Housing finance approvals data for June came in below expectations. The value of owner-occupier loans fell by 1% over the month, while the value of investment lending fell by 2.7%.

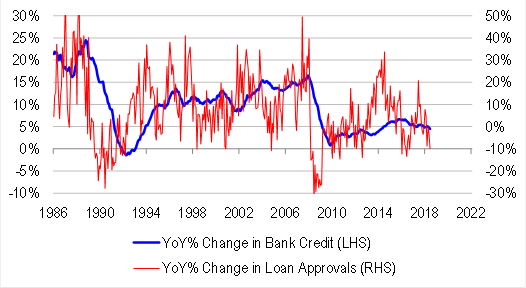

We do not yet have the complete lending finance data set, which also accounts for commercial and personal loans. But if we were to flat-track the missing data for June, net loan approvals would fall by 0.1% over the month, taking year-ended growth sharply lower to -10% from -3.7%.

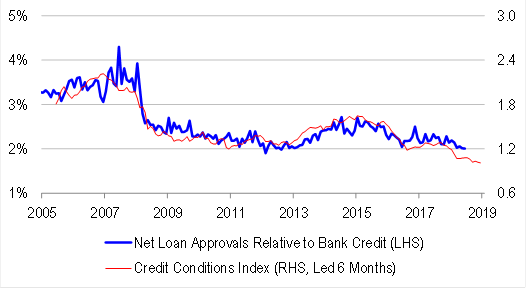

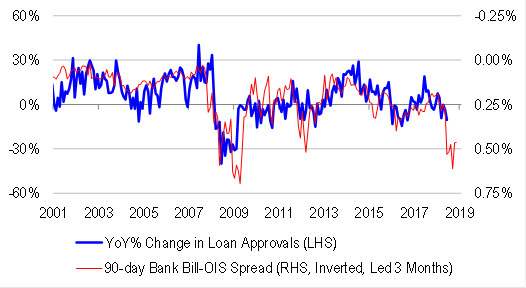

The data are evolving broadly in line with leading indicators. Our proprietary credit conditions index, which takes into account reported mortgage lending standards and credit spreads, has been pointing to weakness in loan approvals for some time. Interbank credit spreads point to an even sharper decline shorter-term.

On the basis of either leading indicator, there is much more weakness in loan approvals to come. Indeed, high frequency data from CoreLogic has not been pretty recently.

Should loan approvals fall sharply, we should expect credit growth to slow as well, because flows ultimately lead stocks. And with government spending tightening up in FY19, we should expect overall money supply growth to slow as well, consistent with disinflation in the economy.

Investment and policy implications

Falling house prices and slowing credit growth are serious problems for the economy. They threaten to derail the RBA’s current outlook on growth and inflation. The worrying thing is that we may only be seeing the tip of the iceberg in the available data, with historical relationships suggesting that it will take more time for recent credit and money market tightening to flow through the system.

While the RBA has made it clear that it does not plan to adjust rates any time soon, the disinflation coming through needs to be priced in. As such, there is considerable scope for curve flattening and further inversion of Australian-US yield differentials, undermining the carry trade appeal of the currency. Within the equity market, this sort of macro environment favours high quality industrials over banks and domestic cyclicals.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.