Bankruptcies to rise as negative mortgage equity spreads

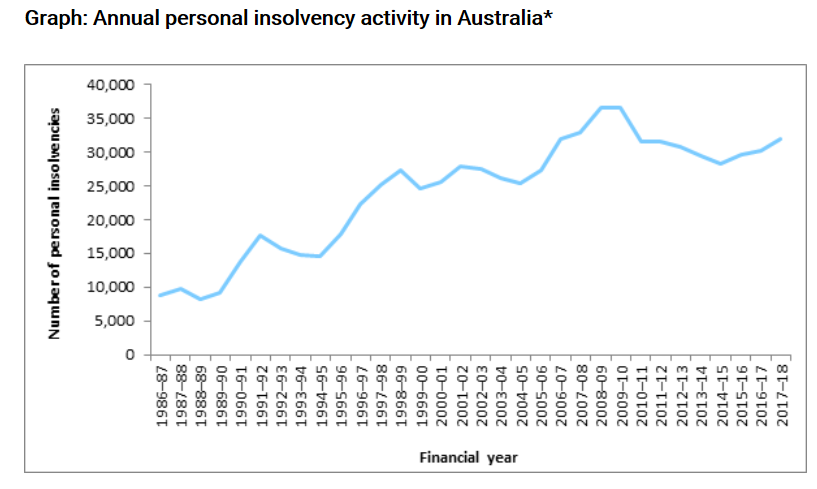

Last month, the Australian Financial Security Authority (FSA) released personal insolvency statistics for 2017-18, which revealed a sharp rise in total personal insolvencies to the highest level since the Global Financial Crisis (GFC):

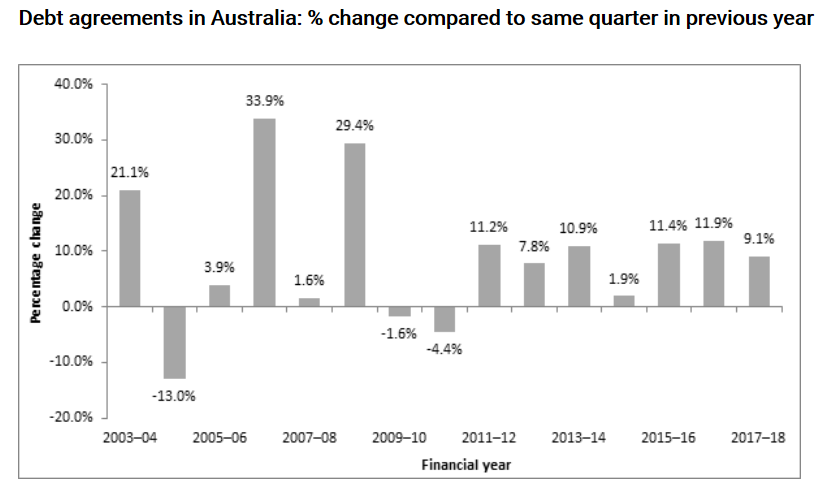

In particular, debt agreements hit the highest annual number on record in all states and territories except Tasmania after posting the seventh annual increase:

Now, data analytics company illion has released data showing that more than 32,000 Australians declared personal bankruptcies in 2017-2018, an eight year high:

Personal bankruptcies across Australia are at an eight-year high and experts are warning that a combination of rising debt, stagnant wage growth and falling house prices could herald more bad news for people living on the east coast…

illion CEO Simon Bligh… warned that a combination of rising debt levels, stagnant wage growth and falling house prices could mean more personal bankruptcies for Australians on the east coast.

Almost 6000 people in NSW declared bankruptcy in the last financial year, which was a 7.6 per cent increase from the previous year…

illion’s economic advisor Stephen Koukoulas said… “A lot of small businesses leverage their business borrowings with the security of their mortgage.

“When the housing market turns down, like in Perth and Darwin in particular, and we’re just starting to see that in Sydney, the banks are less inclined to extend that line of borrowing”…

Mr Bligh expected NSW and even Melbourne to see an uptick in personal bankruptcies as further forecast falls in the property market took effect.

“The lights are flashing red across several regions in terms of rising consumer stress levels,” Mr Bligh said.

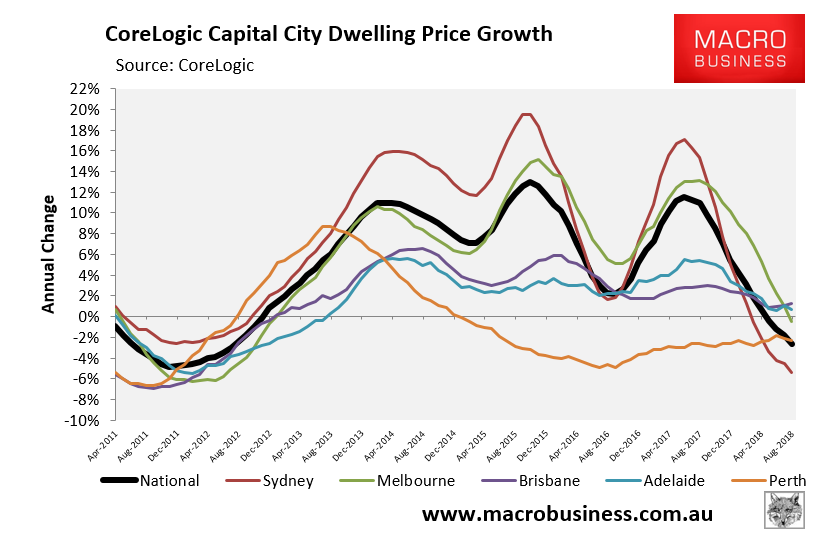

Australia’s housing downturn is just getting started, led by Sydney:

And even now, suburbs in Sydney’s inner west have taken a hammering with several suburbs posting double-digit losses in the year to June:

These price moves do not match the auction clearance rates which have been much worse in the Sydney mortgage belt, the ring of homes further out. This suggests that this correction has much further to run given outer ring prices obviously have further to fall and that will impact the move-up ladder which moves from out to in.

Hence, Sydney is on the verge of a much larger wave of price falls and negative equity than it experienced during the 2003 correction, along with a likely surge in personal bankruptcies.

Melbourne’s property correction is not as advanced as Sydney’s, but appears headed the same way.

With no sign of an end to price falls, an ongoing reset for interest-only loans for another three years, rising bank funding costs and mortgage rates, a fading economy with no inflation nor real wage rises, plus an aged cycle heading into some kind external shock, the whole system is about to be tested. And this is before you factor in Labor’s negative gearing and capital gains tax restrictions in the likely event that it wins the upcoming federal election.

The only saving grace is that the RBA will probably be forced to cut rates some time next year. But with the cash rate already at just 1.5%, and the banks certain to keep half of any cut, they are unlikely to stem the pain.