DXY was firm overnight. CNY and EUR were weak:

AUD was hit:

Gold is still stuck:

Oil broke to a four year high:

Base metals reversed:

So did miners:

And EM stocks:

But EM junk signaled more bid ahead:

Treasuries were hosed:

And bunds:

While stocks eased a touch:

Westpac has the wrap:

Market Wrap

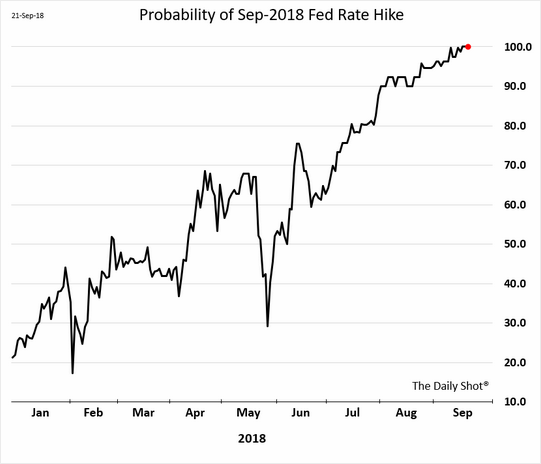

Global market sentiment: US equities were in a cautious mood following China’s abandonment of trade talks with the US, the S&P500 down 0.3%. Brent crude oil is up 3.3% after OPEC indicated less urgency to boost output. US bond yields were stable while currencies were mixed.Interest rates: The US 10yr treasury yield continued to range sideways a four-month high, between 3.06% and 3.09%. 2yr yields also ranged sideways but did nudge 2.83% – a fresh high since 2008. Fed fund futures yields continued to price 100% chance of a hike on 26 Sep, while the chance of another hike in Dec is priced at 90%.

FX: The US dollar index is unchanged on the day. EUR initially jumped from 1.1750 to 1.1815 – a three-month high – after Draghi’s speech (see below) but completely retraced a few hours later. USD/JPY rose from 112.50 to 112.76. AUD slipped from 0.7280 to 0.7255. Underperformer NZD fell from 0.6675 to 0.6642. AUD/NZD rose from 1.0890 to 1.0925.

Economic Wrap

In the US, Chicago Fed survey was unchanged at a solid 18 (exp. 20, prior revised from 13) while Dallas Fed’s survey slipped to 28.1 (exp. 31.0, prev. 30.9) with some noted pullbacks in new orders and employment.Germany’s September IFO survey was stronger than expected, holding close to August’s (revised up +0.1%) levels. Among the main components: business climate 103.7 (vs exp. 103.2, previous 103.9), expectations 106.4 (vs exp. 106.0, prior 106.5).

ECB President Draghi gave his regular economic update to the EU Parliament and began with phrases lifted from the ECB policy statement, maintaining its neutral bias. However, he added that the stable profile of headline inflation forecasts conceals “a relatively vigorous pick-up in underlying inflation” and underscored an improving labour market and signs of shortages, supporting the ECB’s expectations of higher wages.

Event Risk

Japan: BoJ Governor Kuroda speaks at a press conference in Osaka.Euro Area: ECB Chief Economist Praet speaks in London at various events. ECB member Coeure chairs a sessions at the annual ECB research conference.

US: Jul S&P/Case-Shiller home prices are seen to be down in the month but remain in an uptrend. Sep Conference Board consumer confidence is anticipated to remain elevated with a strong labour market providing a foundation for upbeat sentiment.

The probability of a Fed hike this week is now 100%:

We may well see another in December, especially if oil keeps running which is US bullish. There are reasons to think it might for a short while at least. There is room for speculators to run:

The driver is Iranian curtailments much larger than I expected, via Bloomie:

“The market does not have the supply response for a potential disappearance of 2 million barrels a day in the fourth quarter,” Mercuria Energy Group Ltd. co-founder Daniel Jaeggi said in a speech at the S&P Global Platts Asia Pacific Petroleum Conference, knows as APPEC. “In my view, that makes it conceivable to see a price spike north of $100 a barrel.”

When Trump in May announced plans to reimpose sanctions on Iran’s oil exports, the market estimated a cut of about 300,000 to 700,000 barrels a day, said Trafigura Group co-head of oil trading Ben Luckock. However, the consensus has now moved to as much as 1.5 million barrels daily as the U.S. is “incredibly serious” about its measures, he said.

Iran’s production “is going to be significantly less than it was, and probably lower than most people expected when the sanctions were announced,” Luckock said at the APPEC event. He sees $90 oil by Christmas and $100 in early 2019.

That has buggered my oil balance chart:

The obvious offset in Saudi Arabia is dragging its feet, via Reuters:

The Organization of the Petroleum Exporting Countries and non-OPEC states, including top producer Russia, gathered in Algiers on Sunday for a meeting that ended with no formal recommendation for any additional supply boost to counter falling supply from Iran.

“The market’s still being driven by concerns about Iranian and Venezuelan supply,” said Gene McGillian, director of market research at Tradition Energy in Stamford. “The failure of the producers to address that adequately this weekend is creating a buying opportunity.”

More US supply is coming but it will take time:

Plains All American is building oil pipelines in the Permian as fast as it can. The company currently has two large projects underway, Sunrise, which it initially expected to finish in January of 2019, and Cactus II, which it hoped would start partial service by the end of 2019.

However, given the crucial need for more pipeline space, Plains is “trying to accelerate both of these projects as much as reasonably practical,” according to Chief Operating Officer Willie Chiang. To do so, Plains is “incurring additional costs to expedite material deliveries and vendor services and even installing temporary generators for our pumps until permanent utility power is available.” Those efforts are paying off, as the company now expects to begin commercial operations on Sunrise on the first of November.

The pipeline will move oil from the Permian up to a hub in Texas, where it can catch a ride on other systems to America’s main oil storage hub in Cushing, Oklahoma. Sunrise should be able to transport 360,000 BPD by the first quarter of next year, with full capacity slated to be as much as 500,000 BPD. That near-term in-service date has helped ease the pressure on oil prices in the Permian, causing the discount with WTI to narrow to $11 per barrel.

In addition to the capacity from that pipeline, railroads are looking for ways to help ease the bottleneck in the near term by shipping some crude by rail. “The [Permian] is an interesting place, and we’re definitely seeing some reduction in crude production due to the lack of pipelines,” said Beth Whited, the chief marketing officer of Union Pacific (NYSE:UNP) on the company’s second-quarter call. Union Pacific has “some capacity in our network and expects to see some results in the third and fourth quarter.” Since that time, Union Pacific struck a deal with a logistics company to ship about 400,000 barrels per month of crude on its system through next year, with the potential for it to last into 2020.

However, the big capacity boost will come toward the end of next year, when as many as three large-scale pipelines could enter service. Plains All American Pipeline’s Cactus II should begin partial service by the third quarter of next year before starting full service of 670,000 BPD by April of 2020. Meanwhile, Phillips 66 Partners (NYSE:PSXP) and Andeavor (NYSE:ANDV) are building the Grey Oak Pipeline, which could move as much as 800,000 BPD to the Gulf Coast. Phillips 66 Partners and Andeavor plan to spend $2 billion to build the pipeline, which should start up by the end of 2019. That line would not only bring oil to refineries in the region but also to a new export dock under construction by Phillips 66 Partners, Andeavor, and another partner. Finally, the private equity–backed EPIC crude pipeline is also expected to start construction by the end of this year, which would put it in service by the second half of 2019.

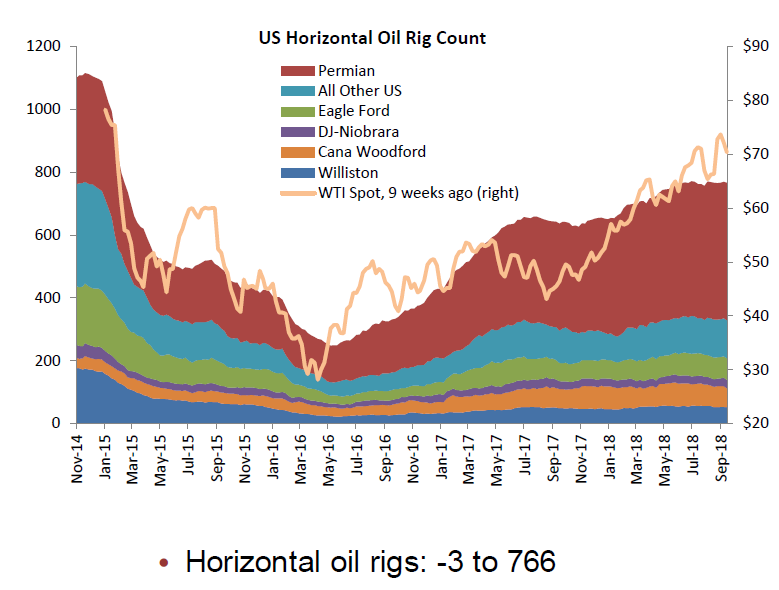

Pipeline constraints help explain the stall in the US rig count:

Rising oil has traditionally been good for the AUD and bad for DXY. But that relationship reversed in 2018:

I put this down to the steady realisation that US growth is these days a net beneficiary from higher oil through its exploding oil and gas export sectors and the understanding that Australian mismanagement of its gas resources means higher oil is a net negative for growth.

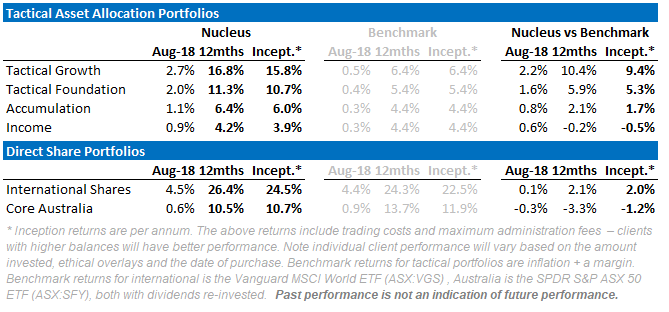

David Llewellyn-Smith is chief strategist at the MB Fund which is long US equities that will benefit from a falling Australian dollar so he is definitely talking his book. Below is the performance of the MB Fund since inception:

If the ideas above interest you then contact us below.