The selloff in emerging markets deepened on speculation the U.S.-China trade war will escalate. Currencies slumped to their lowest level since April 2017 as Goldman Sachs Group Inc. said its models signaled further declines for some developing nations. Stocks also fell.

“Of course, valuations are best seen as a medium- to long-term signal for asset market performance, and are rarely a catalyst in and of themselves to spark stronger performance,” they wrote. “Nevertheless a significant cheapening could provide an anchor point for investors who can take the long-term view and a buffer to weather any volatility.”

It isn’t over by a long way. Let me show you a scary chart for how far EM stocks still have to fall:

Advertisement

That’s EM junk debt versus EM stocks. Notice how wildly dislocated they got after the 2015 Chinese stimulus. Notice as well that high yield debt stress is already approaching the 2015 lows yet stocks remain 30% above that episode. It will not end until the Fed is forced backwards and, possibly, Trump tariffs also unwind.

There is nothing but downside ahead in this chart for EM FX, debt, equities, commodities and the Australian dollar. JPM agrees:

EM FX weakness accelerated in August in absence of broader USD strength or higher US yields:

Second, is growing spillover from individual hotspots into broader EM FX

US trade policy … (JPM) conclude that the elevated tension and focus on trade issues we saw unfold throughout the second half of summer will persist well into the fall

Macro Trade Recommendations:

upward pressure on USD, CHF and to a lesser extent JPY is the inevitable outcome from a phase of de-risking in EM

Shorts in AUD and NZD remain a viable proxy in G10 space for the vicious circle that now confronts EM FX

Stay short EUR/CHF despite less worrying signals on the Italian budget but rotate from GBP/CHF into NZD/CHF as gamma risk from Brexit headlines is now quite punitive.

Advertisement

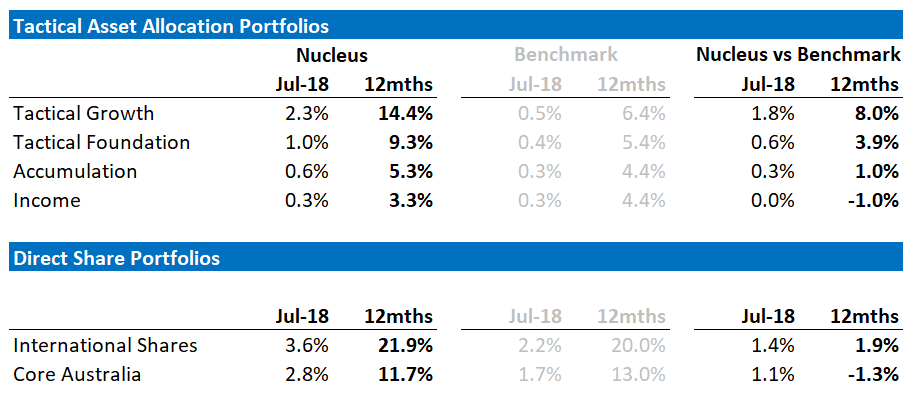

David Llewellyn-Smith is chief strategist at the MB Fund which is long US equities that will benefit from a falling Australian dollar so he is definitely talking his book. Below is the performance of the MB Fund since inception:

If the ideas above interest you then contact us below.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.