A hotter than expected Chinese CPI print has lifted stock markets outside of Japan, even as USD lifted against Yen throughout the session. Most action in currency markets was relegated to Kiwi after the RBNZ announcement this morning while gold continued its minor blip higher.

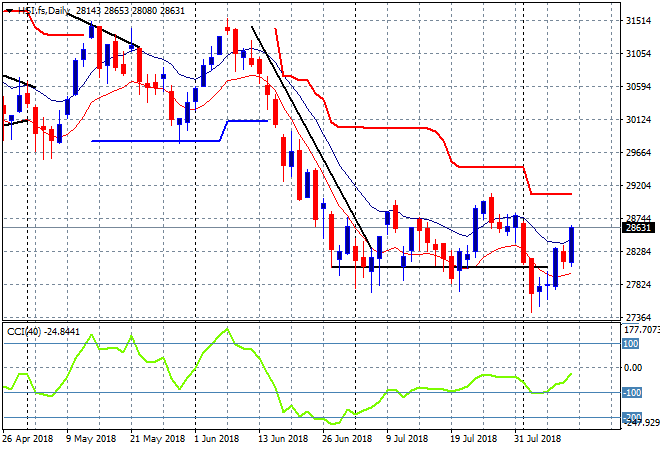

The Shanghai Composite is having another volatile session, lifting almost 2% after the previous loss, currently at 2737 points on the back of the CPI print. The Hang Seng Index also advanced, closing 1.3% higher to 28705 points, remaining above previous terminal support at 28000 points. Last week’s ominous breakdown on the daily chart still remains in play but this swing higher may turn into a substantive bounce:

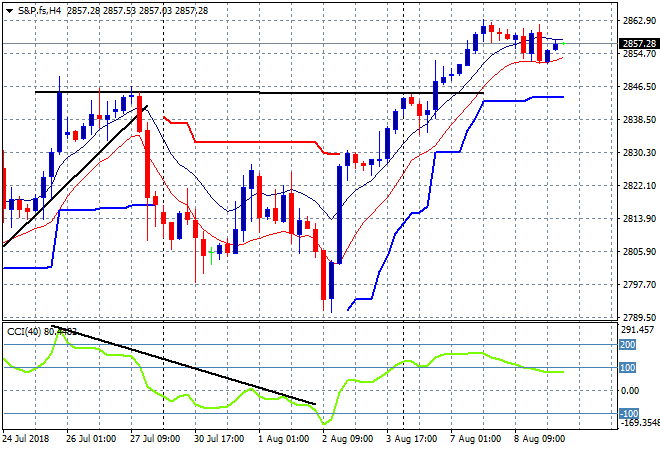

S&P futures are upslightly alongside Eurostoxx with the latter indicating a minor 0.1 to 0.2% lift higher in The City. There’s still daylight above to the 2880 level here for the S&P500 if the former high at 2860 is broken again:

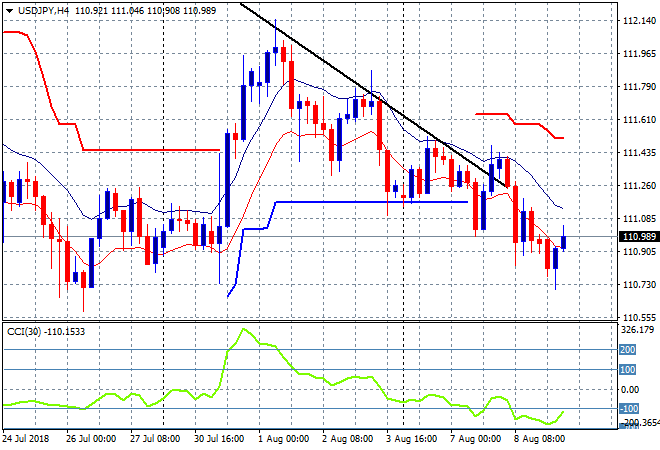

Japanese stocks have finished in the red again, despite the poorer showing by Yen, with the Nikkei 225 closing 0.2% lower at 22598 points, still vainly trying to get out of its sideways move on the daily chart. The USDJPY pair has come back so far in the Asian session, briefly touching the 110.70 level before rallying back up to just under the 111 handle. This still looks weak for mind, with the high moving average not under any pressure here:

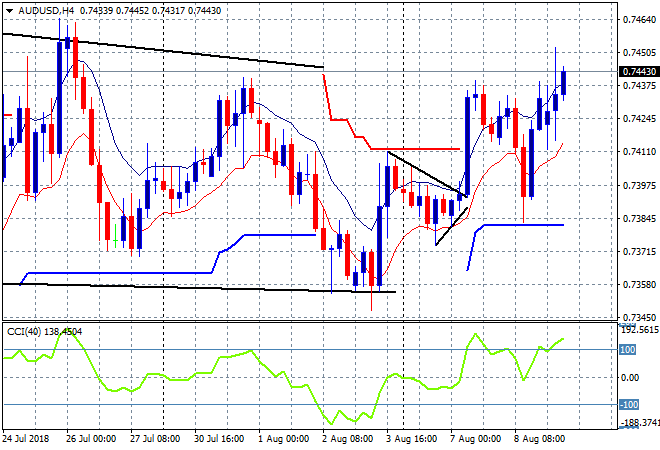

The ASX200 advanced again, lifting nearly 0.4% to close at 6297 points, almost able to breach overhead resistance at 6300 and displaying a lot of buying support below. The Aussie dollar continues its uptick, helped by the abandonment of Kiwi by other crosses, hitting a two week high at the 74.50 mid level going into the City open and ready to accelerate higher:

The economic calendar is again relatively quiet tonight with US initial jobless claims.