Reverse mortgages have yet to take-off in a big way across Australia. This is partly due to the generosity of our aged pension system, which largely excludes the owner-occupied home from the assets test, as well as the relatively high threshold placed on financial assets.

Nevertheless, the Australian Securities and Investment’s Commission (ASIC) has today published a review of reverse mortgage lending, which highlights the risks to borrowers that exhaust their home equity long before they die. Here’s Martin North’s summary:

ASIC’s review of the reverse mortgage industry highlights that some taking a reverse mortgage could face financial difficulty later in life. This despite the fact that borrowers can never owe the bank more than the value of their property, and can remain in their home until they pass away or decide to move out.

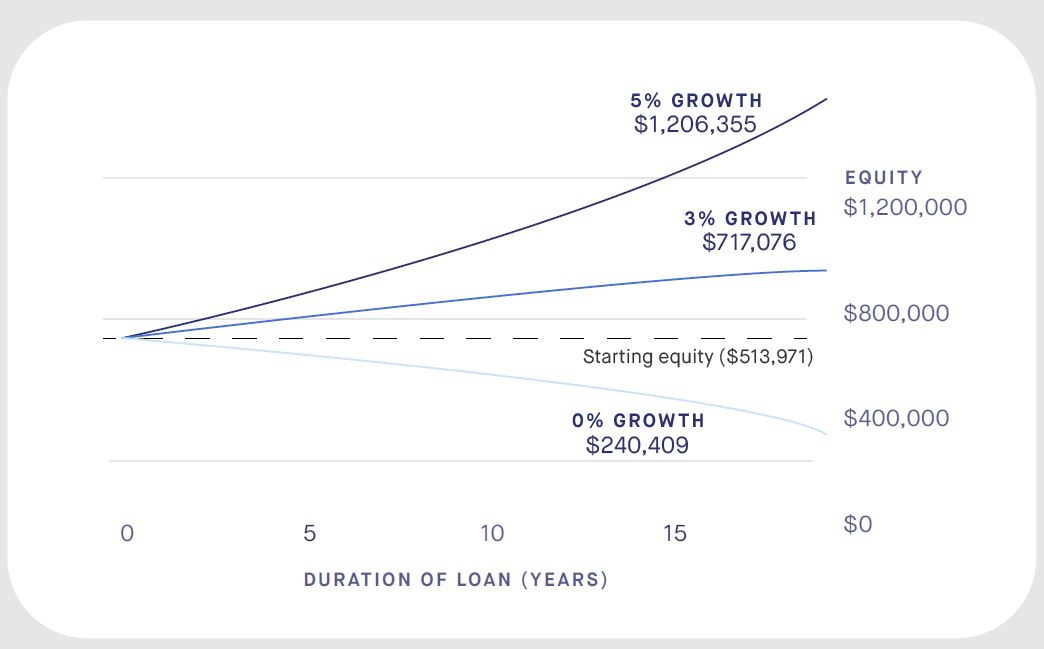

Thus, while this type of finance may assist older home owners (70% aged 55-85 own their own home), they face the dual risks of compounding effects on the original loan value as interest is rolled up…

… and significant risks should home prices fall, leading to loss of all or most capital. 63% of borrowers may end up with less equity than the average upfront cost of aged care for one person by the time they reach 84.

Plus there is limited competition, as just 2 credit licensees wrote 80% of the dollar value of new loans from 2013 to 2017.

And here’s the key extracts from the ASIC paper:

A review by ASIC has found that reverse mortgages are allowing older Australians to achieve their immediate financial goals – improving their lifestyles in retirement – but longer-term challenges exist.

For older Australians who own their home with few other assets, a reverse mortgage can allow them to draw on the wealth locked up in their homes, while they continue to live in their property.

ASIC reviewed data on 17,000 reverse mortgages, 111 consumer loan files, lender policies, procedures, and complaints. We also commissioned in-depth interviews with 30 borrowers and consulted over 30 industry and consumer stakeholders.

The review found borrowers had a poor understanding of the risks and future costs of their loan, and generally failed to consider how their loan could impact their ability to afford their possible future needs. Lenders have a clear role to play here and need to do more: for nearly all of the loan files we reviewed, the borrower’s long term needs or financial objectives were not adequately documented.

Importantly, under legal protections in place since 2012, borrowers can never owe the bank more than the value of their property, and can remain in their home until they pass away or decide to move out. However, depending on when a borrower obtains their loan, how much they borrow, and economic conditions (property prices and interest rates), they may not have enough equity remaining in the home for longer term needs (e.g. aged care).

ASIC Deputy Chair Peter Kell said “Reverse mortgage products can help many Australians achieve a better quality of life in retirement.”

“But our review shows that lenders and brokers need to make inquiries that would lead to a genuine conversation with customers about their possible future needs, not just a set of tick boxes on a form.”

ASIC’s report also finds that there is an opportunity for lenders to reduce the risk of elder abuse. Under the new Code of Banking Practice, recently approved by ASIC, banks will be required to take extra care with customers who may be vulnerable, including those who are experiencing elder abuse.

Consumers also had limited choices for finding a reverse mortgage. Several providers withdrew from the market after the global financial crisis. From 2013 to 2017, two credit licensees provided 80% of the dollar value of new loans from 2013 to 2017.

Background

Reverse mortgages are a credit product that allows older Australians to borrow using the equity in their home. The loan does not need to be repaid until a later time, typically when the borrower has vacated the property or passed away. They are a more expensive form of credit compared to standard variable owner occupier home loans; the interest rates are typically 2% higher and, as there are no repayments required, interest compounds.

Consumer demand for reverse mortgages has grown gradually since the global financial crisis, with the total exposure of ADIs to reverse mortgages increasing from $1.3 billion in March 2008 to $2.5 billion by December 2017.

ASIC commenced a review of lending practices and consumer outcomes in the reverse mortgage market to proactively examine issues that might emerge for older Australians.

As part of this review, we evaluated the effectiveness of enhanced responsible lending obligations for reverse mortgages which were introduced five years ago into the National Consumer Credit Protection Act 2009 (National Credit Act).

This review examined five brands, who collectively lent 99% of the dollar value of approved reverse mortgage loans in 2013-17. These brands were: Bankwest, Commonwealth Bank, Heartland Seniors Finance, Macquarie Bank and Westpac (comprising St George Bank, the Bank of Melbourne and BankSA). As of late 2017, Macquarie Bank and Westpac are no longer providing new reverse mortgages.

The May Federal Budget expanded the Pension Loan Scheme (PLS) to allow all retirees to obtain a state run reverse mortgage.

Thus, there should be less incentive for Australians to seek a reverse mortgage with a commercial lender going forward.

unconventionaleconomist@hotmail.com