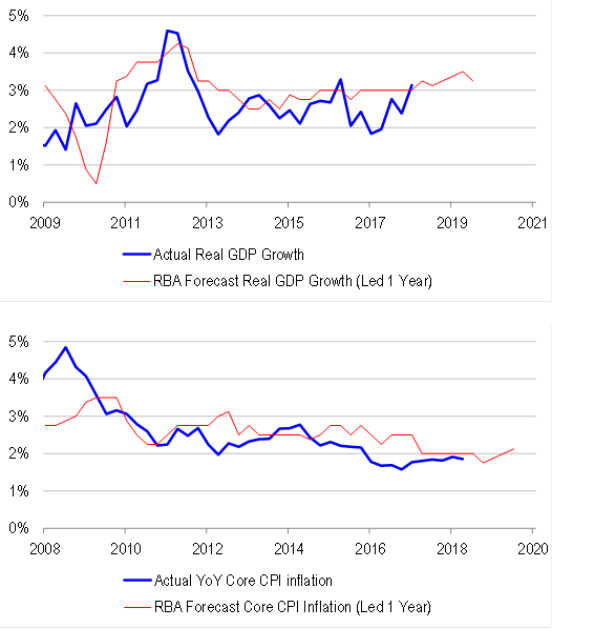

The RBA’s August Statement on Monetary Policy (SoMP) was a little hawkish, with Bank officials suggesting that higher rates are likely to be appropriate at some point if the economy evolves as they expect. However, they do not see a strong case for near-term adjustment.

Growth forecasts were revised slightly lower for FY19 to 3.25% from 3.5%.

Inflation forecasts were revised lower in the short-term, but slightly higher medium-term. The forecast for 4Q 2018 inflation was cut to 1.75% from 2%, reflecting the impact of declines in administered goods and services prices. But offsetting this, the forecast for 4Q 2019 was revised higher to 2.25% from 2%.

Overall, the Bank is a little less positive on growth, but more positive on inflation for the year ahead.

In terms of risks, officials have become a little more concerned about the downside risks to growth from trade protectionism and China. Indeed, they are forecasting moderation in commodity prices and the terms of trade. They also see upside risks to US growth and the prospect of a faster pace of Fed tightening than what the market has currently priced in. All of this could weigh on the AUD/USD.

Effectively, officials believe that a decline in the AUD/USD will help to cushion the local economy against domestic risks. This is the first time in quite a while that the RBA has tried to jawbone the currency lower.

Assessment:

We think that the Bank’s forecasts for growth and inflation are too high. We do not think that the Bank has gone far enough yet in downgrading its assessment of activity. And nor could it have, in order to justify its stated stance on policy.

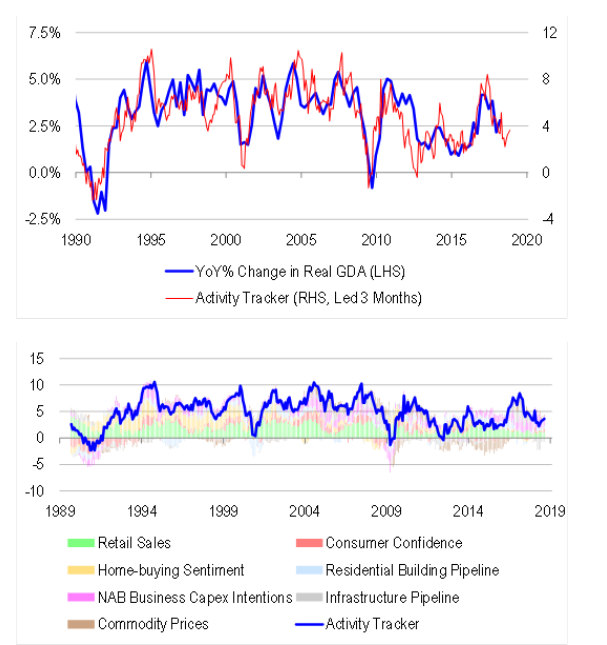

On growth, our proprietary activity tracker points to sub-trend, rather than above-trend activity growth in the coming months. Our tracker is based on high frequency partial indicators such as retail sales, consumer confidence, business confidence, home-buying sentiment, building approvals, the depth of the infrastructure capex pipeline and commodity prices. With trend retail sales growth remaining soft (notwithstanding recently positive data), business confidence moderating, home-buying sentiment remaining weak, and commodity prices falling our activity tracker has been held down. To be sure, the indicator has ticked higher recently on the back of positive housing, and infrastructure spending data. But overall, it points to activity growth below 2.5%, and certainly well below the RBA’s 3%+ forecasts. Interestingly, this is all before we even consider the incremental impact of credit and money market tightening, which has only just started to surface in the credit data.

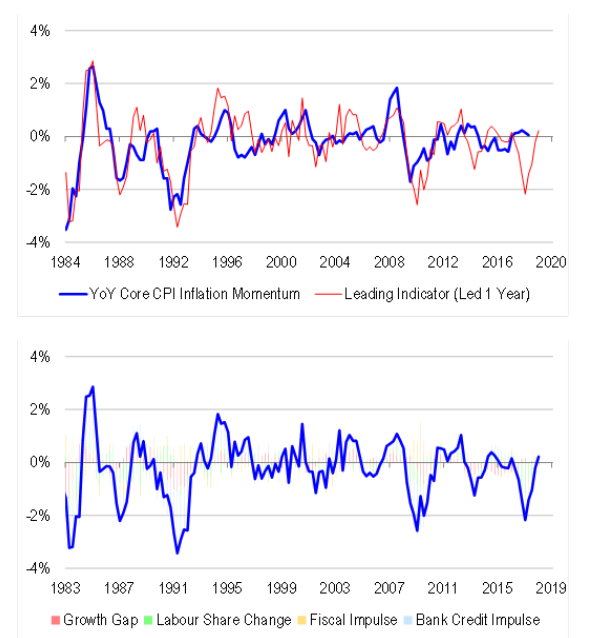

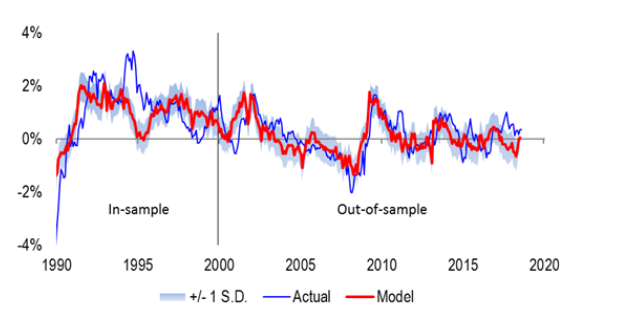

On core CPI inflation, our leading indicator points to negative, rather than positive momentum. That is, while the RBA is forecasting inflation to drift higher, the balance of risks are actually tilted lower based on leading drivers. Our inflation leading indicator is based on the deviation of activity growth from trend, the rate of change in the labour share of GDP (a proxy for shifts in wage bargaining power), the credit impulse (a proxy for changes in the pace of private money creation), and rate of change in the fiscal deficit as a share of GDP (a proxy for changes in the pace of public money creation). The net balance of these factors is pointing to lower inflation because credit growth is slowing, activity growth is not above trend, and fiscal austerity is starting to bite. The main positive in the data is that the labour share of GDP is rising – but historically, this variable lags behind activity growth.

Investment and policy implications

RBA Governor Lowe has made it clear that the RBA will not cut rates regardless of any undershoots in growth and inflation, and is prepared to hike rates quickly if activity growth and inflation exceed the Bank’s forecasts. But the RBA’s growth and inflation forecasts are very optimistic, as they have been consistently for some time. Also, bond market investors are clearly not buying into the Bank’s view, because the yield curve is not steepening. It appears that investors want to see what the economy looks like after credit tightening has manifest in the data, with early signs not looking very encouraging. Interestingly, recent open-ended commentary from the RBNZ (that rates could rise or fall in the foreseeable future), who face very similar circumstances to the RBA, suggest that our peers across the Tasman do not agree with the Bank’s stoic hawkishness.

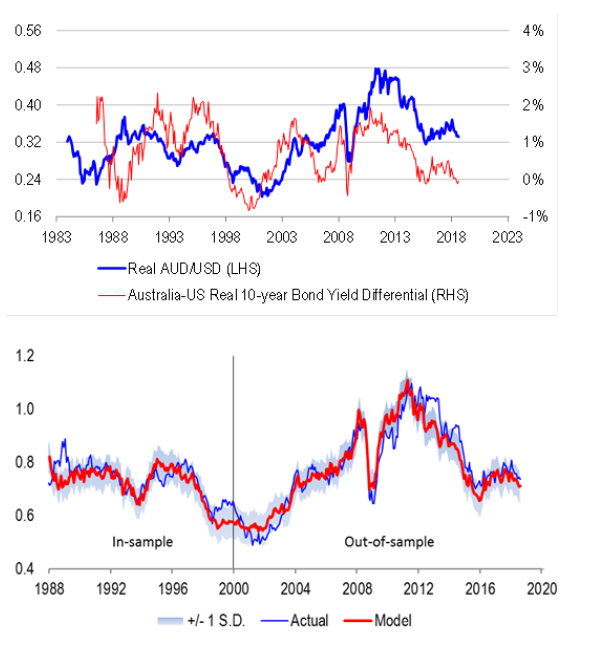

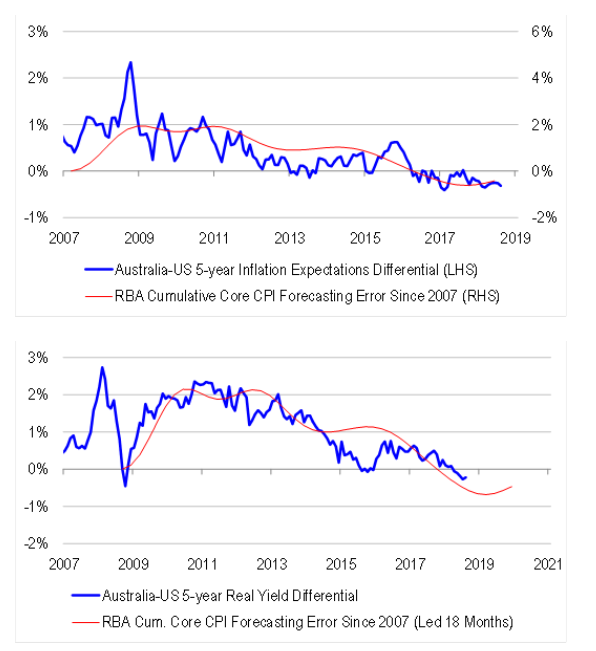

The leading indicators we follow point to much lower growth and inflation outcomes than the RBA is forecasting. Disappointment is likely to erode the Bank’s inflation-targeting credentials, and drive a wedge between global and domestic inflation expectations. In turn, this could contribute to greater inversion of Australian-US yield differentials, undermining the carry trade appeal of the currency. On current yield differentials and commodity prices, the equilibrium level of the AUD/USD is around 71c. But we could easily see yield differentials become more negative to the tune of another 50bps. In turn, this could drive the equilibrium level of the currency into the 60s.

While we sympathize with the RBA’s negative tone on the AUD/USD, we do not think that a weaker AUD/USD will necessarily stimulate the local economy. This is because our reasons for seeing the balance of risks tilted to the downside are all growth negative – poor domestic growth, and weakness in China leading to inversion of yield differentials and possible weakness in commodity prices.

Also, there is considerable scope for curve flattening. Our model of the real yield curve, based on the NAB survey confidence-conditions spread, home-buying sentiment, USD funding availability and RBA “Taylor” rule points to a completely flat slope, with some risk of undershooting into inversion territory. Note that our RBA “Taylor” rule captures much of the Bank’s current thinking about rates – that with the unemployment rate low, and activity growth being healthy in early 2018, there may be room to hike rates to around 2%, on the assumption of full pass through to effective borrowing rates. However, our curve model also suggests that the RBA’s narrow criteria for setting rates is incomplete. Housing and money market conditions matter at least as much as labour market conditions and inflation, and these “other” factors point in the opposite direction to the Bank’s intended trajectory for rates.

If we are in a regime biased towards currency weakness and curve flattening, history tells us that we ought to be defensively positioned within the equity market. We are currently overweight high quality industrial exposures (especially those with USD earnings exposure) relative to banks, domestic cyclicals and resources.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

While we sympathize with the RBA’s negative tone on the AUD/USD, we do not think that a weaker AUD/USD will necessarily stimulate the local economy. This is because our reasons for seeing the balance of risks tilted to the downside are all growth negative – poor domestic growth, and weakness in China leading to inversion of yield differentials and possible weakness in commodity prices.Also, there is considerable scope for curve flattening. Our model of the real yield curve, based on the NAB survey confidence-conditions spread, home-buying sentiment, USD funding availability and RBA “Taylor” rule points to a completely flat slope, with some risk of undershooting into inversion territory. Note that our RBA “Taylor” rule captures much of the Bank’s current thinking about rates – that with the unemployment rate low, and activity growth being healthy in early 2018, there may be room to hike rates to around 2%, on the assumption of full pass through to effective borrowing rates. However, our curve model also suggests that the RBA’s narrow criteria for setting rates is incomplete. Housing and money market conditions matter at least as much as labour market conditions and inflation, and these “other” factors point in the opposite direction to the Bank’s intended trajectory for rates.If we are in a regime biased towards currency weakness and curve flattening, history tells us that we ought to be defensively positioned within the equity market. We are currently overweight high quality industrial exposures (especially those with USD earnings exposure) relative to banks, domestic cyclicals and resources.

While we sympathize with the RBA’s negative tone on the AUD/USD, we do not think that a weaker AUD/USD will necessarily stimulate the local economy. This is because our reasons for seeing the balance of risks tilted to the downside are all growth negative – poor domestic growth, and weakness in China leading to inversion of yield differentials and possible weakness in commodity prices.Also, there is considerable scope for curve flattening. Our model of the real yield curve, based on the NAB survey confidence-conditions spread, home-buying sentiment, USD funding availability and RBA “Taylor” rule points to a completely flat slope, with some risk of undershooting into inversion territory. Note that our RBA “Taylor” rule captures much of the Bank’s current thinking about rates – that with the unemployment rate low, and activity growth being healthy in early 2018, there may be room to hike rates to around 2%, on the assumption of full pass through to effective borrowing rates. However, our curve model also suggests that the RBA’s narrow criteria for setting rates is incomplete. Housing and money market conditions matter at least as much as labour market conditions and inflation, and these “other” factors point in the opposite direction to the Bank’s intended trajectory for rates.If we are in a regime biased towards currency weakness and curve flattening, history tells us that we ought to be defensively positioned within the equity market. We are currently overweight high quality industrial exposures (especially those with USD earnings exposure) relative to banks, domestic cyclicals and resources.