that will benefit from a falling Australian dollar so he is definitely talking his book. Below is the performance of the MB Fund since inception:

Advertisement

If the ideas above interest you then contact us below.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.