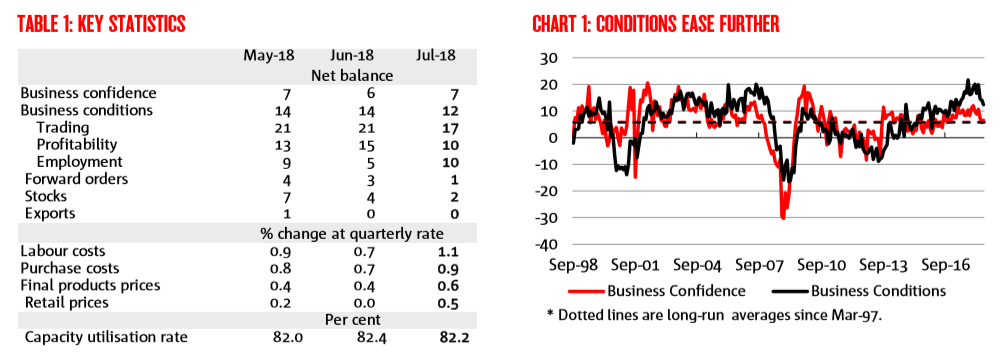

How confident are businesses? The business confidence index ticked up 1pt to +7 index points in July and remains around average.

How did business conditions fare? The business conditions index fell 2pts to +12 index points following an unchanged outcome in June. Conditions remain well above the long-run average of +6 but have now eased notably since April.

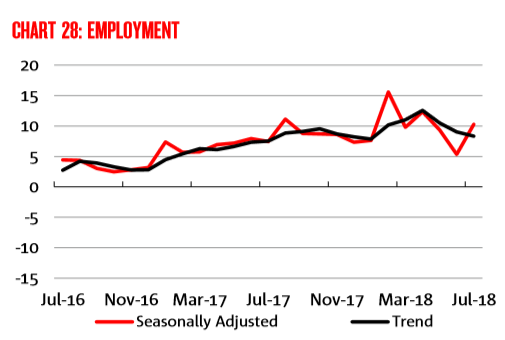

What components contributed to the result? The trading and profitability indices fell in the month (by 4 and 5pts respectively), while the employment index rose to +10 index points (reversing last month’s decline).

What is the survey signalling for jobs growth? The employment index – based on historical patterns – is consistent with jobs growth around 23k per month, which should see the unemployment rate continue to edge lower over the rest of 2018 (see page 2 for a more detailed look at the survey measure of employment).

Which industries are driving conditions? Conditions fell in manufacturing , retail , finance, business & property , transport & utilities , and mining in July . This was partially offset by a sharp increase in construction and smaller increases in personal & recreation services and wholesale . In trend terms, conditions remain highest in mining , construction and finance, business & property services . Retail remains weakest.

Which industries are most confident? Confidence remains highest, in trend terms, in the mining (+32) and construction (+11) industries. Confidence is lowest in transport & utilities and manufacturing ; the remaining industries remain at or around the national average.

Where are we seeing the best conditions by state? Conditions (in trend terms) remain most favourable in Tasmania (+19) , Queensland (+17) and Victoria (+16) though all states remain at or well above average. Conditions in Western Australia continue to lag the other states as they have done for some time now.

What is confidence like across the states? In trend terms, confidence is highest in South Australia (+10), followed by Western Australia and Queensland (both +9). Confidence in N ew South Wales and Victoria was again the weakest (both +4).

What does the Survey suggest about inflation and wages? Surveyed price, cost and wage variables generally edged higher in the month, though overall continue to suggest weak price pressures in the economy. Labour cost, purchase cost and final products prices growth all rose in July. Retail inflation picked up in the month after a flat outcome in June – though still remains relatively weak.

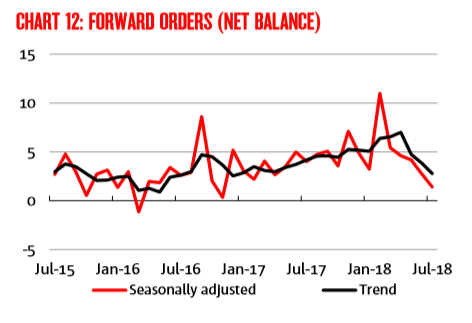

Are leading indicators suggesting further improvement? The forward orders index declined again, falling to +1 which is around its long-run average. Capacity utilisation edged slightly lower in July, but remains above average after trending higher over recent years.

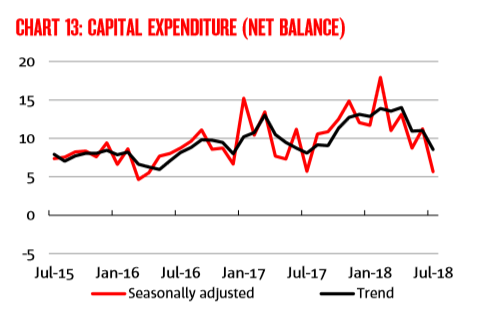

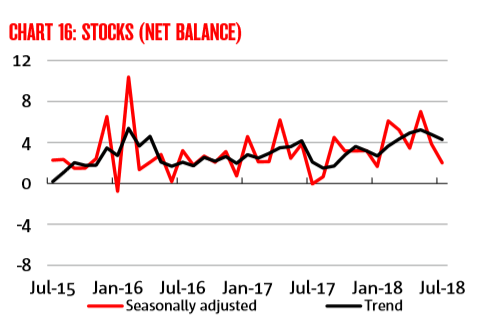

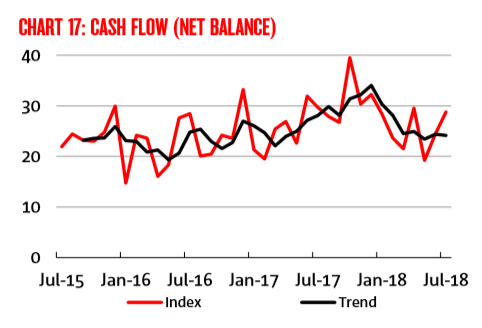

NAB should re-read its own survey. The key internals are weakening with forward orders, stocks, employment, cash flow and capex all down:

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.