Eurozone final August PMI was unchanged at 54.6, aided by a lift in Dutch activity (59.1 vs exp. 57.6), but the details show notable and disconcerting divergence. German and French PMI’s were revised -0.2 lower than their initial releases, but it was the write up on the profiles for new orders and lowering optimism that is a clear concern. Italy’s PMI was particularly weak (50.1, exp. 51.2) and Markit raised the potential for not only stagnation but even recession.

UK August PMI missed expectations (52.8, exp. 53.9). The contraction in new orders (for the first time since GBP’s sharp Brexit vote decline), falling domestic demand, sliding optimism and Brexit uncertainty are combining to raise fears of a “stalling manufacturing sector”.

Event Risk

Australia: Q2 current account deficit is expected to widen to $11.0bn (Westpac $11.5bn) from $10.5bn. Q2 net exportscontribution to GDP is anticipated to add 0.1ppts and Q2 public demand is forecast by Westpac to be up 1.0%. The RBA policy decision is universally expected to be on hold and no significant changes to their activity outlook are anticipated ahead of the Q2 National Accounts tomorrow. RBA Governor Lowe gives remarks later this evening at the RBA Board Dinner which typically involves a reflective and broad ranging speech.

UK: BOE Governor Carney testifies before Parliament’s Treasury Committee along with fellow colleagues Haldane, Tenreyro and Saunders.

US: Aug ISM manufacturing is seen to decline to 57.6 from 58.1 consistent with the fall in the flash estimate of the Aug Markit manufacturing PMI (final result also released today).

NZ: The GDT dairy auction tonight is priced by futures to result in a 1% fall in whole milk powder prices.

The Australian dollar was off the lows yesterday after GDP partials firmed up forecasts for a decent number, via Damien Boey at Credit Suisse:

Advertisement

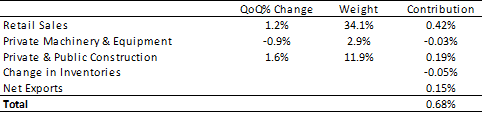

2Q real GDP looks quite solid

There were a few indicators released by the ABS a moment ago. Backward looking indicators were favourable, but forward looking indicators were not.

First, the good news. It appears that 2Q real GDP will print quite solidly, with the partials to date pointing to a growth contribution of at least 0.7%.

Inventory build was surprisingly robust in 2Q, with the stock rising by 0.6% in real terms, following an 0.7% gain in 1Q. The second derivative of inventories (the stock), which matters for GDP (the flow), was only slightly negative. Consensus was looking for a much bigger drag.

Prior to the business indicators release, we already knew that retail spending growth was strong over the quarter, while capex indicators were quite mixed, and net exports (in volume terms) contributed moderately to growth. We are still yet to receive government spending data, which makes up a significant chunk of the 50% of GDP missing from available partials. But early indications are still positive for 2Q.

More partials today. After GDP tomorrow we can expect forex markets to look forward again and not like what they see. Given my year-end forecast for AUD of 0.72 cents is now blown, let’s aim for 0.7 cents by New Year.

0.65 cents next year.

Advertisement

David Llewellyn-Smith is chief strategist at the MB Fund which is long US equities that will benefit from a falling Australian dollar so he is definitely talking his book. Below is the performance of the MB Fund since inception:

If the ideas above interest you then contact us below.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.