The Australian dollar continues to fall on the crosses. It held against DXY:

But fell against EMs:

Advertisement

Gold is stuck:

Oil too:

Base metals fell:

Advertisement

Big miners are breaking down:

EM stocks hit new lows:

Junk was a bit better:

Advertisement

Treasuries sold:

And bunds:

Stocks firmed:

Advertisement

Westpac has the data wrap:

Economic Wrap

EU chief negotiator Barnier said a Brexitdeal within eight weeks is realistic and possible, speaking at a conference in Slovenia. There is growing expectation in the media of a Brexit summit in November with a more lenient EU mandate for Barnier to reach an agreement (after that, it would still need to pass the UK Parliament).

UK data was mixed but positive overall. July GDP rose +0.3%m/m (beating expectations of +0.1%), but the impact was muted given that this is only the third release of this new monthly series. UK July trade deficit contracted more than expected to almost zero at -GBP0.11m (exp. –GBP2.1bn) and June’s deficit was revised lower by almost GBP1bn (to –GBP0.94bn). July industrial production slipped below expectations to +0.9%y/y (exp. +1.1%y/y. Recently troubled construction surprised with a lift (+0.5%m/m, exp. -0.5%m/m) but manufacturing was markedly lower (-0.2%m/m, exp +0.2%m/m).

Event Risk

NZ: electronic retail spending in August is estimated to have risen 0.5%. Consumer spending has held up well in the face of a slowing housing market, probably supported by the new government’s family support measures.

Australia: Aug NAB business survey conditions were last at 12, which is still elevated despite the recent moderation. The confidence index has held just above average and will be closely watched this month after the recent Prime Minister change. Q3 AusChamber-Westpac manufacturing survey is released.

Euro Area: Sep ZEW survey of expectations has stabilised in Aug at -11.1 after the index deteriorated to a greater extent than other European sentiment gauges.

UK: Jul ILO unemployment rate is expected to hold at 4.0%.

US: Aug NFIB small business optimism is anticipated to remain at an elevated level.

Argentina: The Central Bank of Argentina meeting will get more attention than usual amidst the emerging market rout. The BCRA raised the benchmark rate to 60% in late August.

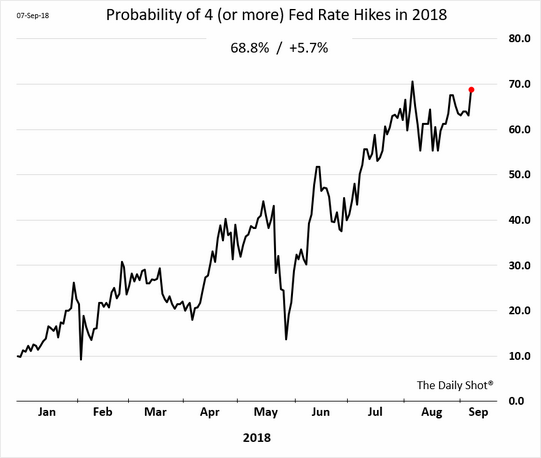

Rate markets have moved to price more Fed tightening after Friday’s excellent jobs report:

Advertisement

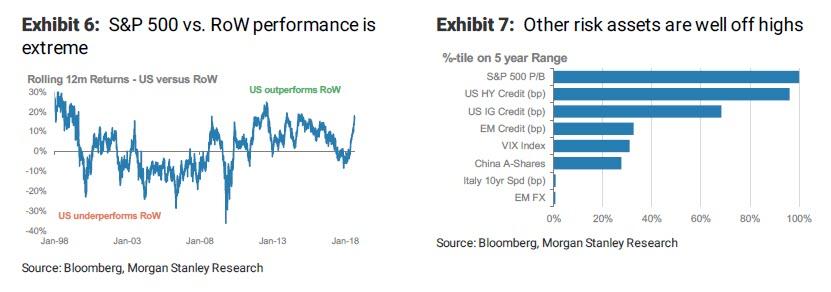

What’s next? Morgan Stanley says weakness by year end and has removed:

a positive bias to US equities that has existed since April 2017…while our cycle models remain in ‘expansion’, a phase that has historically seen valuation overshoots, we are increasingly concerned that the bulk of this tailwind is already behind us.

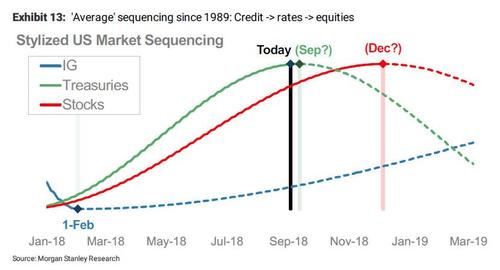

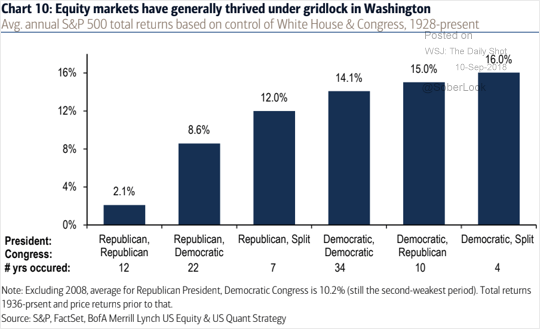

That accords with the MB Fund base case. We are using something of “barbell” strategy to address it with overweight allocations to both tech for growth and consumer staples for defense. The standout risk in coming months is the US mid-terms which will likely see the Dems win the House and increase pressure on the White House. That said, political deadlock is usually good for US stocks:

Advertisement

I still see the odds for 2019 as evenly split. The US consumer is on a charge with rising wages a tailwind. Yet they are not so tearaway as to threaten corporate profits. We know the fiscal cliff is coming but we could (should) see more US fiscal stimulus as well and more Chinese stimulus kicking the can forward again. Neither is going to want to appear to be losing the trade war.

The question is one of timing. How much weakness creeps into both economies and markets first? Yet this is offset by a Fed clearly willing to pause mid-next year.

Advertisement

We continue to hold a conservative equity allocation around 60% heavily over-weighted international for AUD protection with the balance in cash in fixed interest for a hedge and war chest.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.