This post is dedicated to all of the Nervous Investors out there: you know who you are. You want to start investing, or invest more, but are frozen by a myriad of concerns:

- are you buying at the wrong time?

- you wanted to buy last year but didn’t get around to it, and now you are waiting until prices fall

- you can’t buy until you understand the difference between a fee and an ICR

- is the market about to crash?

- you don’t know what you are doing and so are worried at the next Royal Commission they’ll be using your investments as an example of all that is wrong with the system.

I have good news and bad news for you. The bad news is that as a Nervous Investor you will never find a perfect time to invest when everyone agrees that the markets are going to go up, you know everything you need to know and its safe to pile in. The good news is that I think I can help – and we also have a podcast out on the same topic.

I’m going to approach this from three angles:

- Why retail investors underperform professionals, so you can avoid the usual traps

- Typical assets, and how they typically perform so that you have an idea of the types of assets that you should own

- Five tips on what to do

Why retail investors underperform professionals

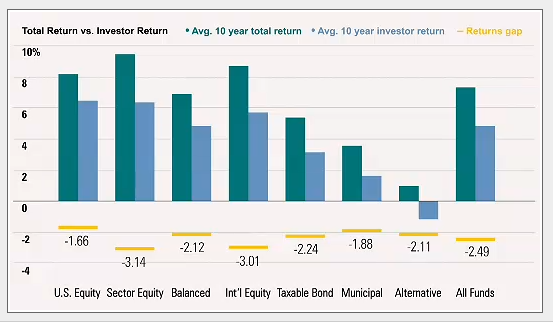

Morningstar regularly publishes studies showing that retail investors underperform by around 2% (and others think the gap is even larger):

Returns Gap

Source: Morningstar

The main factor is investor behaviour. When markets wobble, investors tend to sell or sit on their cash. When markets have been performing well, investors tend to invest their cash.

From a risk perspective, this might seem reasonable to the Nervous Investor – buy when risks seem low and sell when risks seem high.

But, from a return perspective, it is exactly the wrong strategy: buy high, and then sell low.

Your brain is actively working against you

What is clear from the studies is that the average investor in the heat of the moment makes poor investment decisions.

The media doesn’t help – they generally only report two things: (1) the markets are up a lot and you should have bought last week, get in quick before you miss out (2) the markets are down a lot and you should have sold last week, sell now before you lose the lot

Getting perspective is difficult, especially if you rely on newspapers, financial TV or stock brokers. The first two are in the entertainment business and so creating an exciting story trumps any obligation to give you a realistic perspective. Stockbrokers are in the business of making money from turnover, so convincing you to buy one day and sell a few weeks later trumps any obligation to give you long-term advice.

You need to recognise that the instincts that evolved with humans over thousands of years to stay alive on the savannah are ill-suited to investment. Some of the many recognised biases that are harmful to investing include:

- Loss aversion: Losses hurt more than gains. For a Nervous Investor, this might mean being overly conservative rather than taking calculated (and diversified) risks

- Confirmation bias: searching out facts that support our view rather than facts that challenge our view. For a Nervous Investor, it means looking for reasons to invest later. And the internet is a big place, I’m sure you’ll find someone who agrees with you.

- Planning fallacy: is our tendency to underestimate the time, costs, and risks of future actions and at the same time overestimate the benefits. For the Nervous Investor, this means “I’ll invest later after I have had time to learn the entire financial system and become knowledgeable about all of the risks”. But life gets in the way.

- Choice Paralysis: Too many choices overloads us. For the Nervous Investor, this is a never-ending excuse – you just need to research the choices more.

- Optimism bias: Humans are only correct about 80% of the time when we are “99% sure.”.

- Bias Blind Spot: We can see everyone else’s biases but not our own

The best way to overcome these biases? Create a plan and stick to it. More on that below.

Hindsight is 20/20

One of the most dangerous historical biases is judging a past decision by its ultimate outcome instead of based on the quality of the decision at the time it was made, given what was known at that time.

Humans are constantly rewriting history – especially anyone who writes about the markets the following two are staples of investment prediction:

- “Last year was much easier, all you needed to know was [INSERT THEME THAT IS KNOWN NOW BUT WASN’T 12 MONTHS AGO] – this year will be more difficult”

- “Last year was all about [INSERT ONE OF GROWTH / VALUE / QUALITY / MOMENTUM]. This year will be a stock pickers market” (its always a stock pickers market)

The reality is that investing is never riskless and there are always reasons for markets to fall or to rise – stocks “climb a wall of worry” is a more valid quote – meaning that stocks rise while a range of concerns keeps some people on the sidelines. The full quote being:

“If bull markets climb up a wall of worry, then bear markets slide down a slope of hope. A bull, or rising, market often begins in an atmosphere of gloom and skepticism when all sorts of reasons why prices should not rise prevail. The majority of market participants are bearish, thinking that prices will fall. On the other hand, when a bear market starts and prices begin falling, it is often in an overwhelming spirit of hope and optimism. The majority expects prices to rise.”

So, don’t re-write history. Yes, the market might have risen 20% last year, but it was never a “no-brainer”, no matter how obvious it may seem with hindsight. 12 months ago there were plenty of people warning of the dangers.

Typical assets, and how they typically perform

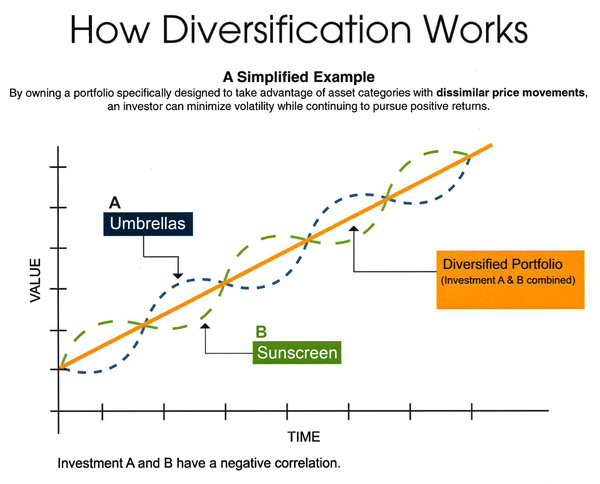

First, you want to diversify to smooth out your returns. For example, consider the apocryphal portfolio owning an umbrella seller and a sunscreen seller – some days one does well, other days the other does well. An investment in only one gives a volatile return, an investment in both smooths the return:

Cash / Term Deposits:

The big advantage of cash is that the value doesn’t fall in times of stress. The two main disadvantages are:

- Over the long term, cash gives a poor return relative to other assets.

- In times of trouble, central banks cut interest rates which flow through to cash balances almost immediately. If you are relying on the interest payments to live then this can create problems at the worst possible point of the economic cycle. While you can mitigate somewhat by using term deposits, now you have lost the liquidity of cash and may be up for break fees if you need to use it.

Most Nervous Investors will already be intimately acquainted with cash. The danger is that you own too much.

Government Bonds

The big advantage of government bonds is that in times of stress the value often (but not always, depending on the type of crisis) rises. This is hugely beneficial as it provides diversification when you want it most.

Bonds also provide a much steadier income relative to cash. What I mean by this is that bonds pay fixed amounts until they expire, and so if interest rates get cut then your bond portfolio might take 10 years to fully reflect the change in interest rates – very useful if you are living off the interest payments

The main downside is that the value of the bond does change, and so bonds are riskier than cash. Over the long term, bonds perform better than cash, but not as well as stocks.

Corporate Bonds

Corporate bonds provide a higher return (interest rate) than government bonds. The downside is that there is a much larger chance that the company you are investing in goes broke vs investing in government bonds.

This then manifests itself in a poorer level of diversification. i.e. when the economy goes through times of stress, more companies default and even the value of corporate debt for companies that don’t default declines.

This makes the returns for corporate debt more similar to stock market returns – meaning that for the Nervous Investor corporate debt is less useful.

Stocks

Stocks are the most volatile – in boom times they will return the most, in bust times they will lose the most. As a Nervous Investor you want to have a diversified weighting to stocks over the long term, but keeping this exposure to a level that you feel comfortable is important.

Five Areas of focus on for the Nervous Investor

1. Asset Allocation:

Get your strategy right and then stick to it. Write it down. Put it somewhere safe and refer to it before you make any investments. As a Nervous Investor, don’t let your emotions rule.

Diversify. Diversify. Diversify. Very useful for ordinary investors, doubly so for a Nervous Investor.

2. Regret Minimisation:

As a Nervous Investor, you need to realise that every investor is wrong at some stage. Your goal as an investor is not to make zero mistakes, its to make sure that your mistakes don’t ruin your portfolio. Accept that mistakes will be made, but we are trying to minimise the level of regret.

First, evaluate the fear vs greed trade-off. If you really want to be the person at the BBQ talking about how much you made on the stock market, then you are going to have to take some risk. And some years you are going to have to own up to some big losses. For many Nervous Investor’s, this is unrealistic – abandon your dreams of being the hare and embrace the role of the tortoise.

Second, don’t invest all at once. Make a plan, for some this will mean gradually investing over a few months, for others, it will mean gradually investing over a few years. Stick with your plan. You will probably be alternatively kicking yourself for not investing earlier and then berating yourself for not waiting for the market to fall. Accept that now and move on.

3. Self Evaluation:

- Do you have the knowledge to make investment decisions? If not get a professional to do it. If you “just need to read up on a few more things”, then get a professional to do it for you in the meantime, just in case it takes you a few years longer than you expect.

- Do you have the temperament to make investment timing decisions? If not get a professional to do it. You need to stick to your plan above – as a Nervous Investor if you are unsure of your ability to do so, then leave it to the professionals.

4. Self Control:

Rebalance regularly. As a Nervous Investor, this will be a painful process because it will entail selling assets that are doing well and buying assets that have done poorly. Do it anyway.

For many investors, near the end of the tax year is a good time.

Don’t watch every market tick. Once your plan is set up and running, turn off the live prices and financial news. As a Nervous Investor, they are going to pander to your worst instincts.

5. Analysis Paralysis:

As a Nervous Investor, you are probably already a few years overdue to “do something”. Do something is far better than doing nothing.

If you are really nervous then write down a longer-term plan to start investing – take years to be fully invested if that is what you feel comfortable with. But start.

—————————————————-

Damien Klassen is Head of Investments at the Macrobusiness Fund, which is powered by Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.