China has released August economic numbers and the news is mixed. Industrial production is stable at 6.1%, retail sales likewise at 9% but fixed asset investment just keeps on falling at 5.3%:

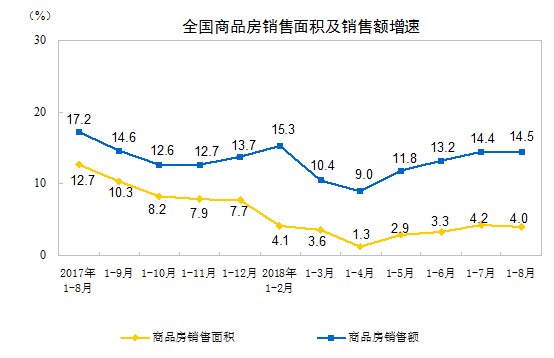

Turning to real state, sales by floor area are up 4% year to date:

That suggests there is slowing ahead but it’s not appearing in starts which are running wild, up 15.6% year to date. Indeed starts are now on target to exceed the 2012/13 superboom peak:

My guess is there is demand being brought forward ahead of winter shutdowns and we’ll see falling growth ahead:

Offsetting the boom now is the downdraft in infrastructure investment which has taken the brunt of deleveraging:

The split between houses and roads is showing up in the difference between outrageous steel output and falling cement production:

So, it looks likely still that Chinese growth will slow into year end as infrastructure and house building slow together into industrial winter shutdowns.

But, given we know that China is already priming to boost infrastructure spending, and that will counter-balance any forthcoming slowing in the apartment boom, the prospect next year is for China to kick the can again and build right into Trump’s trade war.

If the US joins them, next year will be quite spectacle for global growth.