Via Bill Evans at Westpac:

The Reserve Bank’s August Statement on Monetary Policy provides few surprises.

Of most interest in the Statement is the update in the Bank’s forecasts. In particular, this update includes another six months of forecasts to cover the whole of 2020.

The GDP growth rate forecasts through to end 2018 and end 2019 are unchanged from the May Statement at 3 ¼ per cent, while the 3 per cent forecast for growth through to June 2020 is extended to December 2020. The forecast slowdown between 2019 and 2020 is attributed to a flat contribution from LNG exports as production capacity peaks in 2019.

Growth to June 2018 is forecast at 3 per cent compared to 2 ¾ per cent in May. This forecast implies that the Bank is expecting the GDP print for the June quarter to be an optimistic 1.0%, following the 1.0% which was registered for the March quarter. In contrast, Westpac is expecting 0.6% for the June quarter growth rate.

The significant change from May comes with the inflation forecasts. Headline inflation to December 2018 has been revised down from 2 ¼ per cent to 1 ¾ per cent. Underlying inflation to December 2018 has been revised down from 2 per cent to 1 ¾ per cent. If those forecasts prove correct, then 2018 will be the fifth consecutive calendar year in which headline inflation has printed below the bottom of the 2-3% target band and the third consecutive year when underlying inflation has been the below the bottom of the band.

The Bank attributes this revision to changes in the September quarter, specifically for electricity, childcare costs and some education costs. They are claimed to be one-off and do not affect any subsequent quarters. Consequently, the forecasts for the year ending December 2019 are unchanged at 2 ¼ per cent (headline) and 2 per cent (underlying). The modest forecast lift in underlying inflation to 2 ¼ per cent to June 2020 which we saw in the May statement is extended to December 2020, with both headline and underlying forecast at 2 ¼ per cent.

There are no changes to the unemployment profile with the rate expected to be 5 ½ per cent in December 2018, 5 ¼ per cent in December 2019 and a projected fall from 5 ¼ per cent in June 2020 to 5 per cent in December 2020.

Commentary in the Statement around the growth and inflation outlook is largely unchanged from May. Consumer spending continues to be a source of “significant uncertainty” largely because of the outlook for household income growth. Key components here are wages growth and employment growth. The Bank does not provide specific forecasts for these variables, although employment growth is expected to be slightly above working age population growth of 1.6%.

Last week, I pointed out the deterioration in employment growth around the last two Federal election periods (2013 and 2016). With another election due by May next year, the risk of an unexpected slowdown in employment growth must be quite real although the Bank does not consider that prospect as part of the risks outlined in the Statement.

We are also not given the Bank’s forecasts for wages growth. The persistence of the unemployment rate being forecast to be above the full employment rate of 5 per cent would indicate little expected wage pressures. The Bank does identify uncertainty around the level of spare capacity in the labour market and seems to rely on its liaison program and evidence of tight conditions in construction and information technology. It is interesting to observe that the Government’s forecasts which were included in the May Federal Budget, and entailed a similar profile for the unemployment rate, expect wages growth of 3 ¼ per cent in 2019/20 and 3 ½ per cent in 2020/21. Prospects for such an optimistic outcome for wages growth seem remote, particularly as the Bank observes that current new enterprise bargaining agreements are lower than the average of those currently in existence.

The reason why the outlook for household incomes is so important is that with a very low savings rate; high debt levels; and falling house prices; it seems unlikely that household consumption can grow at a faster pace than incomes in the way we have seen in recent years.

These risks around a negative wealth effect are down played in the commentary. Various spokesmen for the Bank have indicated that while empirical estimates of the wealth effect are quite dated, the view is that the negative wealth effect in this upcoming cycle will be modest.

The Statement notes that “there is no evidence that moderate house price declines have weighed on household consumption to date”. However, appropriately, some concern is raised around the consumption of highly indebted and or credit constrained households. The Statement rightly acknowledges the recent solid growth in non-mining business investment which reached 10% over the year to the March quarter, largely driven by non-residential construction. While approvals in this sector are falling, the Bank’s expectation is that growth in machinery and equipment investment will pick up further over the forecast period. These investment decisions will be significantly influenced by expected demand and therefore the household consumption profile, making the debate around incomes important not only for consumption itself but also business investment. Those risks around political uncertainty are also relevant for business confidence and investment.

Public demand and exports remain the bright side of the growth outlook. We acknowledge that this boost is likely to continue and has spill-over effects to private sector investment. It is also true that resources export growth will be sustained although iron ore and coal volume growth will be relatively flat and compensated for by the ongoing boost in LNG at least out to end 2019.

Conclusion

The Bank’s approach, consistent with the May Statement, and many preceding statements, is to anticipate a gradual return to “normal conditions”. The spectre of the persistent underperformance of inflation over multiple years must be unnerving. Nevertheless this gradual return to normality remains the theme. From our perspective weak wages growth; a slowdown in employment growth; and potential negative wealth effects loom as more significant risks to these forecasts than the Bank appears to be prepared to accept at least in the Statement.

Westpac expects growth in the key policy year of 2019 to be only 2.5% compared to the 3 ¼ per cent anticipated by the RBA. We see larger risks around the household sector; negative wealth effects from the housing market; and share the RBA’s unease around the outlook for risks in China.

There is a clear sense that there is no particular urgency to change the policy stance and a forecast of 2 ¼ per cent underlying inflation and 5 per cent unemployment in 2020 certainly confirms that view.

We see no reason based on the Statement and the forecasts to change our view that the cash rate will remain on hold through the remainder of 2018 and 2019.

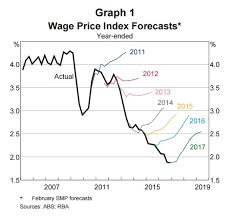

And a quick reminder of how reliable the RBA isn’t:

Next move in interest rates remains own.