By Chris Becker

Yet another muted night on risk markets with European stocks largely positive before the US open, where only tech stocks and small caps advanced as the bigger issues dragged the headlines back to scratch sessions. It was a night for bond markets as yields tumbled after the US PPI print and a solid 30 year auction. The USD is again advancing, particularly against emerging markets currencies, while the Kiwi made even further losses against the majors after yesterday’s RBNZ re-weighting.

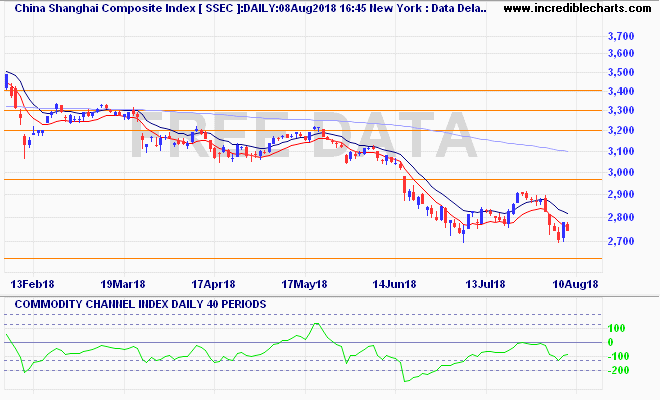

Recapping Asia’s session with Chinese stocks first, as the Shanghai Composite went through another volatile session, lifting almost 2% after the previous loss, closing at 2794 points on the back of a hotter than expected CPI print. Momentum remains negative here and given the ongoing trade war and the trajectory of the 200 day moving average (light blue line) there is still no reason to try to pick this monkey’s bottom:

The full text of this article is available to MacroBusiness subscribers