On Friday the US dollar fell (DXY), the Chinese yuan (CNY) and Euro (EUR) lifted:

The crazy EUR long is at last extinguished. Now for the short!

Advertisement

The Australian dollar (AUD) jumped against all developed market (DM) forex:

And against emerging market (EM) forex :

Advertisement

Market positioning for the AUD last week shifted slightly less short:

Gold lifted:

Advertisement

Oil too:

Base metals jumped:

Big miners were bid modestly:

Advertisement

EM stocks too:

EM junk firmed:

Treasuries were bid:

Advertisement

Bunds too:

Not Italy:

And stocks firmed:

Advertisement

So, is it over? No. We are still far distant from any reversal in Federal Reserve tightening, the key driver of the EM crisis, and hope for a US/China trade deal is very preliminary. The Turkish lira did manage a goodly bounce:

But we’ve still only had a forex crisis. There’s been no default nor banking issues at all. They are coming. Some nice analysis at FTAlphaville shows just how far we have to run yet using the 1990s Asian crisis analogue:

Advertisement

You may have noticed Turkey is going through somewhat of a crisis.

It looks like a classic emerging-market meltdown: a rapidly growing economy funded by short-term, dollar-denominated liabilities, fronted by a strongman leader with a penchant for appointing insiders to key government positions.

Which reminds us of a better time — a time of boy-bands, Britpop and a forgetful Ralph Fiennes — yes, the nineties. And, of course, the Asian currency crises of 1997 and 1998. They hold lessons for Turkey.

We’ll tell you why. (Charts courtesy of Macquarie.)

Thailand

Unlike Turkey, before its crisis Thailand had pegged its currency, the baht, to the dollar. As anyone familiar with the Monetary Trilemma, or British politics in 1992, will know, a fixed currency mixed with open capital flows can spell problems in times of economic weakness.

Up to mid-1997, Thailand had been the recipient of a tidal wave of international hot money, helping to fuel 7.8 per cent GDP growth between 1980-95. According to Paul Blustein’s seminal book The Chastening, dollar-denominated loans to Thailand totalled $56bn in 1997, up from $19bn in 1994. The current account deficit on the eve of the devaluation was 8 per cent of GDP, according to a paper from the World Bank.

Investment flows from richer foreign countries to developing nations are in theory not a bad thing. As Duncan Weldon pointed out this week, foreign capital, if invested wisely, can help nations develop faster than they would otherwise. Yet a lot of this short-term capital had flowed directly into relatively unproductive real estate, via shadow banking institutions such as Finance Once. In 1996, 600,000 square meters of office space came on to the market in Bangkok alone, over half of it unleased. In 1998, 1.3m square meters was planned.

In 1996, however, the real estate market began to collapse as it became clear demand was drying up just as a tsunami of supply was hitting. By May 1997, non-performing loans had hit 12 per cent of all loans outstanding, partly thanks to speculative real estate projects. Blustein reckons the real number was significantly higher. Businesses like Finance One were crippled.

This severe disruption in Thailand’s credit markets spooked international financiers, who began questioning whether they should roll over their short-term funding to the stricken country, realising that if their investmentsweren’t safe, then the currency peg might not be either. The central bank, armed with a reported $30bn of reserves, intervened. One May 14, for instance, it threw $10bn at the baht an attempt to calm markets and vanquish short-sellers.

On May 15, the Bank of Thailand went one step further to stop speculators — it withdrew foreign banks’ ability to borrow baht except for trade-related reasons. But the bank was out of ammo. A disastrous $23bn trade using currency swaps meant the bank had far fewer foreign exchange reserves than anyone, including the IMF and Thai government, thought.

To avoid showing a weak hand, the Bank of Thailand relented and decided to let the baht float on July 2nd.

On August 21 the IMF announced a $17.2bn rescue package which included cash from Japan, the World Bank and the Asian Development Bank. The market, though, was still in the dark over the true reserve number. When the bailout failed to stabilise the currency, the Bank of Thailand, under pressure from the US Treasury, was forced disclosed the disastrous currency swap as speculation mounted over its reserves. By early 1998, the baht had crashed to 56 per dollar, despite structural reforms to clean up its stricken financial system, including the closing of 58 failing financial institutions and the introduction of deposit guarantees. Financial markets found it hard to believe political intent when they’d been deceived on key data.

Like Thailand, Turkey’s property market is also larger than life. Last year, 43 per cent of total foreign direct investment flowed into Turkey’s real estate sector, around $4.6bn. But it is unclear whether there is demand to meet this supply. For instance Emlak Konut, one of Turkey’s largest real estate developers, at the end of the last quarter had 716m liras worth of completed units on its balance sheet, versus 324m liras two years ago, and just 12m liras at the end of 2015. Turkey’s current account deficit is currently 7 per cent of GDP, via Thompson Reuters.

Yet Turkey’s banking sector seems OK for the moment. A research note from Barclays yesterday highlighted that while Turkish banks are heavily dependent on FX wholesale funding — it accounts for circa 20 per cent of bank liabilities — there is “sufficient FX liquidity to cover H2 18-19 FX maturities”. However, further depreciation in the lira, or a drop in asset quality, could spell trouble for banks hoping to rollover foreign liabilities in the next 6 months. Keep an eye on the refinancing of Akbank’s $940m syndicated loan, maturing at the end of September, for signs of broader investment confidence in the banking system.

Asset quality does seem to be a pivotal issue. By Barclay’s calculations, Turkish banks can absorb non-performing loan ratios of around 7 per cent. However, if the lira weakens to around the 7 lira per dollar range, this number drops to around 5 per cent. At pixel the Lira is holding around the 5.8 mark after touching 7 last week.

A lesson for Mr Erdogan from Thailand: surprises are bad. They will drag down the value of the lira. Best to let investors know what’s going on deep down inside of you, before they see that you’re falling apart.

Malaysia

Like Turkey, Malaysia’s financial unravelling started in the private sector. Malaysia’s economy was in relatively good shape when Thailand’s crisis spread to neighbouring countries. During the 1990s, real output growth averaged 8.5 per cent a year and unemployment steadied below 3 per cent. Malaysia did have a current account deficit, but its government had little short-term external debt and the foreign reserves to cover it.

What it didn’t have was the assets to also cover the private sector’s. As Dani Rodrik points out, during crises, “all short-term liabilities, regardless of whether they are domestic or foreign, become potential claims against the government’s liquid foreign assets”. So by mid-1997, with a domestic debt-to-GDP ratio breaching 170 per cent (one of the highest in the world at the time) and investors pulling capital from the country, Malaysia’s government found itself exposed. Between June 1997 and January 1998 its currency, the ringgit, weakened 62 per cent against the dollar.

While Malaysia didn’t go directly to the IMF for help, the Deputy Prime Minister embraced the Fund’s economic orthodoxy at first. The country hiked interest rates and cut government spending by 18 per cent. And despite the ringgit’s slide, they assured investors that the exchange rate would remain flexible and that capital would continue to flow freely.

Prime Minister Mahathir Mohamad had a different idea. He railed against currency trading. The practice was “unnecessary, unproductive and immoral”, he said. “It should be stopped. It should be made illegal”. Mahathir even got into a feud with investor George Soros, who was then shorting Thailand’s baht. Mahathir called him a “moron”. Soros called Mahathir a “menace to his own country”. And in September 1997, Mahathir penned an op-ed in the Wall Street Journal accusing Soros and his cohort of “manipulators” of bankrupting whole regions “to enrich themselves and their clients”.

With some officials saying one thing, and the Prime Minister saying quite another, investors yanked capital from the country at an even faster rate and placed larger bets in the offshore ringgit market that a devaluation was coming. The stock market fell to historic lows, property prices declined and the private sector increasingly could not service its debt. By June 1998 Mahathir all but declared that economic orthodoxy had failed. He cut interest rates and tried to reflate the economy through looser fiscal policy.

So Mahathir tried something more drastic. On September 1, 1998, Malaysia pegged the ringgit to the dollar and imposed controls on capital outflows in a bid to stop short selling in the offshore markets. The government ordered all ringgit assets abroad to be brought back onshore and banned foreigners from repatriating their investments. At the time, the IMF did not believe in capital controls. They have since walked back this stance a bit, in part because economies like Malaysia’s recovered strongly after implementing them.

All of this feels familiar at the moment. Turkey’s lira has weakened roughly 50 per cent in the past 12 months, and Erdogan has been on a similar media blitz. He recently wrote an op-ed in the New York Times and has threatened that “economic terrorists on social media” would pay for their actions. For now, interest rates are off the table, and the central bank has had to increase borrowing costs through a backdoor to avoid a confrontation with Erdogan. As in Thailand and Malaysia, Turkish officials also curbed its banks from using currency swaps and foreign exchange forward deals in an attempt to limit bets against the currency.

Mr Erdogan should know that investors never want to hear you say that short sellers and currency traders are the problem. This is almost always seen as a signal of distress, not strength.

Capital controls are not an immediate next step, but Charlie Robertson of Renaissance Capitals believes Turkey may be inching towards that outcome. GAM’s Paul McNamara disagrees. With a current account deficit, he says, you need capital to fund it. We wrote recently that Erdogan can’t sidestep the IMF for long. That kind of deal may be a ways off, but it still remains Turkey’s sturdiest lifeline.

Turkey and the IMF may be two worlds apart. But no matter the distance, investors may need Mr Erdogan to reach to his heart, calm his rhetoric, and accept a lifeline before it’s too late.

“Strongman” leaders and IMF bailouts do not sit well together, though they are all-to-often forced to in the end.

Before then, the Australian dollar is only enjoying a dead cat bounce.

Advertisement

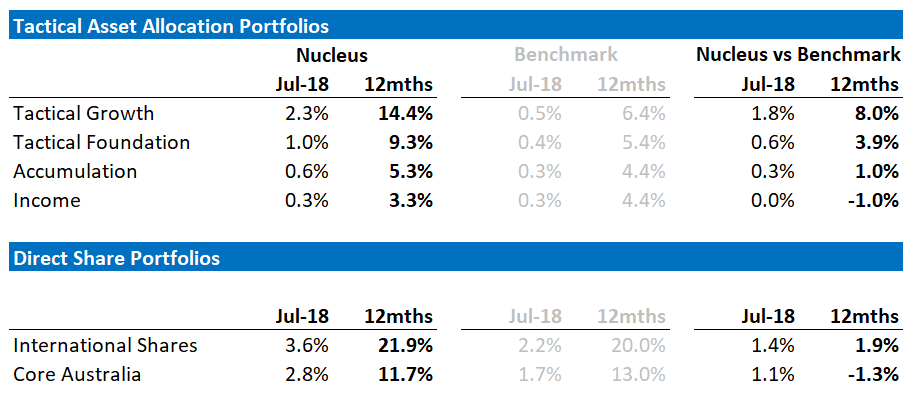

David Llewellyn-Smith is chief strategist at the MB Fund which is long US equities that will benefit from a falling Australian dollar so he is definitely talking his book Below is the performance of the MB Fund since inception:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.