Below is RBA Governor Phil Lowe’s opening statement to the House of Representatives Standing Committee on Economics:

Thank you for the opportunity to appear before the Committee today. These hearings are an important part of the accountability process for the Reserve Bank of Australia. As usual, my colleagues and I will do our best to answer your questions.

Since we last met, the Australian economy has continued to move in the right direction. According to the most recent data, GDP growth is 3.1 per cent, inflation is around 2 per cent and the unemployment rate is now below 5½ per cent. In the broad sweep of our economic history, these are a pretty good set of numbers. We would, of course, like them to be better – we are still short of full employment and we would like to be more confident that inflation will be sustained at a level consistent with the target. But if things work out as expected, we are likely to make further gradual progress on both fronts over the next couple of years.

The Australian economy looks to have grown strongly over the first half of 2018. GDP increased by 1 per cent in the March quarter and a reasonable increase is expected in the June quarter. Business conditions are positive and we are in the midst of an upswing in non-mining business investment. Increased spending on infrastructure is also helping. Resource exports are also increasing strongly as new capacity comes on stream, particularly for LNG. One important offsetting factor is the drought in eastern Australia. While the prices of some farm products are currently quite high, the dry conditions will limit farm production.

I thought it might be useful to make some introductory remarks on four topics the Reserve Bank Board has devoted considerable attention to over recent times: the global outlook; household debt and the housing market; wages growth; and the outlook for inflation.

The global outlook remains positive, although a number of risks have increased. The advanced economies are growing faster than trend and unemployment rates are at multi-decade lows in some countries. A gradual pick-up in wages growth is also now taking place. As is appropriate, the considerable monetary stimulus that has been in place in the United States is being steadily withdrawn. At the same, though, official interest rates in the euro area, Japan, Sweden and Switzerland are still negative, more than a decade after the onset of the financial crisis. In China, growth has slowed a little. The authorities have responded to this, although they also face the challenge of addressing risks in the financial system.

There are a few uncertainties that are worth highlighting.

One is the possibility of an escalation in global trade tensions. The measures announced so far are unlikely to derail the global expansion. Even so, in some countries, businesses are delaying investment because of the additional uncertainty. It is possible that this becomes a more general story. If this were to occur, this could be the channel through which the trade tensions sap the current positive momentum in the global economy.

Another uncertainty is the possibility of a larger-than-expected pick-up in inflation in the United States. The US economy is experiencing a sizeable fiscal stimulus at a time of limited spare capacity, so growth there could surprise on the upside. At the same time, financial markets remain relaxed about the implications of this for inflation. I am less relaxed: it is highly unusual to have such stimulatory fiscal policy when the economy is already operating at a very high level of capacity. One can’t rule out the possibility that the Federal Reserve will have to withdraw monetary accommodation more quickly than currently projected, with possibly disruptive consequences in financial markets.

A third set of global risks originate from a number of individual economies with country-specific structural and/or institutional vulnerabilities, including Argentina, Brazil, Italy and Turkey. Over the past month there have been episodes of market volatility associated with each of these countries. We are watching developments closely as a further escalation of problems could be a catalyst for a period of increased stress in the global financial markets.

The second issue is the housing market and household debt.

The housing markets in Sydney and Melbourne have clearly slowed and prices are coming down. While this has concerned some people, we need to keep things in perspective. Not so long ago, there was concern in the community about rapidly rising housing prices and debt and declining housing affordability. These earlier trends were not sustainable and were posing a medium-term risk to our economy. So a pull-back is a welcome development and can put the market on a more sustainable footing. It is good news that this adjustment is taking place at a time when global growth is strong, the labour market is positive and interest rates are low. All these things are helping with the adjustment. We are nevertheless continuing to keep a close eye on housing market developments across the country.

The slowing in the housing market has reduced the demand for credit by investors. There has also been some tightening in the supply of credit, partly in response to the Royal Commission, although the main story is one of reduced demand. The average variable interest rate paid by borrowers has declined further over the past six months, to be about 10 basis points lower than a year ago. You would not have expected to have seen this if supply constraints were the main reason for slower credit growth.

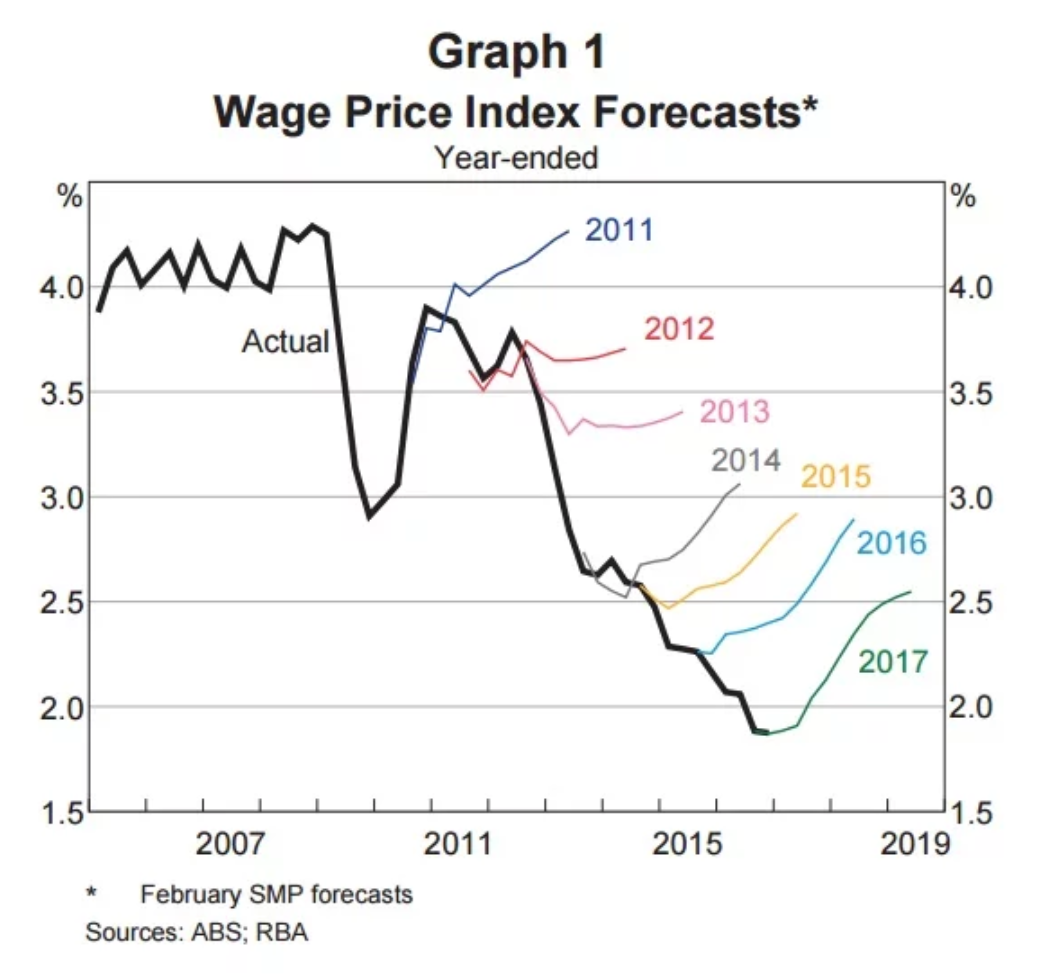

A third issue that the Board has focused on recently is growth of wages. As I have discussed previously, a lift in aggregate wages growth would be a welcome development from several perspectives. It would contribute to inflation being closer to the midpoint of the inflation target. Stronger income growth would also help in the context of high levels of household debt. It would also be of benefit to government finances and more generally would strengthen our sense of shared prosperity. And, to the extent that stronger wages growth is backed by stronger productivity growth, it would boost our real incomes.

We had another reading on the Wage Price Index a couple of days ago, which showed a welcome uptick. Over the past year, the Wage Price Index increased by 2.1 per cent and the broader measure, which captures bonuses, increased by 2.5 per cent. These figures are both up from a year ago. This week, we also received employment data for the month of July. While the month-to-month employment data are volatile, the unemployment rate has fallen to 5.3 per cent, which is the lowest it has been for some years.

Taken together, these data are consistent with our view that wages growth and inflation will pick up gradually over the next couple of years as the labour market continues to tighten. This tightening is evident in a number of indicators. The number of job vacancies, as a share of the labour force, is at a record high. Firms are reporting that it is harder to find workers with the necessary skills, and survey-based measures of hiring intentions remain positive. In our liaison program we also hear reports of larger wage increases for certain occupations where workers with the necessary skills are in short supply. We expect that we will hear more such reports over time.

Even so, the pick-up in wages growth is still expected to be fairly gradual. We still have some spare capacity in the labour market, including part-time workers who would like more hours. There are also structural factors at work, arising from technology and competition that we have discussed at previous hearings.

The fourth and related issue is the outlook for inflation.

The CPI inflation rate – at 2.1 per cent – is higher than it was a couple of years ago, but still below the medium-term average. Strong competition in retailing from new entrants is holding down the prices of many goods and low wage increases are holding down the prices of many services. Rent inflation is also at a very low level. Working in the other direction over the past year has been higher prices for electricity, fuel and tobacco.

We are expecting inflation to move gradually higher over the next couple of years as the economy strengthens. We remain committed to achieving an average rate of inflation over time of between 2 and 3 per cent.

In the short term, though, we are expecting the headline rate of inflation to dip a little in the September quarter. Utility prices have declined recently in some cities and policy changes are likely to reduce the measured price of child care. There have also been some policy changes at the state government level that will reduce other measured prices. Collectively, these changes will help with cost-of-living pressures and free up income to spend on other things. From this perspective, these changes are good news.

So these are some of the main issues we have been working our way through.

As you are aware, the Reserve Bank Board has held the cash rate steady at 1½ per cent since August 2016. This setting of monetary policy is helping support economic growth, allowing for further progress to be made in reducing the unemployment rate and returning inflation towards the midpoint of the target range. We have not sought to fine-tune outcomes, but rather to be a source of stability and confidence as the economy moves along this path.

For most of this year, I have emphasised three points in communication about monetary policy.

The first is that things are moving in the right direction. We are making progress towards full employment and having inflation return to around the midpoint of the target range, and further progress is expected.

The second point is that if we continue to make progress, you could expect the next move in interest rates to be up.

With the central scenario being for the economy to continue on its recent track, it is more likely that the next move in interest rates will be an increase, not a decrease. The last increase in the cash rate was back in late 2010, so an increase, when it occurs, will represent a significant change for many people. It is important to remember, though, that higher interest rates will be accompanied by faster growth in incomes than we have seen over recent times. In this sense, it will be a sign that things are returning to normal. Of course, higher rates will also be welcomed by many depositors, who have been earning low rates of returns on their savings over recent times.

The third point is that because the progress that is being made is gradual, and is expected to remain so, there is not a strong case for a near-term adjustment in interest rates.

The Board’s view is that it is likely that we will hold steady for a while yet. It is likely to be some time before we are at full employment and the inflation rate is comfortably within the target range on a sustained basis. We are prepared to maintain the current monetary policy stance until these benchmarks are more clearly in sight.

So these are our three recent messages on monetary policy.

On other matters, we are planning to release the upgraded $50 banknote in October. The new note will have the same high-tech security features as the new $5 and $10 notes. All up, there are around 700 million $50 notes on issue – that’s around 28 per person – so it is a big logistical exercise. You may have read in the press that there has been an industrial dispute at Note Printing Australia, which manufactures Australia’s banknotes in Craigieburn, Melbourne. I am pleased to be able to report that an in principle agreement on a new enterprise bargaining agreement was reached earlier this week and that we have sufficient notes to launch the new $50 in October as planned.

Finally, at previous hearings we have spoken about the New Payments Platform – the new payments system that allows Australians to easily make information-rich, real-time, 24/7 payments to each other, without having to know BSB and account numbers. Since the system was launched in February, 1.8 million Australians have registered a PayID – usually their mobile phone number – that can be used easily to address payments in the new system. The take-up of the system has, however, been less than earlier industry projections. This partly reflects the fact that a number of the major banks have been slow to make the new system available to their customers. They are now making it available, so we expect take-up to increase. Interestingly, many of the smaller financial institutions have done a better job, with more than 50 of them ready from day one. Despite the relatively slow start, we still expect that the new system will provide the bedrock upon which further innovation in Australia’s payment system will be built. The Payments System Board is keeping a close eye on access arrangements so that those with new ideas and better ways of doing things can use the new system.

Thank you. My colleagues and I are happy to answer your questions.

Nothing much to add. The RBA seems satisfied with the fall in house prices. It also believes that wages will continue to improve as the labour market tightens – essentially the same view that it has had for the past seven years:

And it believes the next move in interest rates will be up. Good luck with that.