Moody’s Investor Services has released a new report forecasting that Australian mortgage delinquencies will increase over the next two years as a record number of interest-only (IO) mortgages convert to principal and interest (P&I) loans. Moody’s also believes that refinancing interest-only mortgages will become more difficult, contributing to an increase in mortgage delinquencies:

Mortgage delinquencies will increase over the next two years because a record number of IO loans will convert to P&I loans. Higher mortgage delinquencies are credit negative for RMBS.

When IO loans convert to P&I, borrowers have to make higher monthly repayments. This “payment shock” can lead to mortgage delinquencies and makes IO loans riskier than P&I loans. IO loans typically have an IO period of five years, after which they convert to P&I. At current mortgage interest rates, monthly repayments on loans that convert to P&I from IO will increase by around 30%, which can lead to delinquencies.

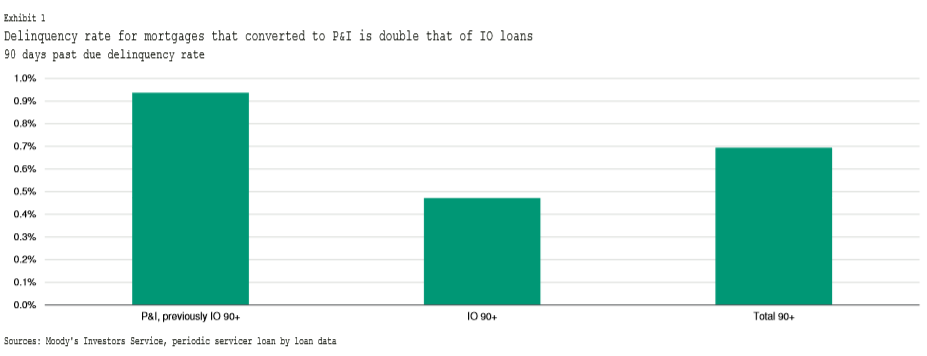

The 90-days past-due delinquency rate for securitised mortgages that have converted to P&I after an IO period was at 0.94% in November 2017, double that of IO loans that have not yet converted and around 0.24 percentage points higher than the overall delinquency rate for securitised mortgages (Exhibit 1).

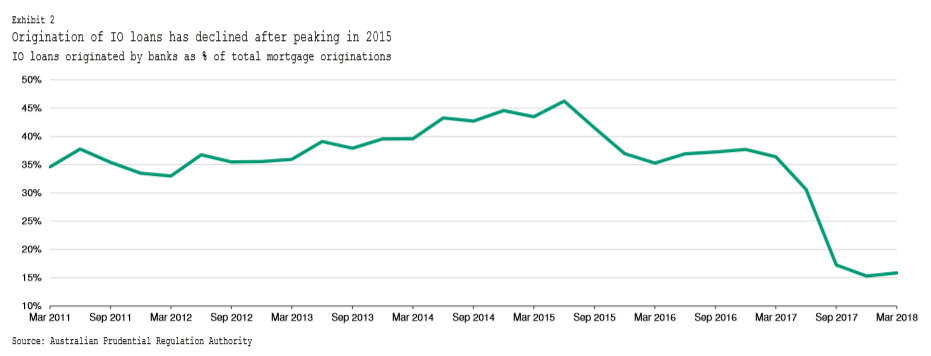

Banks originated a significant volume of IO loans in 2014 and 2015, which means a record number of these loans are scheduled to convert to P&I over 2019 and 2020, when the five-year IO period ends. IO loans accounted for more than 40% of all mortgages originated by banks for much of 2014 and 2015, with this figure peaking at 46% in June 2015 (Exhibit 2)…

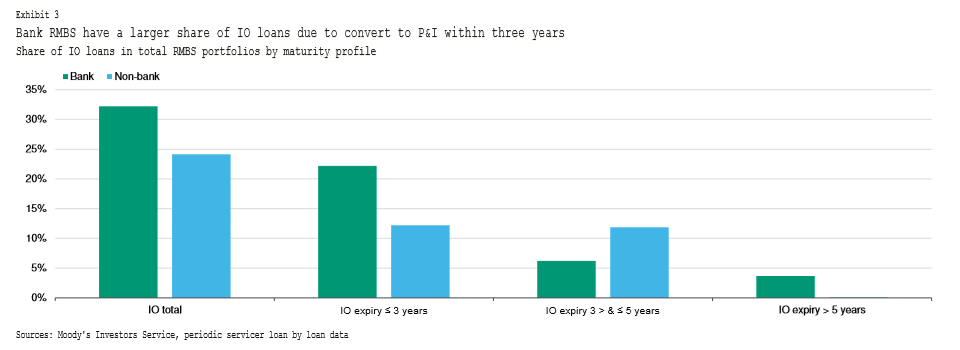

In bank-originated RMBS, IO loans account for about 32% of all loans. Around 22% of the loans in bank-originated RMBS are due to convert to P&I in the next three years, with 6% due to convert in three to five years and a further 4% to convert after five years. In RMBS originated by non-bank financial institutions, IO loans account for about 24% of all loans. Around 12% of loans are due to convert into P&I in the next three years, with the remaining 12% due to convert in three to five years (Exhibit 3)…

Regulatory measures introduced to reduce risks in the mortgage market have curbed the origination of IO loans, making it more difficult for borrowers to refinance their loans at the end of the IO period or extend the IO period for another term with the same lender. The more difficult refinancing conditions will contribute to an increase in mortgage delinquencies as the IO period on a record number of IO loans ends over the next two to three years…

Banks have also tightened loan serviceability criteria, resulting in a reduction, on average, in the amount they will lend, following a review of underwriting standards by APRA…

If house prices are declining when IO loan terms end, this will increase borrowers’ loan/value ratios and further limit their ability to refinance or result in a loss upon the sale of the property.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.