DXY has smashed overnight as the recent EM panic unwinds. CNY and EUR lifted:

AUD jumped against DMs:

If we follow the same pattern as the last few steps down then former support is now resistance and much of this rebound will now be done.

Against EMs, which still look very shaky, the AUD soared:

Gold firmed but not overly:

Oil too:

And base metals:

The caution in the bounce is obvious in miners which fell:

Nonetheless, EM stocks caught a bid:

Though EM junk fell:

Treasuries fell and the curve flattened:

Bunds too:

The S&P500 hit new all-time highs but couldn’t hold them:

The news is still whether and when the Fed moves next, despite our Donald. Governor Robert Kaplan kicked us off:

The neutral rate of interest is the federal funds rate at which monetary policy is neither accommodative nor restrictive. It is a theoretical concept, meaning that it can’t be directly observed—it must be inferred from market and other economic data. Economists’ views on this rate are necessarily estimates and inherently uncertain. However, while theoretical, estimates of the neutral rate are critical to assessing and making decisions regarding the stance of monetary policy.

My own view, informed by the work of my colleagues Evan Koenig at the Dallas Fed [7] as well as John Williams of the New York Fed and Thomas Laubach at the Federal Reserve Board, [8] is that the longer-run neutral real rate of interest is in a broad range around 0.50 to 0.75 percent, or a nominal rate of roughly 2.50 to 2.75 percent.

With the current fed funds rate at 1.75 to 2 percent, it would take approximately three or four more federal funds rate increases of a quarter of a percent to get into the range of this estimated neutral level.

At this stage, I believe the Federal Reserve should be gradually raising the fed funds rate until we reach this neutral level. At that point, I would be inclined to step back and assess the outlook for the economy and look at a range of other factors—including the levels and shape of the Treasury yield curve—before deciding what further actions, if any, might be appropriate.

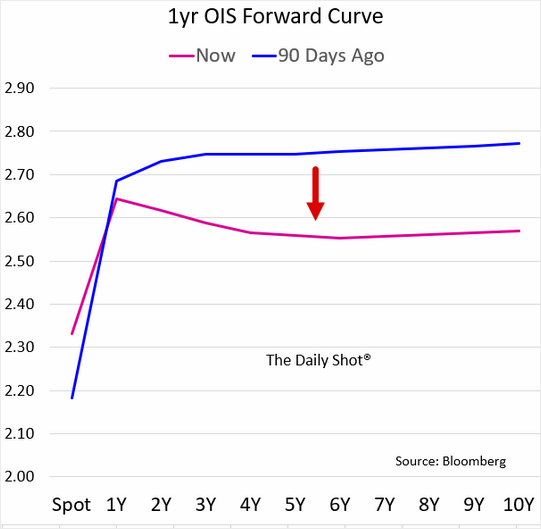

That will definitely be enough to invert the yield curve. Indeed futures are already pricing it:

As the Fed turns increasingly hawkish:

But it’s not all hawks. The doves are also flapping furiously around the inversion, via Tim Duy:

Atlanta Federal Reserve President Raphael Bostic threw down the gauntlet today with a declaration to dissent any policy move that will invert the yield curve. He may get the chance to make good on that threat in December – his last meeting in his current rotation a voting member.

Bostic, via Bloomberg:

“I pledge to you I will not vote for anything that will knowingly invert the curve and I am hopeful that as we move forward I won’t be faced with that,’’ Bostic said Monday in Kingsport, Tennessee, in response to an audience question. “The market is going to do what the market does, and we have to pay attention and react.’’

Arguably, there is some wiggle room here – the criteria for dissension is that the policy must “knowingly” invert the yield curve. And I suppose he could abstain from voting rather than dissent. Moreover, it is important to know what he views to be the relevant portion of the curve. Is it the 10-2 spread? Or the 10-Fed Funds spread? Inquiring minds want to know!

Still, Bostic reveals here a fairly strong conviction that the yield curve must be taken seriously as a warning sign that policy is in danger of turning too tight. His hopefulness that the Fed will not be faced with this decision, however, might be misplaced.

The 10-2 spread has narrowed to 24 basis points. Still not a recession indicator, or even an indicator of weakness in my opinion. What I am looking for is 10-2 inversion plus continued Fed tightening as a recession warning signal. But it is fairly easy to see how a Fed hike in September combined with expectations of continued gradual rate hikes into 2019 pushes the 10-2 spread close to inversion by the time the December meeting rolls around. It is also fairly easy to see that the US economy retains enough strength to justify a rate hike at that meeting. A rate hike at that point could reinforce future rate hike expectations and then push the curve into inversion. This would give Bostic the opportunity to follow through with his threat and dissent – if of course the 10-2 spread is the relevant spread.

Alternatively, if the 10-Fed Funds spread is his focus, his threat might be fairly meaningless as that inversion would not happen until much later. And probably by the time that happens a recession would be baked in the cake. In other words, his threat is only meaningful if he focuses on the long-leading indicator of the 10-2 spread.

And more importantly his threat means little to policy unless he can pull a significant portion of the voting FOMC members in his direction. While some Fed regional presidents are sympathetic to Bostic’s position, they still make up a minority of policy makers. Nor are they voting now. My guess is that given the 10-2 spread is such a long leading indicator, it will invert at a time when that data, from the Fed’s perspective, supports further rate hikes. Hence they are likely to hike through an inversion.

Bottom Line: My sense is that the majority of the Fed would find more reasons to ignore than embrace the signal from a 10-2 yield curve inversion. They will fall back on the basic theory that this time is different because the curve inverts at a lower level of rates than in previous inversions. If the yield curve doesn’t stop them from continuing rate hikes, what will? Certainly a clear slowdown in activity would do the trick. But that is obvious. Less obvious is the possibility that they pause after reaching their estimates of neutral even if the data remains consistent with above-trend growth. That would require something of a leap of faith by Powell & Co. that the lagged impacts of tightening had yet to materialize in a slower pace of activity.

The Kaplan base case of three to four more hikes looks solid. But beyond that is definitely in doubt:

That’s enough to keep the heat on DXY yet though some of that is because Europe and China will likely be even weaker for the next six months as the latter shuts down for Winter and the former reverts to form:

Beyond that, Trump is going to need to pull another fiscal rabbit out of the hat. Infrastructure is the obvious play. As China presses go on the same that may be enough to punt the global economy through 2019 and deliver more Fed tightening. But not without it.

The balance of risks still says the EM crisis is not over and neither are Aussie dollar falls.