While the Turnbull Government continues to pursue suicidal company tax cuts on the faux promise of boosting ‘jobs and growth’, New Zealand’s Tax Working Group (TWG) – which is due to release its interim report to New Zealand’s Labour Government in the next month – has all but rejected the idea.

At 28%, New Zealand’s company tax rate is relatively high by international standards… As at 2017 New Zealand’s company rate is the 10th highest in the OECD, with the unweighted OECD average being 24.9%…

For domestic shareholders, New Zealand’s imputation regime means that the final tax rate on investments in companies is normally taxed at the shareholder’s marginal tax rate2. When factoring in imputation, New Zealand’s tax rate on domestic shareholders is the sixth lowest in the OECD. Foreign shareholders do not receive imputation credits and for them it is the company rate that is relevant…

Investments funded by equity are subject to full taxation at the 28% company tax rate on the income generated by their New Zealand operations. On the other hand, as noted above in paragraph 14, for investment funded by debt, the interest paid is deductible against the income tax base in New Zealand. Accordingly, the New Zealand tax paid on the underlying income is the NRWT (non-resident withholding tax) at a rate of 10% or 15%, depending upon whether the residence country of the parent is a treaty country or not…

Sometimes commentators suggest that New Zealand should cut its company rate to be “competitive”…

In terms of competition for tax base, lower rates overseas may incentivise firms to shift profits out of New Zealand into a lower-tax country with deductible payments such as interest, or transfer pricing measures… Having said that, lowering tax rates is likely to be an expensive way to reduce profit shifting, since it lowers taxes on the tax base that remains in New Zealand.

In terms of competition for business headquarters,.. for New Zealand companies with a substantial New Zealand shareholder base, the New Zealand tax settings mean it is advantageous to remain New Zealand headquartered (as tax paid in foreign jurisdictions cannot be passed on as a credit to New Zealand shareholders, whereas New Zealand tax can).

…on competition for foreign capital, the international “competition” aspect is sometimes overstated. Generally, if an investment makes sense in New Zealand with a 28% company tax rate, it does not suddenly become uneconomic because a foreign country drops its rate from (say) 30% to 25%…

Much FDI to New Zealand may be associated with supplying goods and services to domestic markets. At least traditionally, it will often be hard to do this without establishing a base in New Zealand. In this case, tax is much less likely to play a critical factor in investment decisions. If companies can supply goods and services to New Zealand without a physical presence, then the company tax will not apply to them anyway (under current frameworks) and so the company tax is irrelevant…

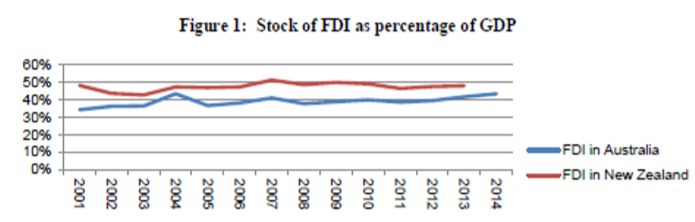

As illustrated in Figure 1 below, the two recent reductions in the company tax rate in New Zealand (from 33% to 30% on 1 April 2008 and from 30% to 28% on 1 April 2011) did not cause a surge of FDI into New Zealand. Nor did it show up in New Zealand’s level of FDI increasing relative to Australia’s. Australia had no cut in its company rate over this period…

A further caution against cutting the company rate is that this would mean reducing taxes on location-specific rents. Economic rents are returns over and above those required for investment in New Zealand to take place. Location specific rents arise from factors that are linked to a location. Such factors could include resources, or access to particular markets that allow above-normal profits to be earned. Economic rents are likely to be larger in a geographically isolated market like New Zealand where supply of certain goods and services is likely to require a physical presence in New Zealand…

Economic rents are an efficient source of taxation, but are especially valuable when they are earned by non-residents. Because New Zealand gains (through greater tax revenue) but does not bear any of the costs, New Zealanders gain at the expense of non-residents. When the economic rents of New Zealanders are taxed, New Zealand gains at the expense of particular New Zealanders.

A cut in the company tax rate will also provide windfall benefits to those who have invested in New Zealand in the past…

A reduction in the New Zealand company rate would negatively impact on the integrity of the overall tax system as people would be likely to shelter income in companies to avoid the top personal rates. The top personal tax rate, and the rate for trusts, is 33%. The 5% rate differential between the company and personal tax rates already encourages tax-sheltering arrangements, and the rewards from these arrangements increase the greater the differential.

All of this leads us to conclude that, on balance, in the judgement of the Secretariat it would not be in New Zealand’s best interests to lower the company tax rate.

Far more sensible analysis than anything that has come out of the Australian Treasury or the ‘growth lobby’.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.