Westpac: Falling deposits to keep bank funding costs elevated

By Elliot Clarke, Senior Economist at Westpac

Overview:

The significant increase in short-term wholesale interest rates and associated volatility has been a key topic of debate in markets throughout 2018.

Initially linked to higher borrowing costs in the US, a further spike in only Australian rates as the June quarter drew to a close saw participants’ focus shift to domestic drivers of this pricing activity.

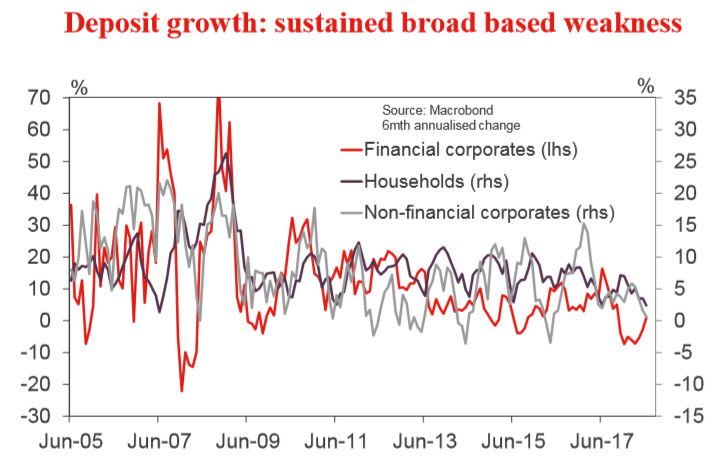

There are many market factors that have played a part in the surge in short-term interest rates. All are worthy of discussion, but in this instance we focus on the real economy’s effect. Specifically, the broad-based deceleration in deposit growth.

While we believe that there is insufficient evidence to label the decline in deposit growth as the prime catalyst for higher short-term interest rates, deposit growth’s persistent underperformance is critical to our view that the abnormally large market spreads present will, by and large, be sustained.

Put simply, if (in dollar terms) retail deposits increase at a lesser rate than credit, then Australian lenders’ reliance on wholesale funding must increase. This looks likely over the remainder of 2018 and 2019 if, as we anticipate, national and household income growth remain soft, led by weak wages growth; a downturn in employment growth; and the terms of trade. Consumer saving and investing decisions are unlikely to provide a meaningful boost to deposit growth absent a shock because consumers already favour deposits (and super) over other asset types.

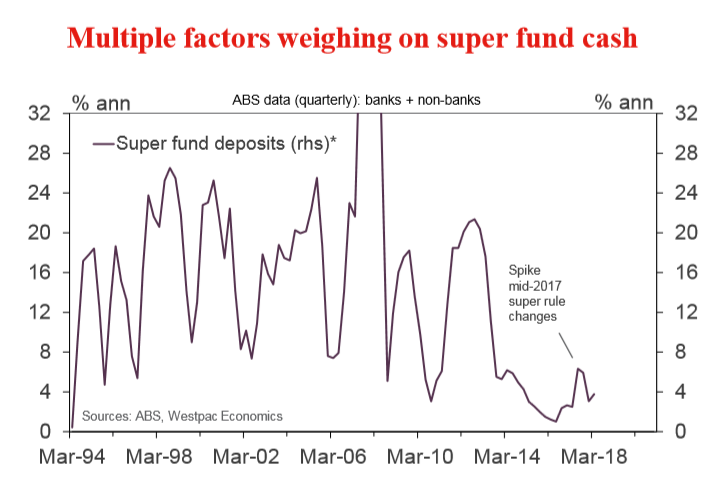

For superannuation deposits, weak income growth is not the only headwind. Over the past year, households’ capacity to make voluntary contributions to super has been further reduced, limiting the flow of new fund inflows. A falling allocation to domestic cash (in favour of offshore investment opportunities) amongst the industry has further restricted the flow of new deposits to Australian banks and other depository institutions. With the Australian economy expected to register growth at or below trend in 2018/ 2019 as global growth remains near its post-GFC peak, Australian investors’ appetite for offshore assets is likely to persist.

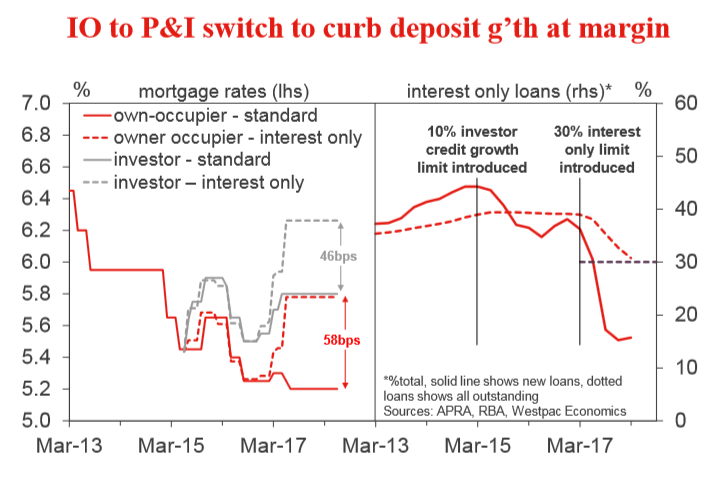

The final point of note is the significant tightening of lending standards underway. This policy shift, yet again, is a negative for households’ ability to accrue deposits. Specifically, those switching from interest only to principal & interest face a much higher total monthly payment. Meanwhile, those who remain on interest–only terms will pay a higher interest rate now, and the majority will still inevitably have to move to principal & interest later to pay down the loan. The longer that interest only terms are relied upon, the more rapid the required paydown becomes over the remainder of the 30-year term, unless a borrower is successful in refinancing the loan with another counterparty.

Drivers of elevated short-term interest rates are plentiful:

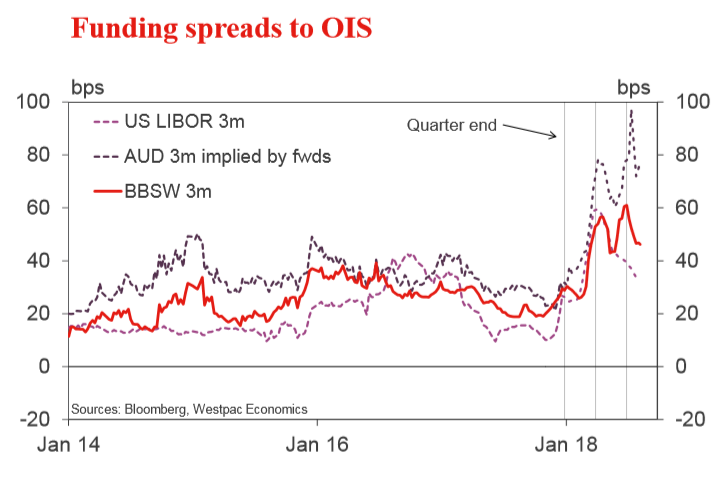

Australian short-term wholesale interest rates have been a point of debate throughout 2018. Into March quarter end, the move higher in the Australian 90 day BBSW spread to OIS mirrored the move in the US’ LIBOR spread to OIS. However, going into June quarter end, Australian funding spreads exhibited another spike higher as LIBOR eased back. Attention then turned to potential domestic factors.

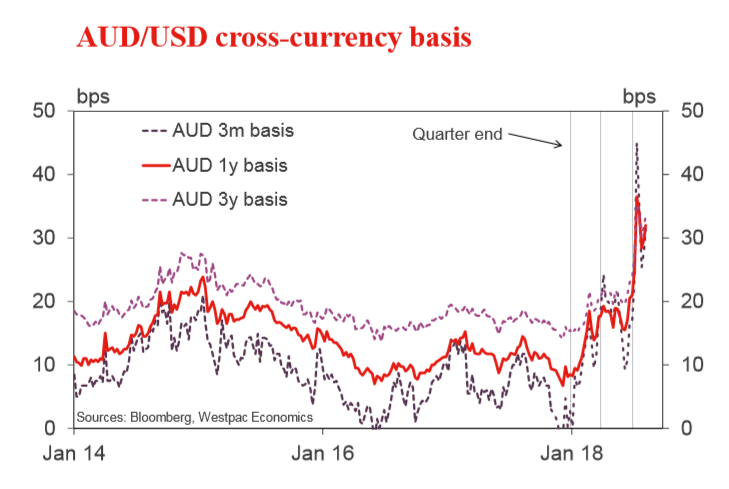

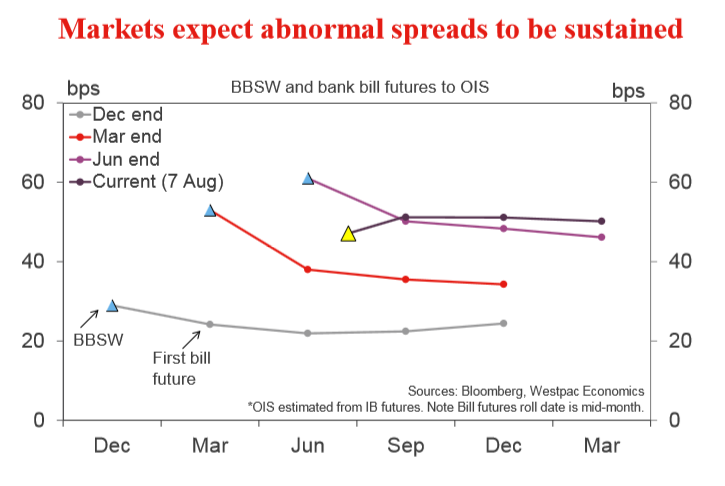

The lift in Australian short-term rates is not limited to BBSW. Secured funding in the repo market as well as the premium to borrow AUD in the FX swap market (cross currency basis) have also risen and exhibited greater than usual volatility. Pressures have been most acute around quarter end, but spreads have also remained more elevated than usual through the middle of the quarter. The key question that follows is whether these pressures will be sustained. Increasingly the market believes that they will, with the forward curve spread between domestic bill futures and OIS flattening out around 50bps versus the 35bp spread priced during the first bout of funding pressures in March.

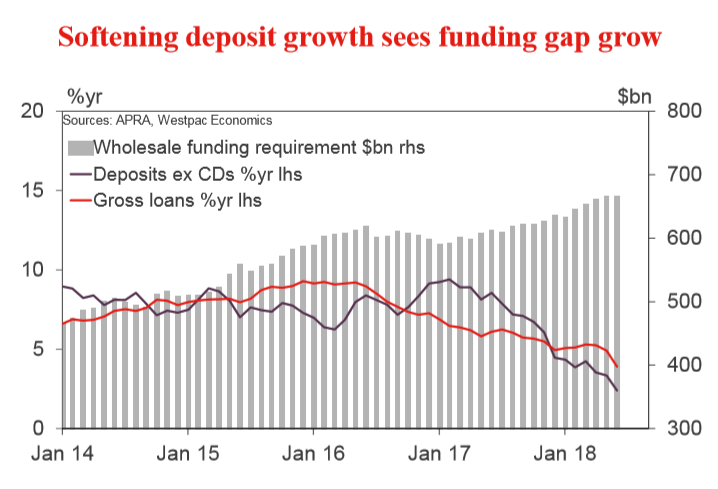

A number of potential drivers have been identified by market analysts as relevant, and we agree with many. But from the real economy, decelerating deposit growth and a consequent widening of the deposit gap is critical.

Weak deposit growth is a structural factor…

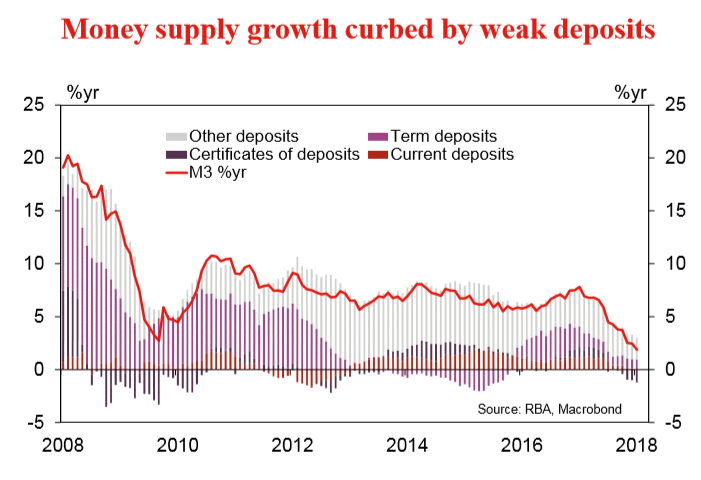

As the market has sought to understand the jump in short-term Australian interest rates, the sharp deceleration in money supply growth (M3) has come into focus. Notably this decline has come as a result of softer growth for all deposit products sustained through the year.

We believe there is insufficient evidence to label the decline in deposit growth as the prime catalyst for higher interest rates – particularly as net issuance of certificates of deposits (wholesale deposits) has been little changed over the period. That said, the underperformance of deposit growth is central to our expectation that these abnormal circumstances will endure.

Put simply, if (in dollar terms) retail deposits increase at a lesser rate than credit, then Australian lenders’ reliance on wholesale funding must increase. Some of this funding will come from offshore, but as the hedging cost of swapping foreign currency into Australian dollars has also risen sharply (shown in chart 2 on the previous page), new issuance will likely be balanced across offshore and domestic markets. Higher demand for funds at a time of restricted supply will sustain upward pressure on the cost of funds from both jurisdictions.

Why do we anticipate deposit growth will remain subdued?

… that will only reverse as income growth lifts

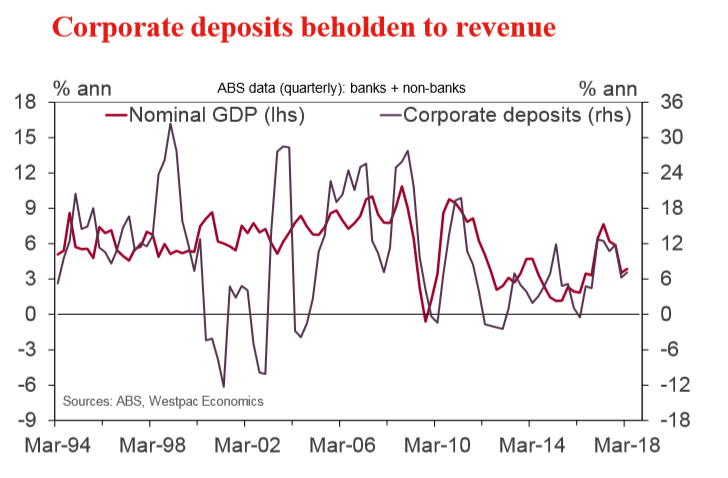

A marked slowdown in nominal income growth has been crucial to the broadbased deceleration in deposit momentum. With the exception of a spike to 8% in March 2017, nominal GDP growth has experienced a protracted period of subdued growth since mid-2012, restricting the flow of new corporate deposits. Here, Australia’s terms of trade have been key, particularly over the past year, as growth fell from +25%yr at March 2017 to –3%yr at March 2018.

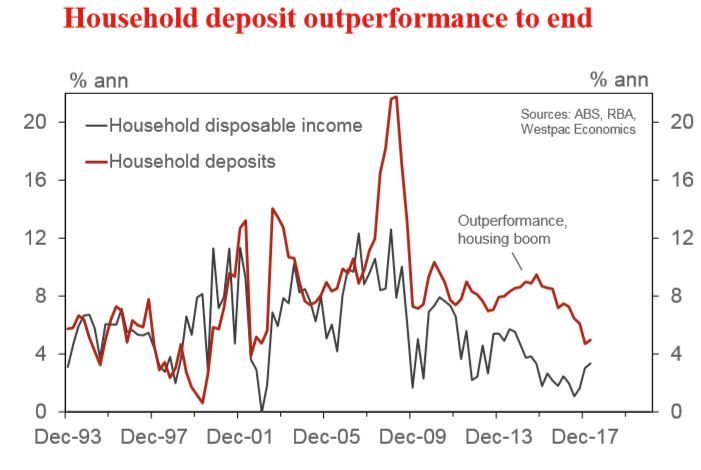

Wages have consequently also come under sustained pressure as firms maximised the pass-through of revenue to profit. Interestingly however, for households, income’s effect on deposit growth was not seen until late-2015. This is because prior to that, strong growth in house prices and subsequent high turnover (property sales) boosted deposit growth. Looking ahead, with momentum in the housing market to remain muted, income is expected to be the dominant factor behind household deposits. For household income, stronger growth will be challenging owing to the lasting headwinds of labour market slack; technology and globalisation.

Growth in super fund deposits face additional challenges because of households’ reduced capacity to make voluntary contributions and super funds’ allocation out of domestic cash in favour of offshore investments. Each of these factors are also likely to have a lasting effect.

The risks for deposit growth are negatively skewed

In addition to the rate of growth of income, household saving, investing and financing decisions are also important for deposit growth.

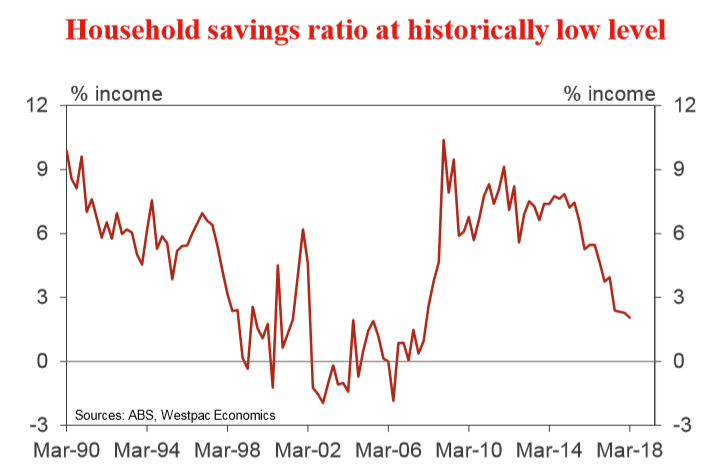

Evident from the national accounts, households’ capacity to save is dwindling. This is a consequence of weak income growth rather than strengthening spending as consumption growth has maintained a sub-par pace for a number of years. While a sentiment shock could see households reduce consumption and save more, in ordinary conditions this is unlikely.

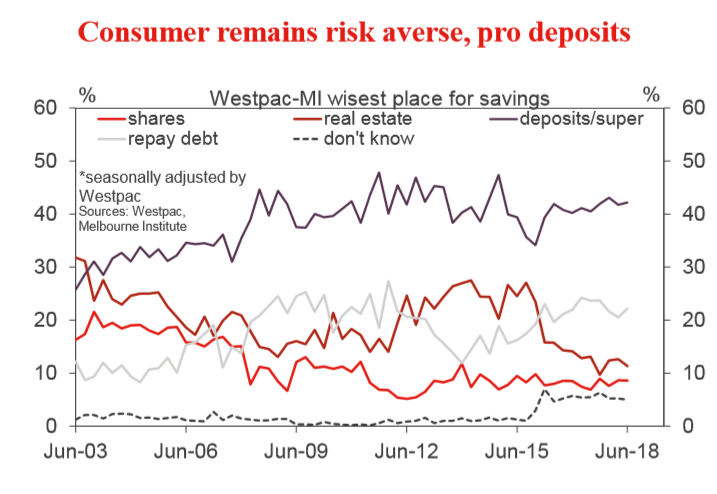

Moreover, from our Westpac–MI consumer sentiment survey, it is evident that deposits and super remain the focus for household savings. Hence, we are unlikely to see a sustained reallocation from risk assets to deposits. Within super, as above, the more likely outcome is that growth opportunities offshore are taken up, to the detriment of the asset allocation to domestic assets.

Regarding financing, the switch from interest only to principal & interest repayments will, at the margin, detract from households’ deposit accrual. Though principal & interest loans come with a lower interest rate, the total repayment is much greater than the interest cost alone. While this switch sees debt repaid more quickly, all else equal, it also slows deposit growth.