DXY is off to the races. CNY held and EUR is cooked:

The Australian dollar tumbled again versus developed markets (DM):

And emerging markets (EM):

Gold held on:

Oil didn’t:

Nor base metals:

Big miners are breaking down:

EM stocks sank fingernails into the clifftop:

EM junk bounced:

Treasuries were sold:

Bunds too:

Italy is aflame:

US stocks don’t care:

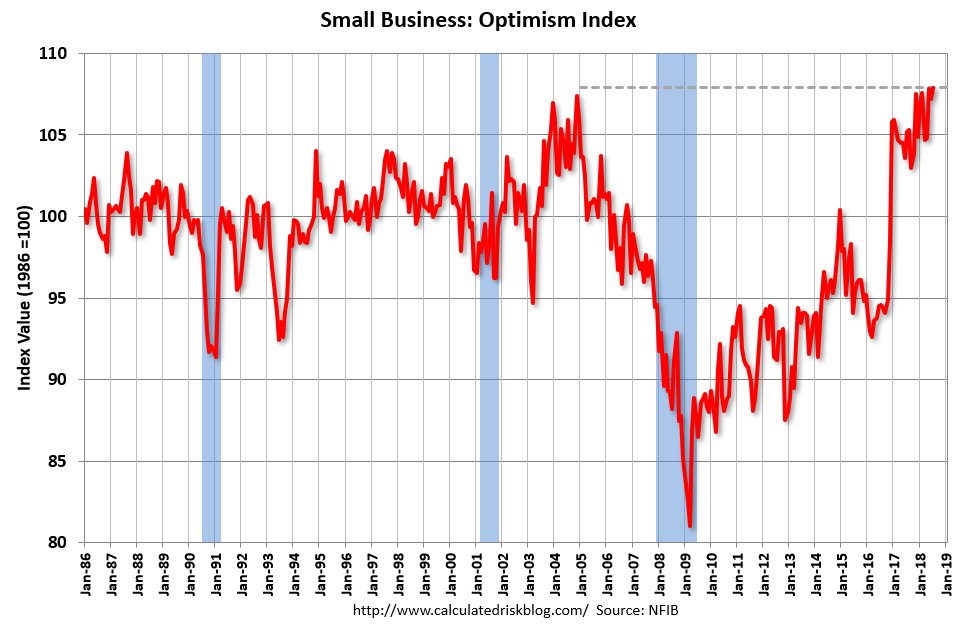

US data was solid with small business booming:

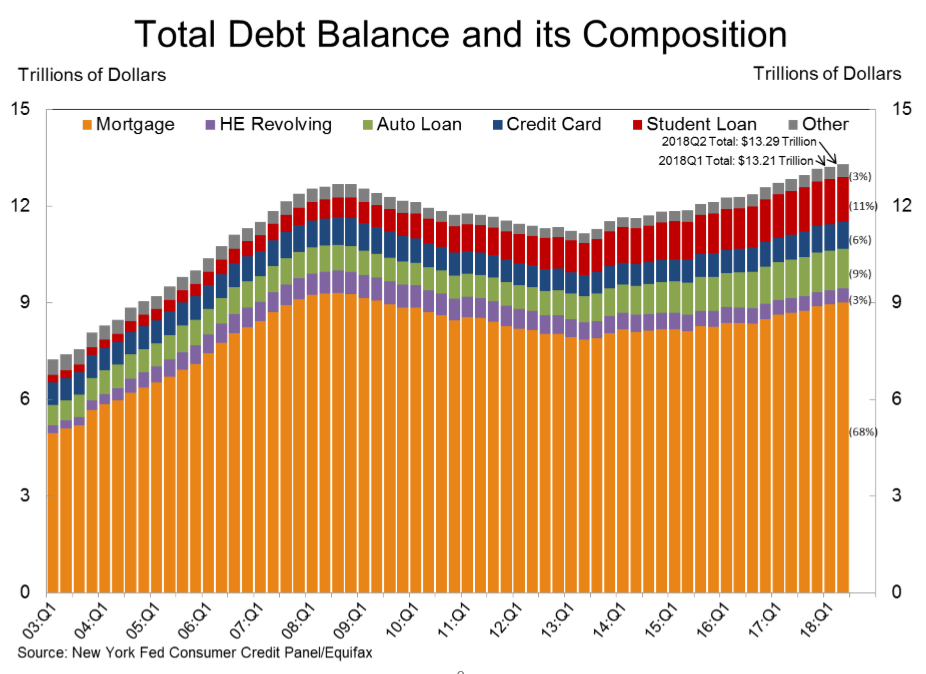

And household credit piling on:

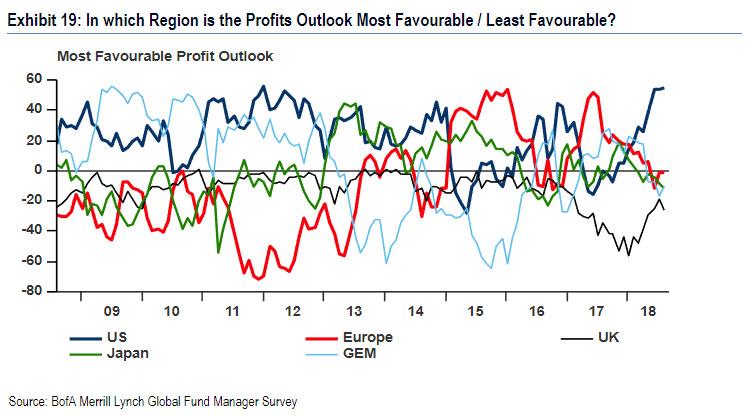

Fundies can’t get enough of US profits, via BofAML:

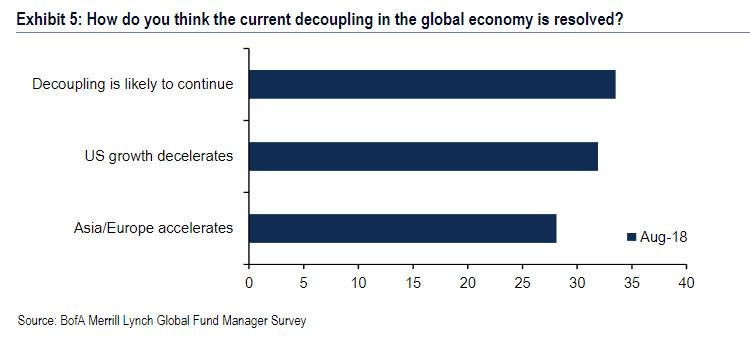

But think a US slowdown will bring it back to the pack:

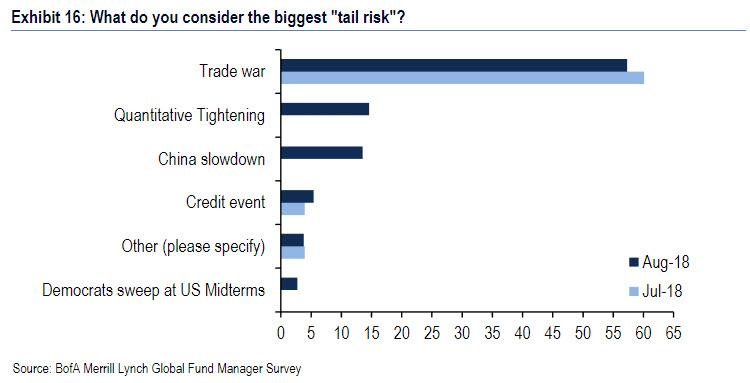

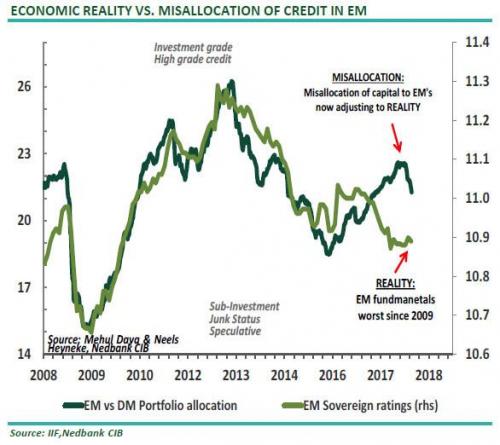

The big risks are all EM and China:

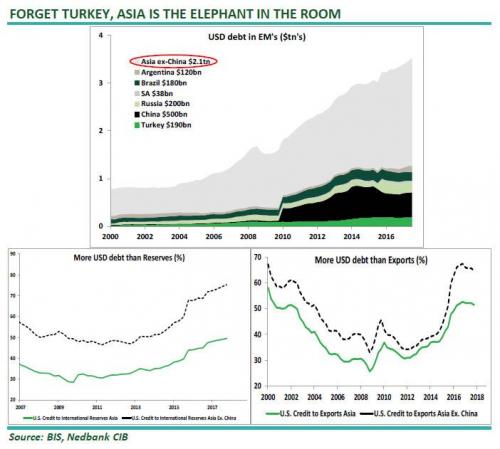

Turning to the EM crisis and Turkey, it’s just not big enough!

Thought the crisis will deteriorate as the US powers on:

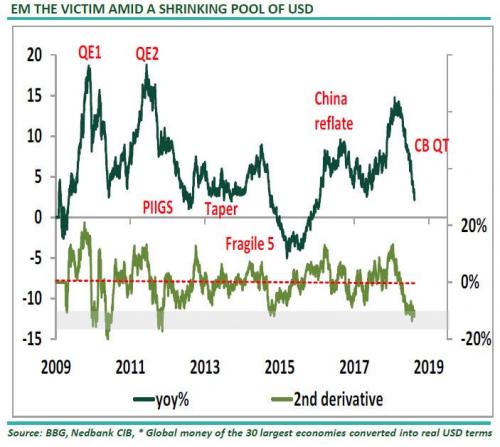

Sucking away the USD lifeblood:

From Asia next:

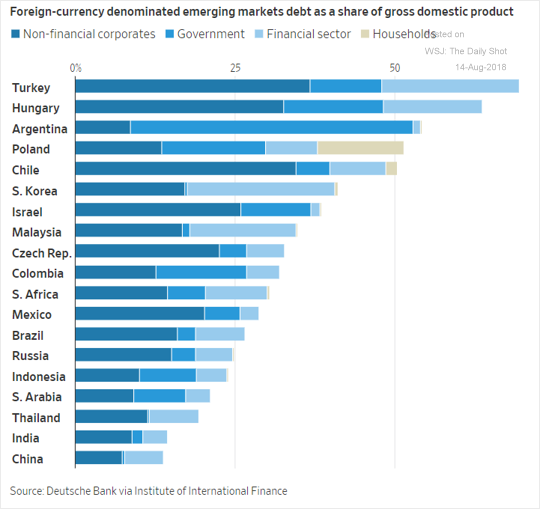

But it’s not obvious who is vulnerable:

So, it’s onwards and upwards for now. China is slowing and easing with more of both ahead, made worse by the looming Winter shutdowns. Europe is stagnating and Italy a thorn in the EUR. The US is powering for another 6-9 months with booming EPS growth and Fed hikes locked-in driving a rising DXY. I expect more infrastructure stimulus as well. Trump cannot afford to let it slow.

At some point the Fed is forced to brake either owing to slowing growth at home or abroad as markets crash.

Until then the Australian dollar keeps on falling with commodities and a slowing local economy delivering internationally positioned Aussie investors more out-sized late cycle returns.

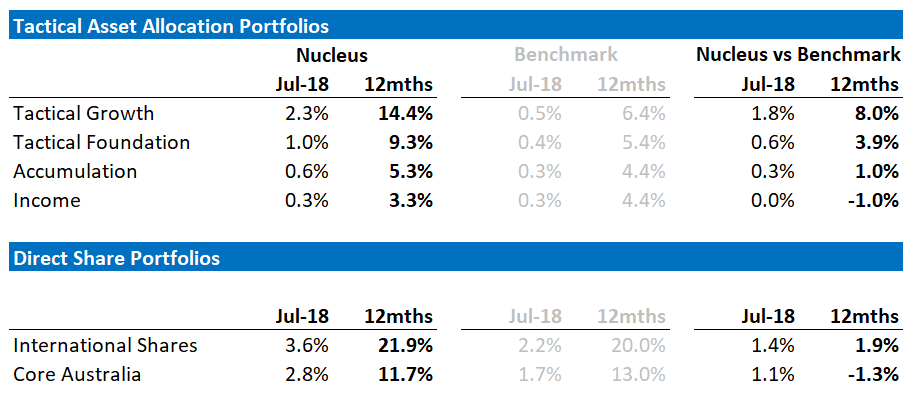

David Llewellyn-Smith is chief strategist at the MB Fund which is long US equities that will benefit from a falling Australian dollar so he is definitely talking his book. Below is the performance of the MB Fund since inception:

If the ideas above interest you then contact us below.