Global LNG export contracts are broken all of the time

From The Australian comes AGL:

Australia’s largest power generator, AGL Energy, has warned Victoria faces gas shortages in the early 2020s as supplies from Queensland dry up, with the problem to be made worse should Labor introduce a price trigger to limit export volumes and free up domestic supplies.

…“As we move into the 2020s, we do think there’s going to be physical constraints on supplying gas to southern markets,” said Mr Wrightson.

“But also the cost of coal-seam gas climbs higher and higher as all the easy gas is taken first and you move into the more expensive gases further out in some of these fields. So the market dynamic still remains incredibly tight. There’s also a physical pipeline infrastructure which will be put under greater stress.”

AGL does not want domestic reservation for two reasons. First, if it can control the gas price via imports then it will be much higher than otherwise. Second, that ensures much power prices for its legacy coal assets and developing renewables platform given gas sets the marginal cost of electricity.

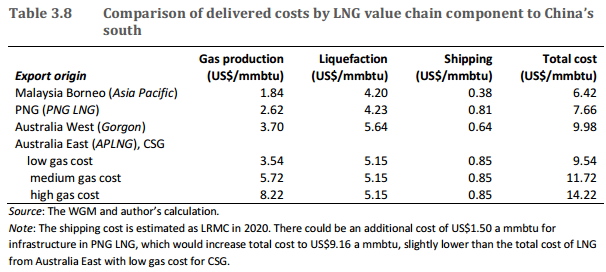

Its reasoning is rubbish. It is the case that as cheap Bass Straight is depleted the production cost will rise but nowhere near as high as it already is. $6Gj for domestic reservation is double historic averages and more than high enough to cover the cost of QLD gas extraction. Here is what that gas costs, via BREE:

These are all-in costs that include infrastructure. $6Gj offers reasonable margins for a lot of it. The gas cartel will fight you, of course, as its margin will be hit and it will have to write down the value of its white elephant plants even further but that’s just too bad. They need to leave the cheapest gas here and shave their export volumes 10-20%.

The next time somebody screams “sovereign risk” about prospective east coast gas reservation remind them of this:

- Edison renegotiated RasGas contract on price and volume in 2012;

- PGNiG renegotiated QatarGas contract on volume in 2014;

- Petronet renegotiated RasGas contract on volume and price in 2015;

- PetroChina renegotiated QatarGas contract on volumes in 2015;

- JERA renegotiated RasGas contract on volume and price in 2016;

- Pakistan renegotiated QatarGas contract on volume sand price in 2016;

- Japan declares multiple contracts illegal owing to “destination clauses” in 2016, following Europe from a few years earlier;

- Petronet renegotiated Exxon-Mobil Gorgon contract on volume and price in 2017;

- Woodside Pluto contracts renegotiated on price in 2017;

- Kogas renegotiated Woodside contract on price in 2018;

- GAIL renegotiated Gazprom contract on volume and price in 2018;

- India in talks with Cheniere and Dominion to renegotiate contracts in 2018.

These are just prominent examples. Notice that all of these renegotiations happened with foreign firms because they were overcharging for LNG once the global glut took hold.

Why is Australian “sovereign risk” so much more egregious than that of India, Pakistan, Poland, China, Korea or Japan? Why should the Aussie public be treated with less respect than that of India, Pakistan, Poland, China, Korea or Japan?

Gas reservation now.